(Bloomberg) — Iron ore behemoth Fortescue Ltd.’s months-long stock rally suffered a big pullback in February as investors turned sour on the company’s earnings growth and high exposure to slumping metal prices amid China’s rocky recovery.

Most Read from Bloomberg

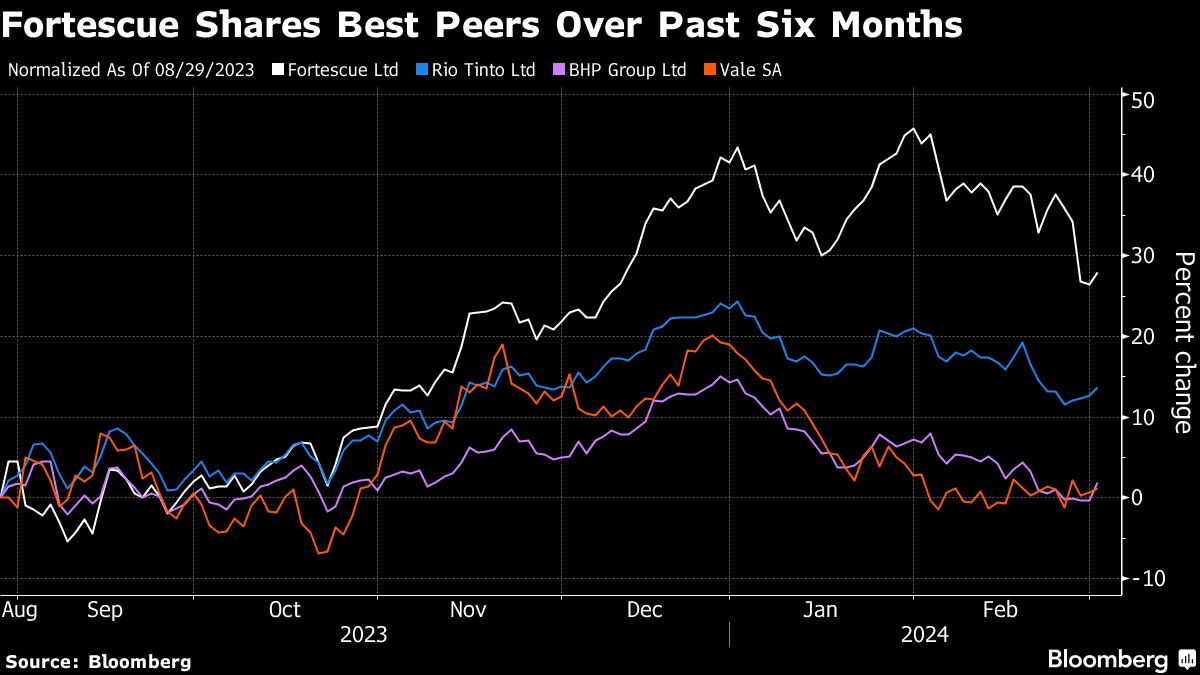

The world’s fourth-largest iron ore miner is tipped for the greatest earnings slowdown over the next year compared with peers BHP Group Ltd., Rio Tinto Group and Vale SA, according to data compiled by Bloomberg. Shares of the Australian firm founded by billionaire Andrew Forrest have surged almost 30% in the past six months, outpacing peers. But since the start of this year, shares have tumbled alongside iron ore, one of 2024’s worst-performing major commodities.

As a relatively high-cost producer, the miner is more sensitive to iron ore price swings compared to peers, according to Mohsen Crofts, a Bloomberg Intelligence analyst based in Sydney.

“Fortescue’s operating margins are slimmer than BHP or Rio Tinto’s. Any change in the iron ore price will therefore have a greater Ebitda impact for Fortescue,” he said. “While BHP and Rio now get a material share of their revenue from base metals, Fortescue is for now still fully reliant on iron ore.”

The metal makes up about 91% of Fortescue’s revenue, compared to about half for BHP and Rio Tinto, according to Bloomberg-compiled data. Fortescue’s iron ore business propped up its half-year earnings released in February, bucking a trend of declining profits among its diversified rivals. But now Fortescue’s earnings growth is in doubt, with analyst estimates suggesting 14% downside for next year, the worst among its peers.

Read: Fortescue’s Profit Jump Defies Downturn for Mining Rivals

The Perth-based miner’s bumper stock run has also been halted by dwindling metal prices. China’s property woes have weighed on the steelmaking ingredient, which lost 10% last month. Post-Lunar New Year demand for iron ore remains disappointing amid a slow recovery to construction activities, wintry conditions and sluggish home buying.

“While Fortescue has benefited from significant unit cost reductions, cost inflation is kicking in now,” Jefferies analysts led by Mitch Ryan wrote in a note dated Feb. 28, downgrading the miner to underperform from hold after earnings. “While we believe management has done an excellent job operationally, Fortescue’s share price will be highly dependent on the iron ore price.”

The stock has no buy ratings and an average 12-month price target that’s 16% below Friday’s close, according to data compiled by Bloomberg. Meanwhile, price targets for rivals BHP, Rio Tinto and Vale all point to potential upside.

Still, the stock slump isn’t unique to Fortescue. Miners are the biggest laggards on the Australian benchmark this year as commodity prices from iron ore to lithium and nickel crater. Fortescue has fallen 10% so far this year, with BHP and Rio posting similar drops.

Despite lackluster demand in recent weeks from China, the world’s largest steel manufacturer, analysts expect iron ore futures to regain lost ground in the short and midterm. UBS Group AG, which has a sell rating on Fortescue, estimates the metal’s price will trade around $120 a ton for the remainder of 2024 before a plateau. Demand will be propped up by a growing appetite in India and Southeast Asia thereafter.

“We’ve always said that we would see China steel demand peaking, and it’s exactly what we’ve said,” Rio Tinto Chief Financial Officer Peter Cunningham said in an analyst call last month. “Then you just see demand from elsewhere in Asean and in India growing as well. So, I think all of this is playing out exactly pretty much as we thought it would play out over time.”

–With assistance from Liz Yee Xing Ng.

(Updates with share performance in ninth paragraph)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.