When it comes to the tech heavyweights in the artificial intelligence (AI) space, companies such as Nvidia, Microsoft, and Alphabet immediately come to mind. By contrast, legacy PC company Dell Technologies (NYSE: DELL) doesn’t. But Dell stock is up 185% over the past year, and AI is driving its gains.

Dell completed its fiscal 2024 on Feb. 2. For the year, the company’s net revenue of $88.4 billion was down 14%, and its operating income was down 10% to $5.2 billion — hardly the kind of financial results one would expect to drive triple-digit gains for the stock.

Dell’s financial results may have been down, but price targets from Wall Street analysts were up due to the company’s upbeat commentary on AI. As the company’s Chief Operating Officer Jeffrey Clarke said: “We have positioned ourselves well in AI. We’ve already started to benefit from the momentum we’re seeing.”

Indeed, in its fiscal fourth quarter, Dell shipped $800 million of its hot AI product. This was a 40% increase from the previous quarter, and it has investors buzzing about its future.

What’s going on with Dell?

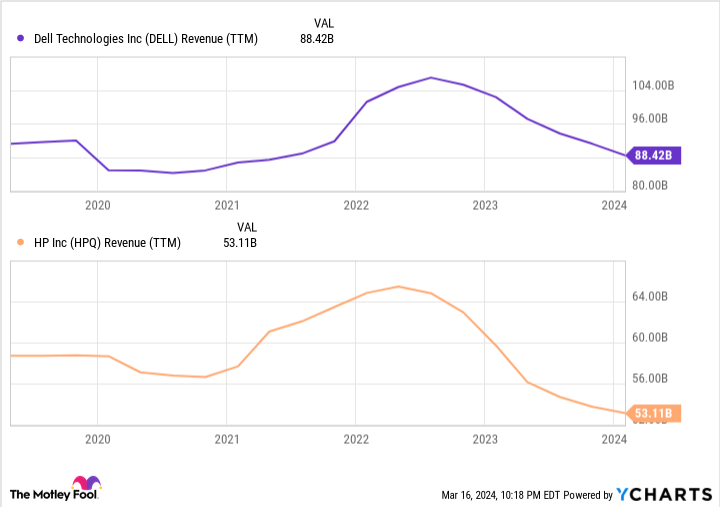

The PC market is notoriously cyclical, and it’s in the slow part of the cycle right now. The decline in Dell’s revenue reflects this as does revenue for top PC rival HP. Many consumers bought new computers in the early days of the pandemic and don’t want to upgrade right now unless they get a good deal.

Therefore, PC companies such as Dell and HP are struggling to get a sale unless it’s for lower-priced models, but the lower end of the market has slimmer profit margins.

The PC market cycle is reflected in the charts for Dell and HP’s revenue over the last five years.

As the AI trend takes off, these PC companies need a strategy. HP is positioning itself for AI personal computers, which management believes will represent 40% to 60% of PC sales three years from now. But for its part, Dell is finding success in AI-optimized servers.

A lot of computing power is needed to run AI applications — power that many businesses don’t have. Therefore, many believe the cloud-computing companies will benefit from the rise of AI since enterprises will go to them for the necessary power.

However, Dell is taking a different long-term view of the AI market. In the latest earnings call, Clarke also said, “We believe the long-term AI action is [on-premise], where customers can keep their data and intellectual property safe and secure.” In other words, the company believes businesses will internally build what they need for AI, which is where its AI-optimized servers come in.

What should investors do now?

As trendy as AI is right now, investors should maintain the right perspective first and foremost when it comes to Dell stock.

First off, the market appears to have high expectations when it comes to Dell’s AI progress. From a price-to-earnings perspective, the stock’s valuation has shot up far above what’s normal for this business.

To be sure, Dell’s AI business is taking off. On top of its aforementioned Q4 shipments, the company now has a $2.9 billion backlog for its AI-optimized servers, which was almost twice as big as its backlog in the previous quarter.

That said, Dell is nearly a $100 billion business; its AI backlog is quite small by comparison. Therefore, this is still largely the same business it’s been all along, which is reason for caution when it comes to the elevated valuation now.

Moreover, it’s unclear how sustainable the AI trend is for Dell. It costs a lot of money to invest in building internal AI capabilities. As companies experiment, they need to see enough return on the investment to continue down that path.

As Dell’s Clarke went on to say, “Most customers are still in the early stages of their AI journey.” That can be good if its customers continue building AI capabilities on premise. But it could be bad if those customers opt for a different AI strategy after dipping their toes in the water with Dell’s servers.

Ultimately, Dell is a good company, and its core businesses will bounce back as the PC cycle improves. Management is intent on returning profits to shareholders, and this can boost the stock. And don’t misunderstand: Its opportunity with AI is promising.

As is always the case with investing, however, it’s possible for investors to get too excited about good things, which can lead to downside risk as expectations become more realistic. Therefore, it’s important for investors to keep the AI news with Dell in perspective.

Should you invest $1,000 in Dell Technologies right now?

Before you buy stock in Dell Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dell Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 18, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, HP, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The PC Market May Be Soft, but 1 Part of Dell’s Business Is Booming Like Never Before Thanks to AI was originally published by The Motley Fool