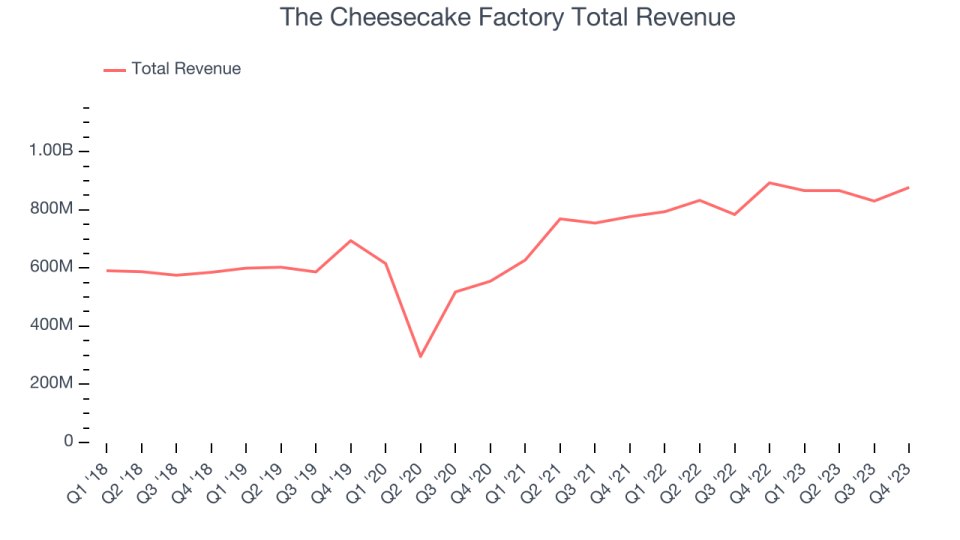

Restaurant company Cheesecake Factory (NASDAQ:CAKE) reported results in line with analysts’ expectations in Q4 FY2023, with revenue down 1.8% year on year to $877 million. It made a non-GAAP profit of $0.80 per share, improving from its profit of $0.56 per share in the same quarter last year.

Is now the time to buy The Cheesecake Factory? Find out by accessing our full research report, it’s free.

The Cheesecake Factory (CAKE) Q4 FY2023 Highlights:

-

Revenue: $877 million vs analyst estimates of $876.2 million (small beat)

-

EPS (non-GAAP): $0.80 vs analyst estimates of $0.73 (9.5% beat)

-

Gross Margin (GAAP): 41.8%, up from 39.6% in the same quarter last year

-

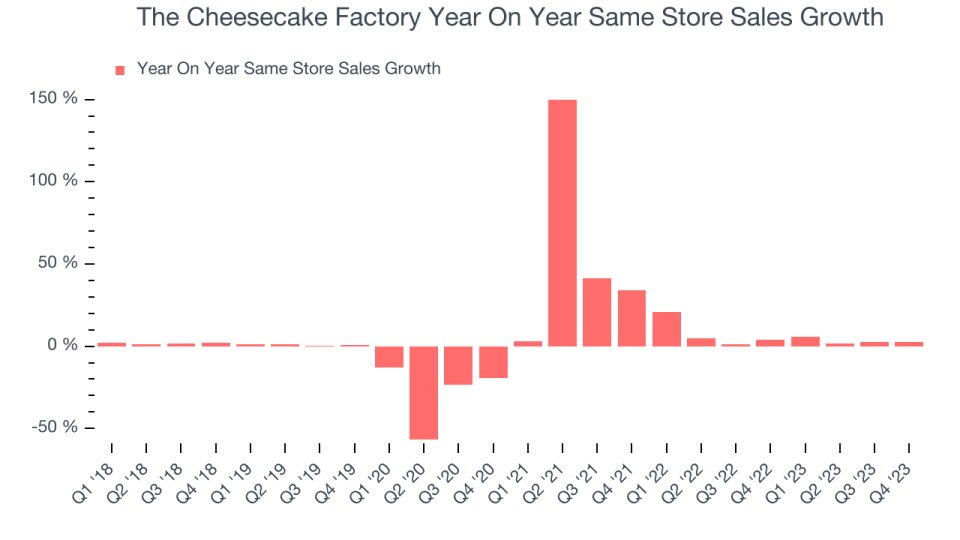

Same-Store Sales were up 2.5% year on year

-

Store Locations: 331 at quarter end, decreasing by 17 over the last 12 months

-

Market Capitalization: $1.76 billion

“Our fourth quarter results marked a strong finish to the year, with positive comparable sales growth and margin expansion contributing to record annual revenue and solid earnings growth for the year,” said David Overton, Chairman and Chief Executive Officer.

Celebrated for its delicious (and free) brown bread, gigantic portions, and delectable desserts, Cheesecake Factory (NASDAQ:CAKE) is an iconic American restaurant chain that also owns and operates a portfolio of separate restaurant brands.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

The Cheesecake Factory is one of the larger restaurant chains in the industry and benefits from a strong brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company’s annualized revenue growth rate of 8.5% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new restaurants and grew sales at existing, established dining locations.

This quarter, The Cheesecake Factory reported a rather uninspiring 1.8% year-on-year revenue decline to $877 million in revenue, in line with Wall Street’s estimates. Looking ahead, Wall Street expects sales to grow 6.4% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Same-store sales growth is an important metric that tracks organic growth and demand for a restaurant’s established locations.

The Cheesecake Factory’s demand within its existing restaurants has generally risen over the last two years but lagged behind the broader sector. On average, the company’s same-store sales have grown by 5.4% year on year. With positive same-store sales growth amid an increasing number of restaurants, The Cheesecake Factory is reaching more diners and growing sales.

In the latest quarter, The Cheesecake Factory’s same-store sales rose 2.5% year on year. This growth was a deceleration from the 4.1% year-on-year increase it posted 12 months ago, showing the business is still performing well but lost a bit of steam.

Key Takeaways from The Cheesecake Factory’s Q4 Results

We were impressed by how significantly The Cheesecake Factory blew past analysts’ gross margin expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street’s estimates. Although its same-store sales growth of 2.5% wasn’t anything to write home about, the company opened 9 new company-owned restaurants (three Cheesecake Factories, three North Italias, three FRCs) and opened two Cheesecake Factory restaurants in China and Thailand under licensing agreements. Since 12/31/23, The Cheesecake Factory has also opened four new Cheesecake Factory restaurants under licensing agreements in Mexico. Overall, we think this was a really good quarter that should please shareholders. The stock is up 1.9% after reporting and currently trades at $34.88 per share.

The Cheesecake Factory may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.