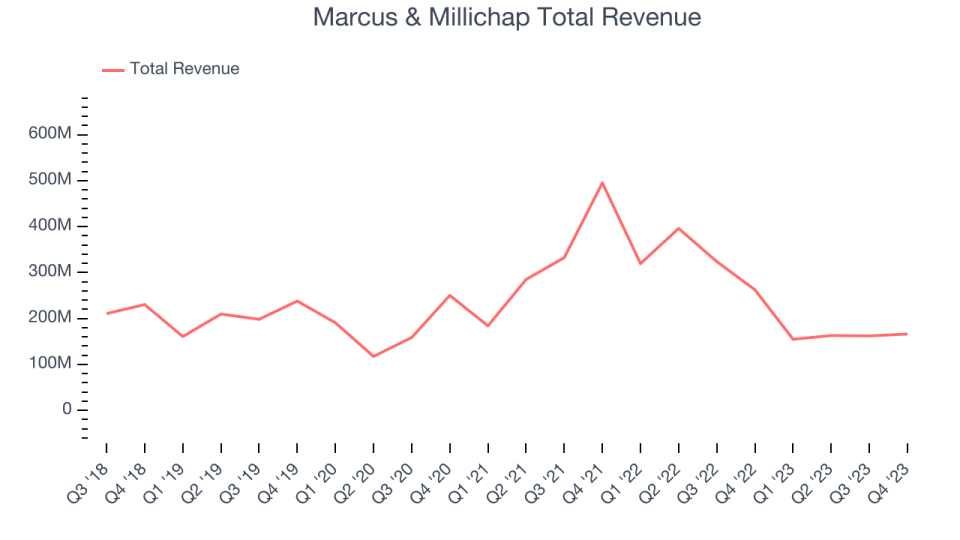

Real estate brokerage and services firm Marcus & Millichap (NYSE:MMI) fell short of analysts’ expectations in Q4 FY2023, with revenue down 36.7% year on year to $166.2 million. It made a GAAP loss of $0.27 per share, down from its profit of $0.19 per share in the same quarter last year.

Is now the time to buy Marcus & Millichap? Find out by accessing our full research report, it’s free.

Marcus & Millichap (MMI) Q4 FY2023 Highlights:

-

Revenue: $166.2 million vs analyst estimates of $171.2 million (2.9% miss)

-

EPS: -$0.27 vs analyst estimates of -$0.28 ($0.01 beat)

-

Gross Margin (GAAP): 36.6%, up from 31.1% in the same quarter last year

-

Market Capitalization: $1.53 billion

Founded in 1971, Marcus & Millichap (NYSE:MMI) specializes in commercial real estate investment sales, financing, research, and advisory services.

Real Estate Services

Technology has therefore been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. Marcus & Millichap’s revenue declined over the last five years, dropping 5.7% annually.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That’s why we also follow short-term performance. Marcus & Millichap’s recent history shows its demand has decreased even further, as its revenue has shown annualized declines of 29.4% over the last two years.

This quarter, Marcus & Millichap missed Wall Street’s estimates and reported a rather uninspiring 36.7% year-on-year revenue decline, generating $166.2 million of revenue. Looking ahead, Wall Street expects sales to grow 33.5% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

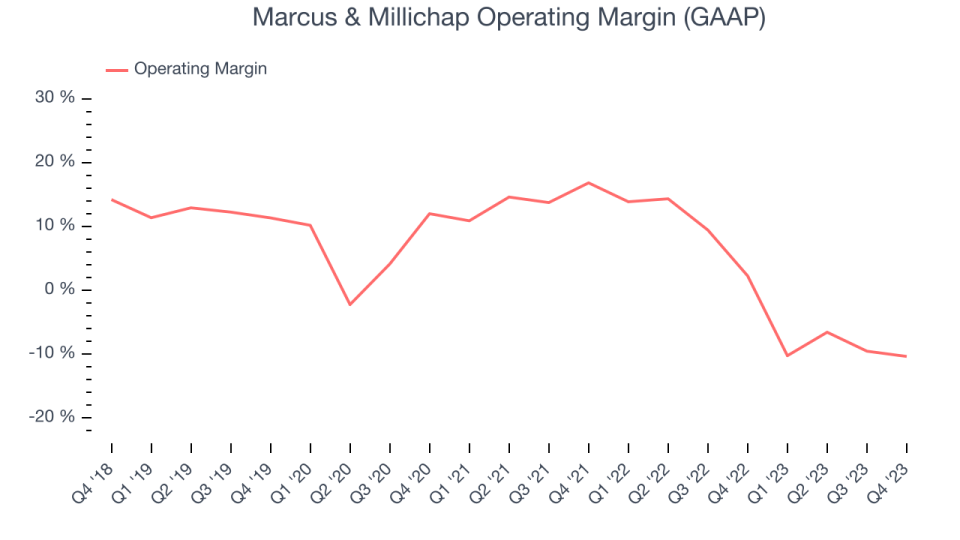

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Marcus & Millichap was profitable over the last two years but held back by its large expense base. Its average operating margin of 4% has been paltry for a consumer discretionary business.

In Q4, Marcus & Millichap generated an operating profit margin of negative 10.3%, down 12.6 percentage points year on year.

Over the next 12 months, Wall Street expects Marcus & Millichap to become profitable. Analysts are expecting the company’s LTM operating margin of negative 9.2% to rise to positive 2.6%.

Key Takeaways from Marcus & Millichap’s Q4 Results

It was encouraging to see Marcus & Millichap slightly top analysts’ EPS expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue unfortunately missed and its operating margin fell short of Wall Street’s estimates. Management added that results “reflect the ongoing market disruption created by the Fed’s fight against inflation and persistent interest rate volatility impacting real estate valuations”. Overall, the results could have been better and the macro is highly uncertain for the company. The stock is flat after reporting and currently trades at $39.96 per share.

So should you invest in Marcus & Millichap right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.