(Bloomberg) — Follow Bloomberg India on WhatsApp for exclusive content and analysis on what billionaires, businesses and markets are doing. Sign up here.

Most Read from Bloomberg

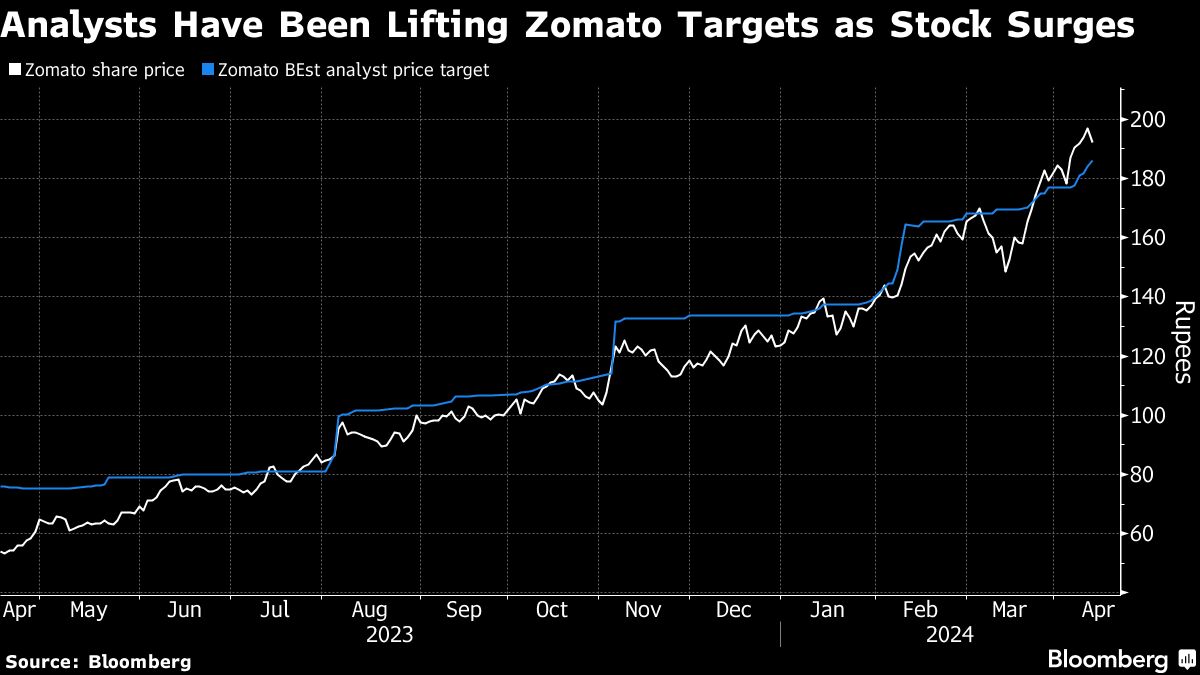

Zomato Ltd. has outpaced gains in all the world’s major delivery stocks over the past year, sending analysts scrambling to boost their outlooks for the Indian company as its profitability improves.

Price target upgrades for Zomato in the past 12 months exceed those for all other stocks in a Bloomberg Intelligence gauge of global ride sharing and delivery peers. At least five brokerages have lifted their estimates for the shares in just the past few weeks, including Citigroup Inc. and HSBC Holdings Plc.

The nearly 260% surge in Zomato since last April has made it difficult for consensus to keep up, but expectations continue to rise. Analysts have shifted earnings estimates into the black from previously expected losses, and optimism is growing for operations beyond the company’s core restaurant meal delivery business.

Goldman Sachs Group Inc. expects profit forecasts to increase for Zomato’s “quick commerce” business Blinkit, analyst Manish Adukia wrote in a recent note. While “earlier investor conversations suggested skepticism around profitability of this business model,” concerns should ease as more results are reported, he said.

Some see the bull run in Zomato as stretched, with the stock showing technical signs of overheating. It’s also trading at 115 times forward earnings, well above multiples for global peers including Uber Technologies Inc., Deliveroo Plc and Meituan.

The Indian firm’s shares are pricing in profits of over $300 million when it only just recently reached breakven, says Rahul Jain, an analyst at Dolat Capital Market Ltd. Jain is one four analysts with a sell rating on Zomato, versus 24 buys and no holds, according to data compiled by Bloomberg.

The rich valuations for Zomato looked justified given “significantly higher” projected revenue and profits for the company, according to ICICI Securities Ltd. analyst Abhisek Banerjee. The broker adds that the stock has basically moved in line with Doordash Inc. over the past six months amid improving sentiment on tech stocks around the world.

Banerjee also notes recent awareness of the strong potential for quick commerce, which includes grocery delivery. The Indian market, where Zomato’s biggest competitor is unlisted Zepto, is expected to grow at a compound annual rate of 29% to reach $36 billion by March 2033, according to the ICICI Securities analyst.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.