The best investments are often small companies with bold ideas that change the game for an industry. Opendoor Technologies (NASDAQ: OPEN) fits that description nicely.

Today, buying and selling a home is about as painful as it was 40 years ago. Opendoor’s ambition to bring a digital touch to the experience and more accessible liquidity for buyers and sellers gives the stock immense potential, even if there are plenty of risks involved.

Below, I’ll explain why Opendoor has multibagger potential and what might hinder investors from realizing massive success.

A massive market

If you’ve ever bought or sold a home, you know how frustrating it is. It’s a cumbersome, stressful process with many steps along the way. Opendoor seeks to change that with a business model based on what’s known as iBuying.

Opendoor’s iBuying idea involves having the company buy and resell homes directly with customers, using technology to deliver a faster, more convenient process. Sellers can quickly get a cash offer on Opendoor, and buyers can easily access inventory and even enter contracts by pointing and clicking at a home on Opendoor’s marketplace.

The U.S. real estate market is enormous. The cumulative value of U.S. homes is nearly $50 trillion, and more than 6 million homes change hands each year. The great thing about such a big market is that Opendoor, with its small market cap of $2 billion today, only needs to take a small piece of the market to do very well.

Limited competition

The opportunity is even more apparent when considering Opendoor’s lack of competition. It wasn’t always this way. The iBuying category was hot in 2020 and 2021, featuring competitors like Redfin and Zillow. However, both companies struggled with iBuying economics and abandoned the business altogether.

Today, Opendoor is partners with these former competitors. The company provides cash offers on request, making Redfin and Zillow traffic sources to get more eyeballs on Opendoor.

NAR Settlement

Recently, a significant splash in the housing industry came from a class-action lawsuit against the National Association of Realtors (NAR). The suits resulted in a settlement proposal that abolished the mandatory 6% commission on home sales on the Multiple Listing Service (MLS), the primary network on which most realtors list homes.

Opendoor applauded the settlement, pointing out in a corporate blog post that the settlement greases the wheels for Opendoor to compete more by:

-

encouraging more frequent housing transactions due to lower commissions

-

lowering transaction costs as competition pushes commission take rates lower

-

direct sales, as the MLS becomes less a powerful tool

This potentially opens the door for a third-party disruptor like Opendoor, which can use its size and deep pockets to compete against the traditional agent model.

The risk that could ruin it all

Opendoor buys and resells homes, which means it has to accurately predict (within a certain margin) what it can buy and sell a home for to make money on the difference. The company uses artificial intelligence (AI) and machine learning to craft most of its offers.

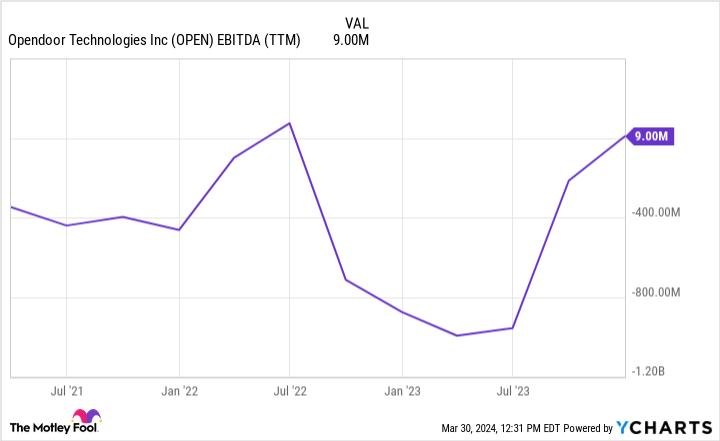

The housing market experienced a shock when the Federal Open Market Committee (FOMC) began aggressively hiking interest rates in 2022. Surging mortgage rates quickly cooled housing prices in many key markets, and Opendoor, which had been aggressively buying houses to grow, was left holding the bag on inventory it had to sell at steep losses:

This hiccup ultimately drove the company’s competition out of the game. Opendoor didn’t come out unscathed, either. It had to reset and scale back growth, and the company’s founder stepped down. Long story short: Embracing iBuying when Opendoor did proved to be a very costly mistake.

For as much potential as Opendoor has, the business can’t afford to make another bad misstep. Investors can see that earnings before interest, taxes, depreciation, and amortization (EBITDA) has recovered. The new challenge? Profitably grow the business from here.

Now, as one of the last remaining players in iBuying, Opendoor could have the potential to create life-changing investment returns. However, it could just as quickly fail. This binary outcome is what makes stocks like Opendoor so lucrative.

However, given the risks, investors should act cautiously and consider making Opendoor a tiny part of a diversified portfolio. You won’t need a lot of stock, anyway, if Opendoor succeeds over the long term.

Should you invest $1,000 in Opendoor Technologies right now?

Before you buy stock in Opendoor Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Opendoor Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $539,230!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 4, 2024

Justin Pope has positions in Opendoor Technologies. The Motley Fool has positions in and recommends Opendoor Technologies, Redfin, and Zillow Group. The Motley Fool recommends the following options: short May 2024 $8 calls on Redfin. The Motley Fool has a disclosure policy.

Should Investors Buy This Potential Multibagger Stock Before the Train Leaves the Station? was originally published by The Motley Fool