(Bloomberg) — Luxury giant LVMH SE and Nordic telecommunication archrivals Ericsson AB and Nokia Oyj are set to usher in the first-quarter reporting season this week.

Most Read from Bloomberg

Last month’s shock warning by Kering SA set a worrying tone for LVMH and beauty specialist L’Oreal SA as fears of a pullback in Chinese consumer spending pressure luxury stocks. L’Oreal warned in February that the Chinese market probably won’t be “over-dynamic” in the first half of 2024.

“A sales growth recovery in the first half of 2023 and extended uncertainty over China spending make for a challenged start to 2024 for the luxury goods industry,” said Bloomberg Intelligence senior industry analyst Deborah Aitken.

Cost cuts will be paramount for Ericsson and Nokia, who have struggled to rebound from a slowdown in spending across the mobile services industry.

Dutch semiconductor equipment maker ASML Holding NV is likely to reveal slowing orders of its chip-making machines after the previous quarter’s record. EssilorLuxottica SA, the Italo-French maker of Ray Ban and Oakley glasses, also reports.

Results and guidance from European companies “need to reverse faltering EPS momentum by signaling a rebound in second-half earnings growth capable of underpinning equity valuations at a two-year high,” BI’s Laurent Douillet and Kaidi Meng said.

Highlights to look out for:

Monday: No major earnings of note

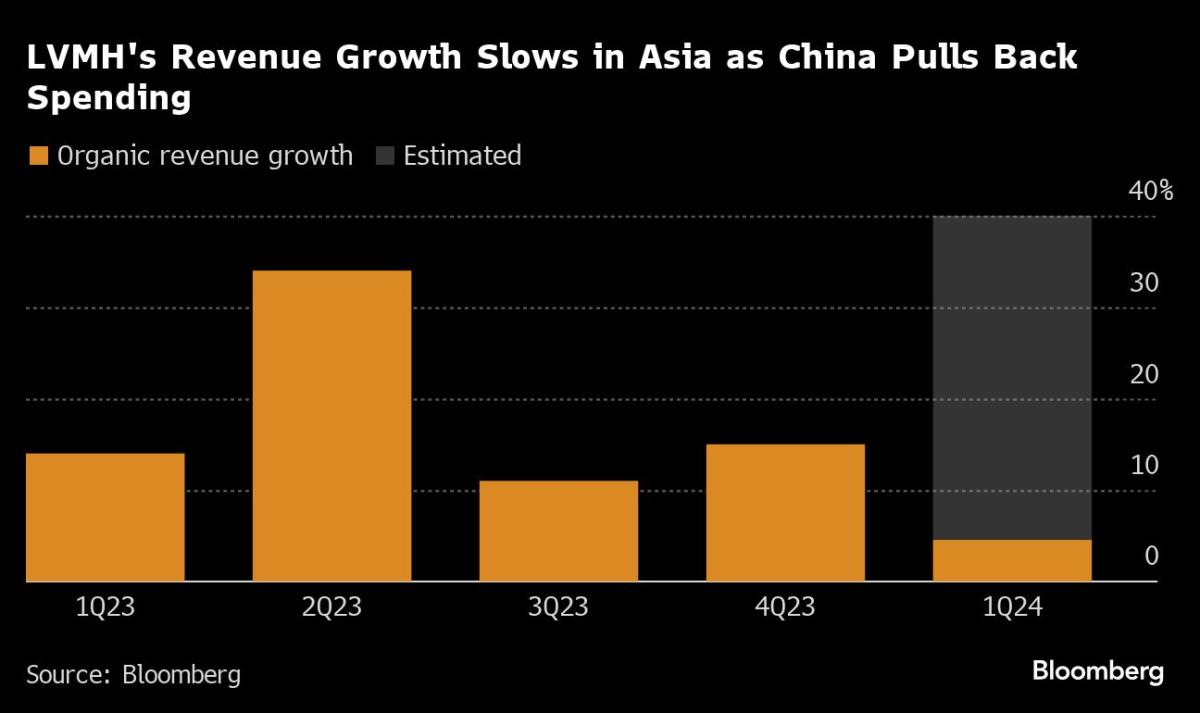

Tuesday: LVMH’s (MC FP) brand breadth could act as a shield as growth rates in the sector normalize this year, BI’s Aitken said. Consensus points to flat sales at the group level in the first quarter, with organic growth in fashion and leather goods seen slowing to 3.2% from 18% a year ago. Growth in Asia excluding Japan is estimated to have slowed to 4.1% from 14%, while sales growth in the US probably decelerated to 3% from 8%. Management will probably stick to the “cautious though positive tone” it adopted in January, Aitken said.

-

Ericsson’s (ERICB SS) adjusted Ebit is seen dropping 55% year-on-year in the first quarter, after the Swedish mobile networks maker warned of a challenging start to 2024 in its previous report. While margin expectations may be too high, this shouldn’t prompt any “material revisions” of full-year guidance, Barclays analysts said. Analysts at SEB see a risk of “another guidance disappointment,” with consensus already factoring in a better US market and mix in the second quarter. Its deal with AT&T may still surprise on the upside in the second half, they said.

Wednesday: ASML’s (ASML NA) order book should be solid, though well short of the blowout €9.2 billion of the fourth quarter. The company’s electric ultraviolet machines are likely to face slowing sales growth and lower margins in 2024 before a recovery in 2025, with first-quarter EUV revenue expected to be down more than 40%, consensus shows. At the same time, underlying tool demand from China should have remained robust, and market share shouldn’t be disrupted by the emergence of a local rival supplier this year, according to Morgan Stanley analysts.

Thursday: L’Oreal’s (OR FP) sales in North Asia will be key in its update, after a challenging travel retail market hampered the French cosmetics group’s performance in the region last year. Like-for-like sales for the quarter ended March 31 are seen up 6.6%, with growth in North Asia seen slipping 2.4%, consensus shows. The dermatological beauty division, which includes skincare brand La Roche-Posay, could be a bright spot, with expected like-for-like sales growth of 20%.

-

EssilorLuxottica’s (EL FP) update will shed further light on the health of the luxury sector. First-quarter sales growth may be limited given the still challenging macro environment, HSBC analyst Anne-Laure Bismuth said. Short-term visibility remains “blurred,” she wrote, after recently downgrading her rating on the stock to hold from buy. BI’s Diana Gomes said “a significant pickup is feasible in 2024,” pointing to a “strong price mix” and efficiency gains from the rollout of the AI-powered Varilux XR lens.

-

In contrast to Ericsson, Nokia (NOKIA FH) may beat on margin estimates for the quarter, though that’s also unlikely to spark a major revision in the full-year forecast, according to Barclays. The Finnish vendor to telecom operators may report a revenue decline of about 16% for the first three months of 2024, consensus shows. Investors will be looking for signs of a network infrastructure revival, which seems to be priced in for the second half, though there’s no evidence supporting this yet, the analysts said.

Friday: No major earnings of note

–With assistance from Christopher Jungstedt, Valentine Baldassari, Jenny Che, Charlotte Hughes-Morgan, James Cone, Jonas Ekblom and Cagan Koc.

(Updates with comments from Bloomberg Intelligence in seventh paragraph)

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.