(Bloomberg) — UBS Group AG’s hotly anticipated three-year growth plan will take the spotlight next week, when it reports alongside French peers Société Générale SA and Crédit Agricole SA.

Most Read from Bloomberg

The Swiss bank is expected to map out in more detail the course it intends to take after integrating Credit Suisse. While investors are counting on profitability improving, UBS’s ability to retain top talent will be key, even more so as central banks pivot toward interest rate cuts and rising impairments threaten earnings power across the sector, analysts say.

Results from US peers earlier this month point to a drop-off in fixed-income revenue as well as net interest income in the fourth quarter, although better-than-expected equities trading bodes well for UBS, according to Bloomberg Intelligence’s Alison Williams.

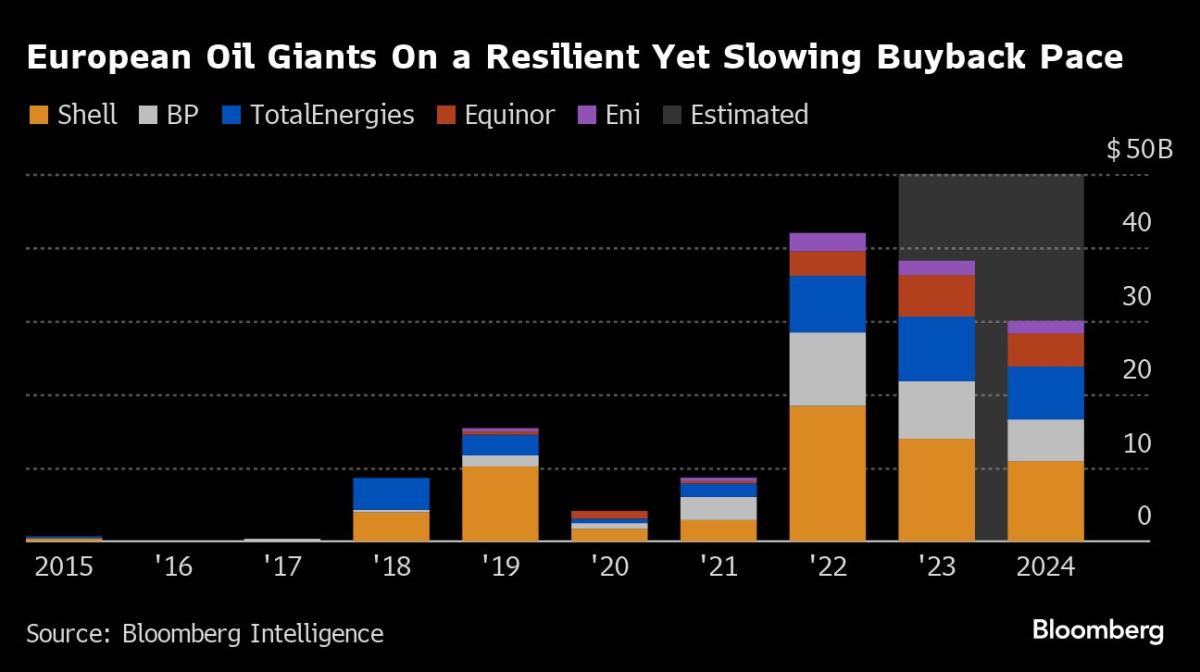

Buybacks will top the agenda for oil majors Equinor ASA, BP Plc and TotalEnergies SE, also due.

While softer demand and a mild winter may have crimped refining margins last quarter, Houthi attacks on freight ships in the Red Sea have been driving up the price of oil again.

Highlights to look out for:

Monday: Vodafone (VOD LN) may have seen a modest slowdown in organic service-revenue growth in its fiscal third quarter, though topline gains and easing energy costs mean its full-year goal of flat Ebitda could still be achievable, said BI’s Erhan Gurses. Price increases in Germany may have helped on the operational side but expect cable TV regulation headwinds from the fourth quarter. Vodafone’s escape routes from punishing competition in Italy are dwindling after it rejected an offer from Iliad SA to merge their units there. The clock is also ticking on efforts to combine its UK unit with CK Hutchison Holdings Ltd.’s Three in what’s shaping up to be one of the most closely watched antitrust reviews this year. Its African unit Vodacom on Friday reported a 27% revenue jump to 38.9 billion rand ($2.1 billion), boosted by the acquisition of Vodafone Egypt.

