After a huge one-year rally, share prices of Zscaler (NASDAQ: ZS) have hit some bumps in the road. That’s not to say the cloud-native cybersecurity leader is performing poorly, though.

On the contrary, the company is doing quite well, although its growth does continue to moderate. I remain optimistic for Zscaler and its cloud security peers, but is this still a top cybersecurity stock buy for 2024 and beyond?

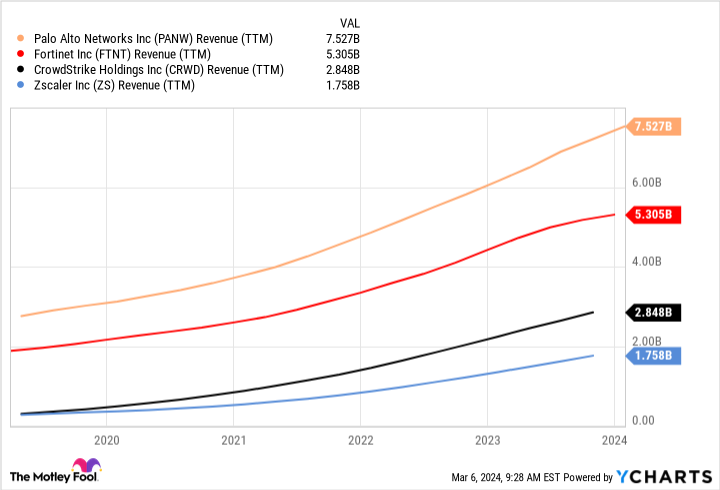

Is a top Zscaler competitor a threat?

Let’s start this discussion by acknowledging the changes that top cybersecurity pure play and Zscaler competitor Palo Alto Networks (NASDAQ: PANW) just announced. CEO Nikesh Arora explained a new go-to-market strategy during the last quarterly update, stating that Palo Alto would be giving away security products and services over the next year or so until customer contracts with competing security companies expire. It’s a type of price war, so to speak, that will temporarily reduce Palo Alto’s growth rate.

Zscaler CEO Jay Chaudhry doesn’t think this will work. But although Zscaler and Palo Alto do overlap in security offerings, the latter works at the convergence of traditional network hardware and newer cloud-based services. Zscaler’s services converge all network traffic into one cloud-based service, and it secures access via zero trust (which continuously verifies users’ identities, like via password and two-factor authentication).

In other words, while Zscaler is going head-to-head with Palo Alto, both companies can coexist and thrive, given the different customer needs they address.

At any rate, Zscaler stock fell after the most recent report on its slowing growth outlook. As I wrote about last year, a slowdown was always to be expected, and not because of Palo Alto’s new aggressive strategy in the cybersecurity market. Zscaler is getting larger, and as it does, its pace of expansion will naturally moderate. Management itself has been indicating this would happen all along.

|

Period |

Zscaler Revenue |

Growth (YOY) |

|---|---|---|

|

Full fiscal 2022 |

$1.091 billion |

62% |

|

Full fiscal 2023 |

$1.617 billion |

48% |

|

Q1 fiscal 2024 |

$497 million |

40% |

|

Q2 fiscal 2024 |

$525 million |

35% |

|

Q3 fiscal 2024 outlook |

$534 million to $536 million |

About 28% |

|

Full fiscal 2024 outlook* |

$2.118 billion to $2.122 billion |

About 31% |

Data source: Zscaler. Note: Full fiscal 2024 is the 12 months ending in July 2024. YOY = year over year.

Growth is growth, though, so we can’t discount Zscaler’s rapid move up the ranks too much. This has been a standout winner in the cybersecurity market, and it now ranks among the largest pure plays for enterprise security software as measured by revenue.

Is Zscaler the best cybersecurity stock around?

The rate of expansion aside, some investors still aren’t going to like what they see at Zscaler. It still operates at a net loss. Under generally accepted accounting principles (GAAP), operating and net losses were at a respective $45.5 million and $28.5 million last quarter (the second quarter of fiscal 2024, ended in January).

Granted, Zscaler is gradually homing in on GAAP breakeven, and has been generating adjusted profitability and positive free cash flow (FCF) for some time. FCF in the last quarter was $101 million, a 19% FCF profit margin.

Most of the discrepancy between the GAAP metrics remains employee stock-based compensation (SBC), including stock awards for Chaudhry (combined, the family still owns about 35% of shares outstanding).

Despite a high rate of SBC, though, Zscaler continues to exceed expectations in growing FCF on a per-share basis.

The only problem is that Zscaler does still trade for a high premium of about 68 times trailing-12-month FCF as of this writing. This premium has stayed elevated throughout the last year, despite overall growth continuing to slow.

Zscaler cannot be ignored as a top player in the cybersecurity world. But given the high price and inherent volatility in the stock — on display in the wake of the recent earnings update — investors should consider using dollar-cost averaging to build a position over time. I for one am content owning shares of Palo Alto Networks, Fortinet, and CrowdStrike for the time being.

Should you invest $1,000 in Zscaler right now?

Before you buy stock in Zscaler, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Zscaler wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 8, 2024

Nicholas Rossolillo and his clients have positions in CrowdStrike, Fortinet, and Palo Alto Networks. The Motley Fool has positions in and recommends CrowdStrike, Fortinet, Palo Alto Networks, and Zscaler. The Motley Fool has a disclosure policy.

Is Zscaler Stock Still a Top Cybersecurity Buy for 2024? was originally published by The Motley Fool