(Bloomberg) — The sharp rally in US stocks this year has left strategists at JPMorgan Chase & Co. and Goldman Sachs Group Inc. divided about whether a market bubble is forming.

Most Read from Bloomberg

To JPMorgan’s chief market strategist Marko Kolanovic, the dramatic rally in US equities and Bitcoin’s quick surge above the $60,000 mark signal yes. He sees those advances as indicative of accumulating froth in the market — conditions that typically precede a bubble when asset prices rise at an unsustainable pace.

He joins in a chorus of rapidly piling up warnings from Wall Street that are hearkening back to the dot-com boom of the late-1990s, or the post-pandemic mania of 2021, when stock prices quickly ballooned and then burst.

Meanwhile, David Kostin at Goldman Sachs is among those who thinks the risk-on mood is warranted, arguing Big Tech’s lofty valuations are supported by fundamentals.

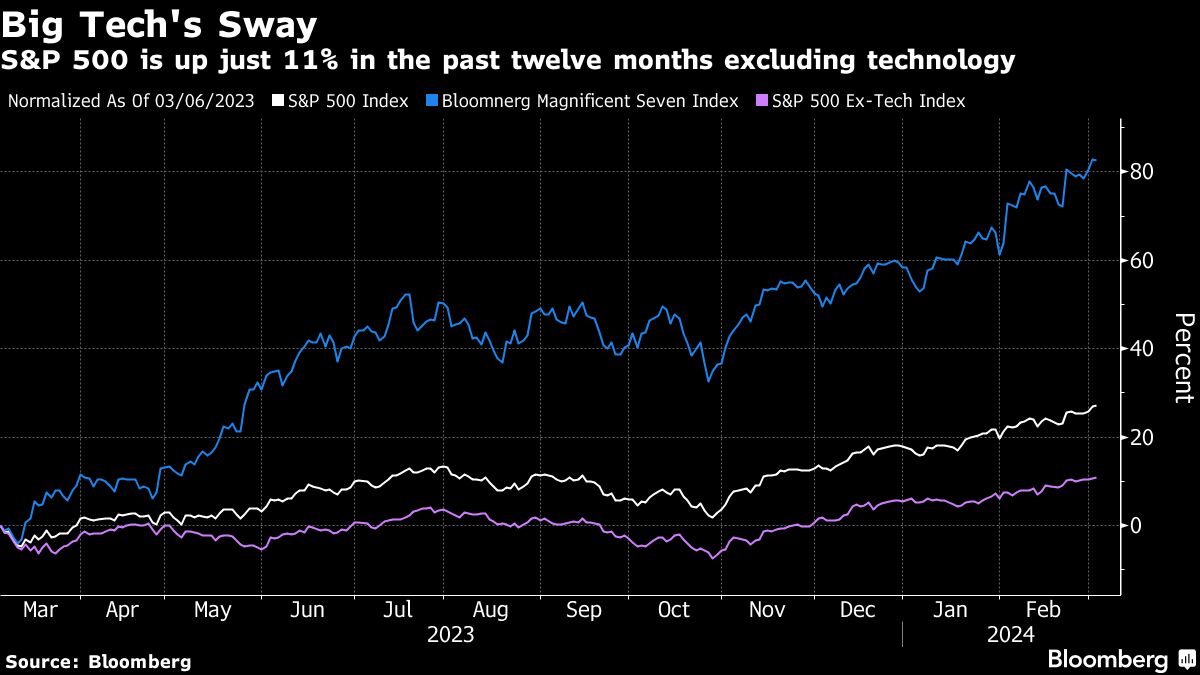

As the S&P 500 Index keeps hitting new highs — driven chiefly by big gains in American technology giants — it’s drawn the ire of critics who think the bullish run can’t last, and excitement from optimists who think there’s room for more gains.

Kolanovic is a key figure in the former group. The market is pushing ahead “with volatility low and froth building,” he wrote Monday in a note to clients.

“Equities have moved up this year, even as bond yields rose and rate cut expectations unwound,” he said. “Investors may be assuming that the increase in yields is reflective of economic acceleration, but earnings projections for 2024 are coming down and the market appears too complacent on the cycle.”

S&P 500 futures dropped 0.2% while Nasdaq 100 futures fell 0.4% at 3 a.m. in New York on Tuesday, putting the underlying benchmarks on track for a second day of losses.

In contrast, Goldman’s Kostin said this time is different from other periods in history when stock prices have moved abruptly, typically beyond their value. Unlike prior such instances, the breadth of “extreme valuations” is far more contained this time, with the number of stocks trading at those multiples down sharply from the peak in 2021.

Moreover, in contrast to the “growth at any cost” mentality in 2021, “investors are mostly paying high valuations for the largest growth stocks in the index,” he wrote in a note Friday. “We believe the valuation of the Magnificent 7 is currently supported by their fundamentals.”

The group, particularly Nvidia Corp., Meta Platforms Inc. and Microsoft Corp., have raced ahead this year and pulled major stock indexes along with them. The S&P 500 has logged 15 closing records in 2024, posting four-straight months of gains.

So far, financial results are justifying the moves. Earnings per share for the cohort rose a combined 59% in the fourth quarter from a year earlier, compared with expectations of 47%, data compiled by Bloomberg Intelligence show.

But to Kolanovic, the environment is a head-scratcher, reflecting investor complacency and an underappreciation of risk.

The continued climb in stocks “may keep monetary policy higher for longer, as premature rate cutting risks further inflating asset prices or causing another leg up in inflation,” he said.

—With assistance from Farah Elbahrawy.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.