-

The soaring stocks’ growing gap with the Fed’s continued pushback on interest rate cuts should be worried, says JPMorgan.

-

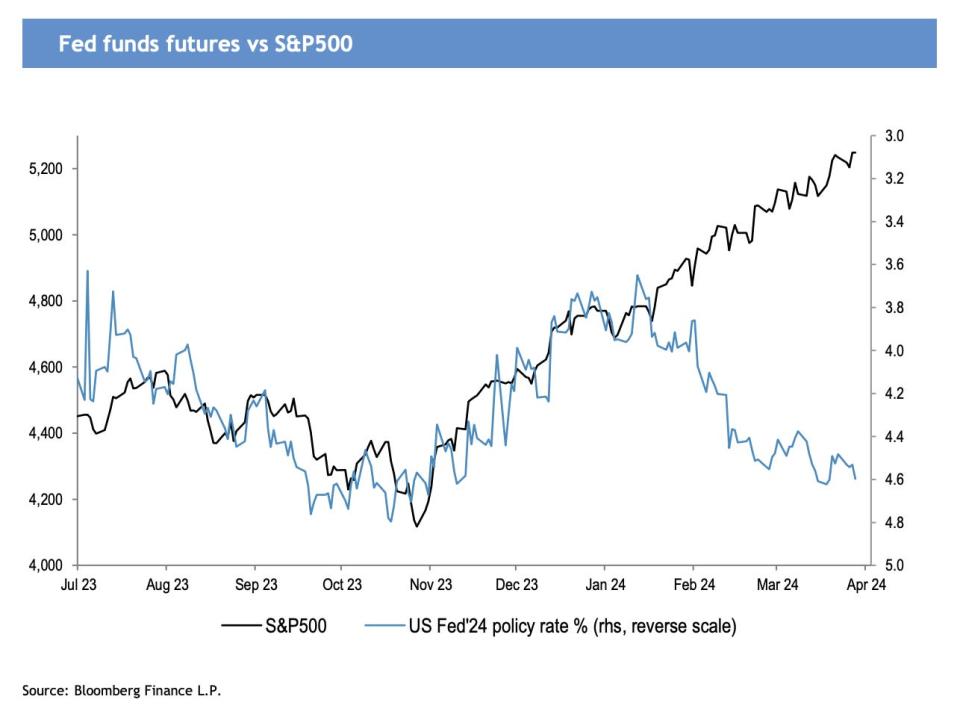

Rate-cut expectations have snapped back to 80 bps, reminiscent of last October’s downturn in the stock market.

-

Analysts highlighted anticipated market growth in the second half of the year, but warned against assuming this will lift earnings projections for 2025.

The fact that stocks are continuing to set new records amid signs of delayed interest-rate cuts is cause for concern, says JPMorgan.

In research sent to clients on Tuesday, JPMorgan’s Mislav Matejka and his team noted that stocks have soared 30% since last October’s nadir, which was largely fueled by anticipations of an interest rate cut in March. However, three months later, these projections have been pushed out considerably.

Taking a closer look, Wall Street initially priced in an 80-basis-point rate cut by the Fed during the October downturn. When the market surged, expectations were revised to 180 bps in January at peak dovishness. Now, those predictions have recalibrated back to 80 bps.

“Equities are ignoring the most recent pivot of a pivot, which might be a mistake,” analysts wrote in the note, adding that corporate earnings will need to pick up speed to plug the gap.

JPMorgan also sees bond yields heading south in the second half of the year, but there’s also an uptick in inflation swaps – which might further delay a rate cut. Combined with less-than-expected returns for bonds again, it flags “a lot of complacency in the bond market with respect to the inflation risk.”

The AI-driven tech stocks have powered the S&P 500 to reach waves of rallies in 2024. Meanwhile, inflation on the rise has sparked the Fed to push first rate cut expectations from March to June. Despite this, some analysts predicted less than 50% chance for a June cut due to the latest inflation indexes.

Matejka’s team further pointed out that there’s an assumption of market growth in the latter half of the year, but this doesn’t mean earnings projections for 2025 would move up.

On top of that, they highlighted the market’s alarming complacency towards downside risks, with recession odds at a mere 7th percentile, likely underestimated. Plus, the surge in cyclicals and defensives mirrors levels seen during the post-Global Financial Crisis recovery in 2009-2010, signaling potential overallocation.

“That is unlikely to be the template this time around, and could act as a headwind. The next time bond yields fall we do not believe the market will have as positive a reaction as it did in Nov-Dec – we might revert to a more traditional correlation between yields and equities,” the team added.

Read the original article on Business Insider