Tuesday: UBS (UBSG SW) has signaled uncertainty around any remaining opportunity to regain Credit Suisse deposit and wealth assets. Underlying wealth flow and deposits may show signs of stabilization, although talent-retention risks remain. Legal issues and any insight into January trends are also on investors’ minds. The pace of profit growth will be pivotal going forward, so expect buybacks to be on the conservative side in the near term, BI’s Alison Williams said.

-

Oil trading could be BP’s (BP/ LN) “swing factor” in the fourth quarter, according to BI. Adjusted operating profit likely slipped sequentially as growing upstream production — probably last year’s highest — failed to offset weakness in its downstream unit. Consensus shows the refining margin down 42% year on year. Watch for any update on BP’s renewable energy ventures after hedge fund Bluebell urged the company to rethink its planned reduction in oil and gas output in a shot across the bow for newly installed Chief Executive Murray Auchincloss.

Wednesday: TotalEnergies (TTE FP) is expected to announce a $2 billion buyback for the first quarter, with total repurchases last year likely reaching the targeted $9 billion, thanks in part to Canadian oil sands disposals. At the same time, a contraction in European refining margins and low utilization rates from major turnarounds probably crimped overall earnings, BI said. Adjusted net income for the fourth quarter slid 27% to $5.5 billion, consensus shows.

-

Equinor’s (EQNR NO) fourth-quarter results could be impacted by mild winter weather and full European natural gas inventories at the start of the heating season, which drove gas prices lower, but upstream volumes may have surpassed 2.1 million barrels a day, BI’s Will Hares said. Adjusted net income likely fell 57% year on year. The company should keep up the pace of buybacks and upgrade its dividend policy for 2024, though it’s unlikely to match last year’s extraordinary dividend of $1.80 a share, Hares said.

Thursday: BNP’s 50% net income slump and weak outlook knocked shares of SocGen (GLE FP) and Crédit Agricole (ACA FP) on Thursday as investors grow wary of potential road bumps for banks ahead. Consensus shows SocGen’s profit probably slid even more than 50% last quarter. Progress on cost cuts as it restructures the investment bank will also be in focus, according to BI. Crédit Agricole may have fared better, with net income seen 17% lower. Revenue gains from International Retail Banking and its business in Italy should have offset limp growth in French retail banking, said BI’s Uzair Kundi.

-

Maersk’s (MAERSKB DC) Ebitda probably slumped more than 80% in the fourth quarter, stacked against the high freight rates of 2022. Although the Middle East conflict is driving up freight rates again, as diversions around the Cape of Good Hope add 10 to 12 days to voyages, structural challenges in the industry mean these will probably crash back to pre-war levels once the crisis has abated, according to BI.

-

Adyen’s (ADYEN NA) second-half revenue and costs will be closely watched after price competition in the US led to disappointing growth in the early part of 2023. The Dutch payments company will likely report Ebitda margin still well below 50%, consensus shows. Cost normalization after “rampant hiring” will be key for margin recovery, said BI’s Tomasz Noetzel and Mar’Yana Vartsaba.

Friday: Hermès’s (RMS FP) annual results will cap what’s been a mixed reporting season for Europe’s luxury sector so far, with French peer LVMH showing resilience but the UK’s Burberry wilting. Hermès may be on the winning side, with consensus putting fourth-quarter sales growth in the low teens, double the average pace of its peers, BI’s Deborah Aitken said. Asia likely led the way with an estimated 17% revenue growth at constant currencies in the quarter, but double-digit increases across all regions are expected.

–With assistance from James Cone, Jenny Che, Valentine Baldassari, Paula Doenecke, Christopher Jungstedt, April Roach and Ana Monteiro.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.