The residential real estate market tightened up in 2022 and 2023. Many homeowners — sitting on low-interest-rate mortgages — decided against selling their homes after the Federal Reserve went through its quickest rate-hiking cycle in history in its effort to bring soaring inflation back down. The combination of lower inventory, higher mortgage rates, and persistently high asking prices froze real estate activity in the United States, and the market will likely take many years to thaw out.

Almost every company associated with residential real estate suffered over the last few years — perhaps none more so than Opendoor Technologies (NASDAQ: OPEN). Shares of the company, which directly buys and sells single-family homes through its online platform, have sunk by 91% from their all-time high.

But with the Federal Reserve signaling it will start to reduce the benchmark federal funds rate in 2024, could Opendoor be set for a rebound over the next two years?

Lower revenue, no profits

Opendoor is in the iBuying business: It purchases homes from individuals quickly for cash, performs some (usually minor) repairs and improvements, and then resells them at a (hopefully) higher price. This business model has a few problems that have kept Opendoor from profitability.

First, it has extremely thin unit economics. Last quarter, Opendoor’s gross margin was 9.8%, and it has been under 10% for each of the last five quarters. Even when home prices were rocketing higher during 2020 — allowing Opendoor to sell its inventory at a nice profit — its gross margin was not much better. For example, it was only 15.4% in Q4 2020.

Second, it is highly capital-intensive to buy and own thousands of homes at any given time, which creates working capital and inventory issues for Opendoor. In order to finance its home purchases, it has a revolving credit facility that allows it to take out loans to add more homes to its balance sheet. It has to then pay interest on these loans until it eventually sells the inventory to individual buyers.

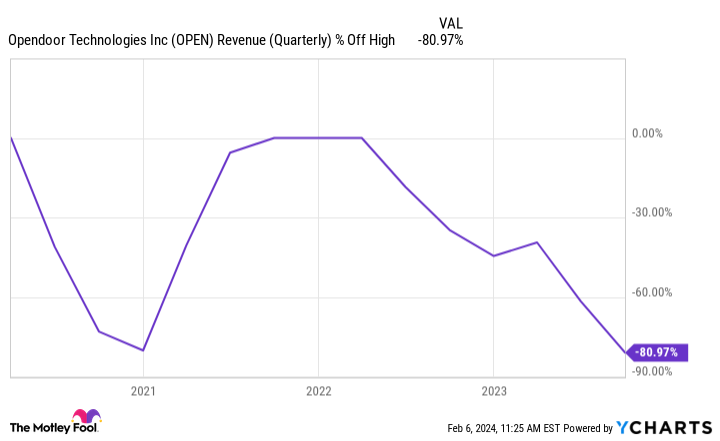

On top of these structural business model issues, homebuying by individuals dried up in the United States in 2022 and 2023. In reaction to this, Opendoor was forced to severely decrease the size of its operation, bringing down how many homes it bought, and cutting marketing expenses and general overhead costs. Last quarter, revenue was $980 million, off 80% from its all-time high.

The company will grow again, but at what cost?

With the real estate market starting to unfreeze at the end of 2023 and early 2024, Opendoor has started to increase its buying activity again. In Q3 2023, the company purchased more than 3,000 homes, bringing its acquisition rate back to around Q4 2022 levels. It still expects to report that revenue declined in Q4 2023, but management is optimistic about getting the business back to growth in 2024.

But investors should be asking: Will this change anything? Regardless of whether Opendoor was growing or shrinking, it has never generated an annual profit. Over the last 12 months, it has posted a net loss of $583 million. And it is nowhere close to finding a way to generate profits. Even if it doubled its quarterly gross profit generation to $200 million, that would barely cover the $175 million in quarterly operating expenses it had in the third quarter. That doesn’t include its interest expense, either.

If Opendoor plans on growing its revenue, it will likely need to spend more on marketing. It will also need to take on more debt to grow its inventory. No matter how you slice it, Opendoor has a tough — perhaps impossible — path to generating positive net income.

All indicators are negative

Opendoor stock may look like a bargain at first glance. Shares are down 90% from their highs, and trade at a cheap-looking price of $3.35, as of this writing. But the actual price of a stock doesn’t matter. It all comes down to the company’s market cap and the amount of future cash flow it is expected to generate.

The hard truth is that Opendoor has a cumulative net deficit of $3.2 billion since its founding, and that deficit grows each quarter. It doesn’t matter what its market cap is: A company that will never generate a profit is worth less than zero. Don’t touch Opendoor stock with a 10-foot pole. Its business model is broken beyond repair, and its shares are likely to end 2025 much lower than they began 2024.

Should you invest $1,000 in Opendoor Technologies right now?

Before you buy stock in Opendoor Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Opendoor Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Opendoor Technologies. The Motley Fool has a disclosure policy.

Opendoor Technologies: Where Will the Stock Be in 2025? was originally published by The Motley Fool