(Bloomberg) — A resurfaced speech from Chinese President Xi Jinping suggests policymakers may start trading government bonds to regulate liquidity in the market, pushing the nation toward strategies used by the Federal Reserve and other major central banks around the world.

Most Read from Bloomberg

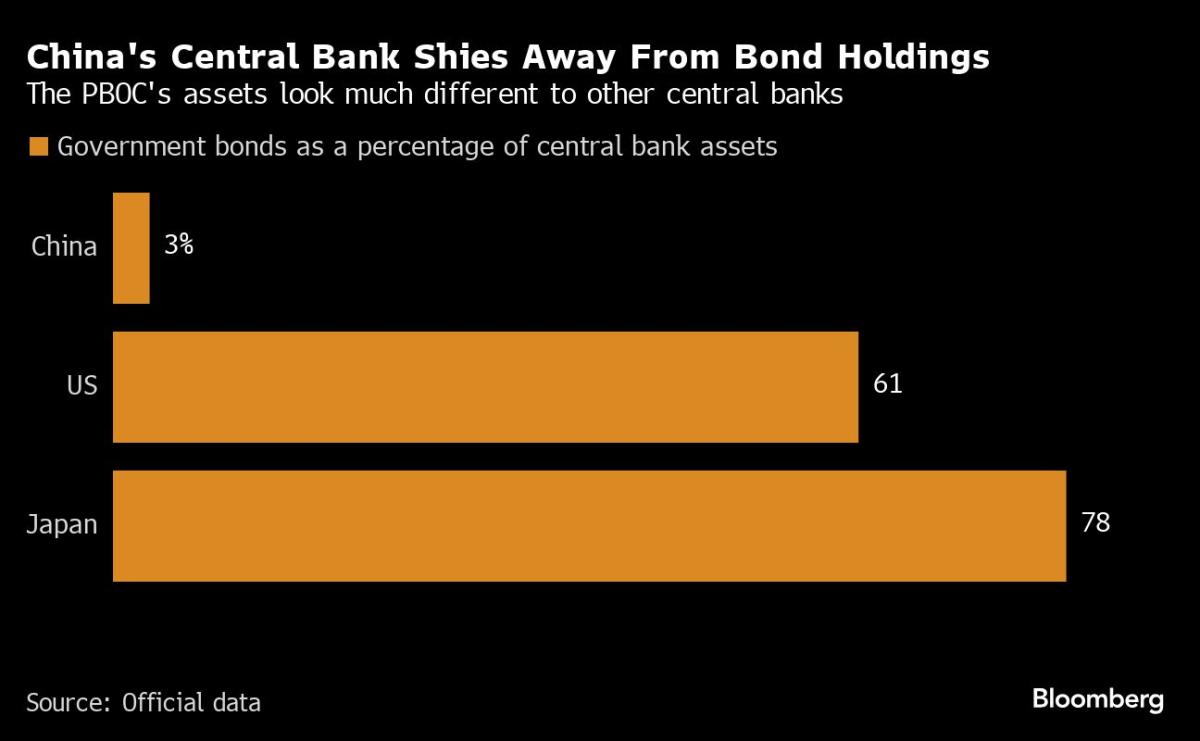

Xi’s call for the People’s Bank of China to “gradually increase the buying and selling of government bonds” in its open market operations sparked a frenzy of speculation among traders last week. The remarks — made in October but publicized recently in a new book and newspaper article — may hint at a policy pivot for a central bank that hasn’t made a significant bond purchase since 2007.

“Central banks in other countries generally use government bonds, or sovereign credit, as a basis to issue money,” said Liu Lei, a researcher at the National Institution for Finance and Development, a state think tank advising government agencies in China. “This is a necessary path for China’s central bank and monetary system to move into modern times.”

The vague comments from the Chinese leader led some traders to initially argue that Beijing may be considering quantitative easing — an unconventional form of stimulus that involves purchasing sovereign bonds and other assets to push down yields and boost economic activity. First adopted by the Bank of Japan more than two decades ago, the tactic was later used by the Fed and other policymakers after the global financial crisis and the coronavirus pandemic.

China’s economic woes have stirred debate in recent months about whether the world’s second-largest economy would consider drastic policies to shore up some sectors, like property. The PBOC has already been using targeted lending programs that some analysts liken to QE because they expand the central bank’s balance sheet.

Several economists demurred from interpreting Xi’s appeal for government bond trading as a revolutionary shift in policy.

For one thing, Xi specifically mentioned both buying and selling — a notable distinction from QE, which generally involves buying and holding government bonds and other assets, especially at a large scale. Interest rates in China are also still well above zero, giving less reason for the PBOC to consider a tactic that’s usually regarded as an emergency tool to spur demand when short-term rates have flatlined.

The PBOC didn’t respond to a faxed request for comment from Bloomberg News late last week about Xi’s speech. In the past, it has signaled disapproval over QE: Former governors have pointed to potential risks from US-led QE and warned that asset purchases would damage markets, hurt the reputation of central banks and create “moral hazards.”

Instead, the trading of sovereign bonds may be best viewed as an additional tool for the PBOC to pump liquidity into the market and ensure rates are stable.

The central bank already has several ways to provide money to the economy. It can inject funds through its monthly medium-term lending facility to support commercial bank lending, or lower the amount of cash banks need to keep in reserve.

Those methods have shortcomings, though. Economists see shrinking space for further cuts to the reserve requirement ratio. Loans need to be renewed. And any misjudgment of demand for liquidity risks leading to a serious cash crunch.

The PBOC “needs more flexibilities in managing liquidity and more tools to expand its balance sheet,” UBS Group AG economists Nina Zhang and Wang Tao wrote in a Thursday note. Because the size of the government bond market has expanded over the years, central bank bond trading has become “more necessary and feasible,” they added.

While the directive from the most important man in China certainly indicates the central bank may start buying up bonds, the actual timing of any purchase remains up for debate.

Central bank bond buying will likely be a “very slow process,” said NIFD’s Liu, adding that the shift is still in its “design phase.”

Others suggest forthcoming fiscal stimulus may mean the PBOC pulls the trigger on purchases sometime this year. That would help alleviate liquidity pressure from an upcoming surge in bond supply resulting from the planned issuance of 1 trillion yuan ($138 billion) worth of special sovereign debt in 2024, according to a report from Goldman Sachs Group Inc. economists on Thursday.

It’s also not clear how ramped up bond purchases would impact Chinese yields. They’d likely fall in the short term, according to Citigroup Inc. strategist Philip Yin, since the central bank’s debt purchases “should help improve market confidence about liquidity and digesting future government bond supply.”

The longer-term effects may be mixed. If China combines the use of more liquidity tools with further policies to stabilize economic growth, investors may shy away from safe haven assets in favor of riskier ones.

Whatever China’s strategy, there’s a reason Xi’s comments have created such a stir: Once a central bank decides to start trading government bonds, things can snowball quickly.

The Bank of Japan, for example, intended to limit the scope of its initial program in 2001 before ramping up the amount of bonds it bought. When it embarked on a second round of QE in 2013, Japanese policymakers folded their regular bond trading program, called rinban, into their massive new asset purchasing plan.

In other words, there’s sometimes little real difference between buying bonds as a liquidity tool versus doing so to stimulate the economy.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.