(Bloomberg) — Traders are piling into bets for a surge in US Treasuries, re-entering a bullish trade they’d fled in the runup to last week’s inflation data and Federal Reserve decision.

Most Read from Bloomberg

Demand for futures contracts that stand to benefit from a rally in the bond market has roared back in the past week, with investors reinvigorated by economic indicators — from ebbing price-pressures to weak retail sales — that bolster the case for lower US interest rates. The market is pricing in two quarter-point rate reductions in 2024, compared to Fed officials’ projection for one.

Momentum is building in the cash market, too, with a JPMorgan Chase & Co. survey signaling the largest net-long in about a month.

It’s a well-timed shift for traders who’d all but abandoned bets for a rally just before last week’s rare double-risk event of inflation data and the Fed’s interest-rate decision. By late last week, fresh long positions were dominating the bond market’s climb, which saw 10-year yields drop below 4.20% on Friday for the first time since April 1, positioning data show.

Treasuries rallied on Tuesday after US retail sales data fueled expectations for lower US borrowing costs.

Open interest, or the amount of new risk held by traders, rose substantially. Patterns in open interest were also consistent with short covering as the swaps market re-priced around two 25-basis-point rate cuts for the year.

CFTC data supported a similar trend, with asset managers aggressively unwinding short positions in futures linked to the Secured Overnight Financing Rate right up until last Wednesday’s inflation data. They’ve flipped net long for the first time since the start of July 2023.

Here’s a rundown of the latest positioning indicators across the rates market:

JPMorgan Clients Bullish

In the week up to June 17, JPMorgan’s Treasury client survey showed long positions rising 6 percentage points, pushing the all-client net long to the highest reading since May 20. Outright shorts dropped 2 percentage points on the week, with neutrals falling 4 percentage points.

Options Premium Closer to Neutral

After premium to hedge a rally in Treasuries rose to highest levels of the year at the end last week, the skew has drifted back to near neutral as yields remain inside last week’s lows. The unwind of call premium has been helped by traders liquidating long positions in futures, which appeared to be a dominant force behind Monday’s selloff. Recent standout Treasury options flows have included a large sale of 10-year September puts for a premium of around $30 million, which Tuesday’s open interest release showed as a new position.

Asset Manager Flip Net Long SOFR Futures

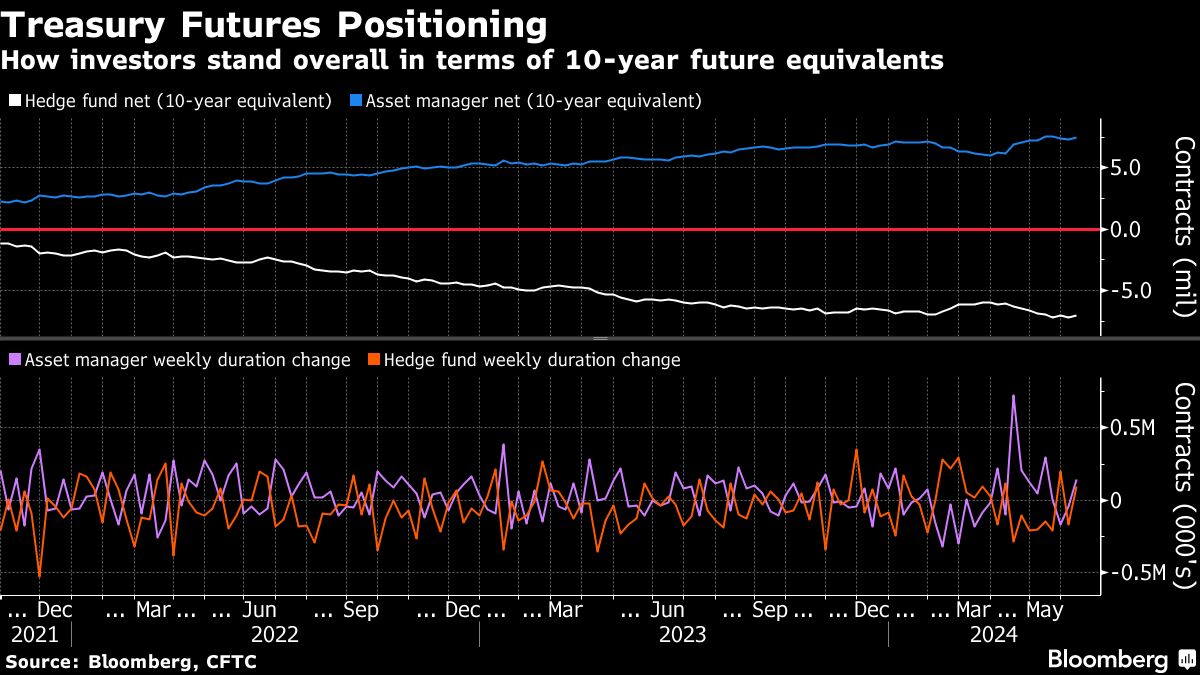

In CFTC data up to June 11, asset managers were bullish, adding to a net duration long from the two-year out to ultra-long bond futures by roughly 140,000 10-year note equivalents. In SOFR futures, asset managers added $8.2 million per basis point in risk, flipping net long in the process for the first time since July 4. Meanwhile hedge funds unwound net short position in Treasury futures by the equivalent of approximately 95,000 10-year note futures equivalents.

Active SOFR Options

The top three traded strikes out to Mar25 tenor over the past week are those involved in the SOFR Dec24 95.1875/94.9375/94.6875 put fly which was bought heavily on Friday, with flows including a 35,000 buyer at 6.25 which open interest showed as new risk. The 98.1875 strike has also appeared in the SOFR Sep24 95.125/95.1875 call spread over the past week, which has been bought in 55,000 at 0.5 which takes positioning in the structure up to around 90,000.

SOFR Options Heat Map

In SOFR options out to the Mar25 tenor, the most active strike is the 96.00 level equivalent to a 4% rate. Large trades involving the strike include the SOFR Mar25 96.00/95.50/95.00 put fly and the SOFR Sep25 96.75/96.00/95.25 put fly. Recent popular trades have also included the SOFR Dec24 96.00/97.00 call spreads which traded back in May.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.