Dividend stocks are an important anchor for well-balanced portfolios. Regular cash distributions can buffer a portfolio against market volatility and provide a steady income across business cycles.

Still, picking dividend stocks is no easy task. Companies operating in high-tech areas like healthcare often face unique competitive pressures that can diminish free cash flows, lowering their ability to reward shareholders via ever-larger dividend checks.

Bristol Myers Squibb (NYSE: BMY), or BMS for short, is a prime example. The drugmaker’s shares are down by over 17% year to date and over 33% over the prior 12 months.

Despite one of the richest dividend yields in the sector at 5.6% and a reasonable payout ratio of only 59.8%, investors have shied away from the stock for three key reasons:

-

Newer drug launches, such as heart medication Camzyos, are ramping up slower than expected.

-

BMS is facing one of the steepest patent cliffs in the industry come 2028 when cancer medication Opdivo and blood thinner Eliquis could both face generic competition.

-

BMS is dealing with the loss of patent protection for its cancer medication Revlimid, which it gained through its acquisition of Celgene in 2019.

Here’s why contrarian investors may want to scoop up this unpopular dividend stock right now.

Bristol Myers Squibb: A proven value creator

Developing new drugs is incredibly difficult. Many therapeutic categories sport failure rates over 90%. BMS has successfully lowered its risk profile from new drug development by buying promising drugs in late-stage development. In March, for example, the pharma giant completed its acquisition of Karuna Therapeutics, adding the potential blockbuster schizophrenia treatment KarXT to its neuroscience portfolio.

Acquisitions are slow-burn value creators in the pharmaceutical industry, frequently adding significant debt to a company’s balance sheet. But they also mitigate some of the unknowns of drug development, providing shareholders with a clearer vision of the path forward.

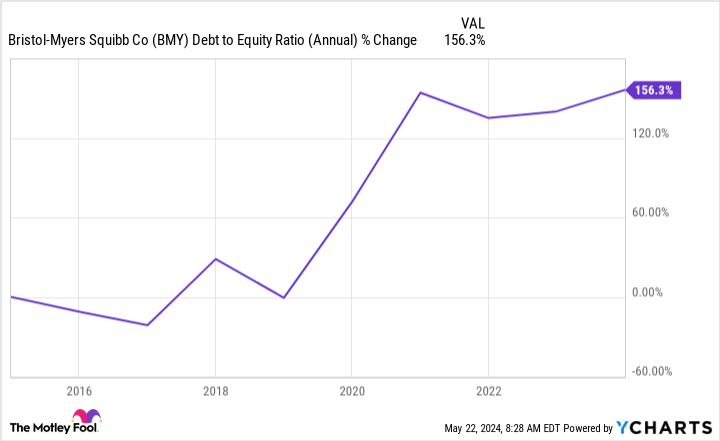

Indeed, BMS’ debt-to-equity ratio has ballooned recently thanks to its acquisitive ways. However, investors should keep the long-term in mind regarding these kinds of deals.

BMY Debt to Equity Ratio (Annual) data by YCharts.

KarXT holds tremendous commercial potential, with some analysts pegging its peak sales over $7 billion per year, depending on its ability to expand into other indications like Alzheimer’s disease psychosis, Alzheimer’s disease agitation, and bipolar 1 disorder.

What’s more, BMS’ struggles with Camzyos and other newer med launches should eventually fade away. The company has a long tradition of creating value for shareholders by expanding drug labels, creating unique marketing campaigns, and leveraging its extensive infrastructure to gain market share.

These initiatives take time to bear fruit. But it’s also probably a bad idea to bet against a proven value creator like BMS.

Final thoughts

BMS’ years-long slide is arguably overdone at this point. Yes, the drugmaker is going through a rough patch with slower-than-expected new drug sales, an upcoming patent cliff, and a growing need to deleverage quickly.

But it’s also important to remember that high-yield dividend stocks tend to outperform most other asset classes when held for extended periods (greater than 20 years). So, if you have a long-term horizon and don’t mind some short-term volatility, this unpopular dividend stock may be a stellar addition to your portfolio.

Should you invest $1,000 in Bristol Myers Squibb right now?

Before you buy stock in Bristol Myers Squibb, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Bristol Myers Squibb wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $584,435!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

George Budwell has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bristol Myers Squibb. The Motley Fool has a disclosure policy.

This Unpopular Dividend Stock Is a Buy was originally published by The Motley Fool