With over 1.4 million paying customers, DocuSign (NASDAQ: DOCU) is the largest e-signature company in the world. It’s estimated to hold a nearly 68% share of the e-signing market.

Even so, its stock is currently well below the 52-week high of $66.98 achieved last March, and down from the more than $60 per share reached in January. The current dip in share price could be a buying opportunity, or a signal to avoid the company. To know which, you have to examine what’s going on with DocuSign in more detail.

And now is a good time to do so, since DocuSign is scheduled to release fiscal fourth-quarter earnings on March 7. So let’s dive into the company to determine if it’s a worthwhile investment.

DocuSign’s sales success

DocuSign shares shot up toward the end of 2023 and into 2024 because of news reports that the company was in talks to be acquired. However, no such deal appears to be happening at this time. As a result, DocuSign stock dropped.

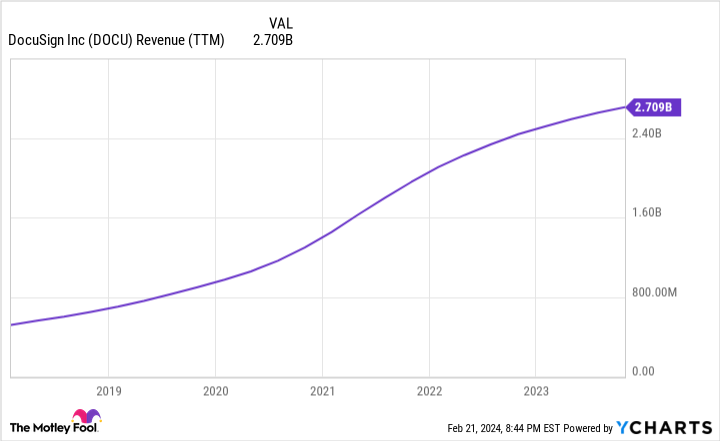

Acquisition rumors aside, DocuSign’s ability to successfully grow its business is what can drive its share price higher over the long run. The company’s sales hit $700.4 million in its fiscal third quarter, ended October 31, representing 9% year-over-year growth. DocuSign’s revenue has been on an upward trajectory since its 2018 IPO.

The company’s sales gains are expected to continue. DocuSign forecasted fiscal Q4 revenue of at least $696 million, an increase over the prior year’s $659.6 million.

Along with revenue growth, DocuSign exited Q3 with net income of $38.8 million. This is a dramatic turnaround from the previous year’s $29.9 million net loss.

In fact, through three quarters of fiscal 2024, DocuSign’s net income was at $46.7 million, compared to a net loss of $102.3 million in the year-ago period. So it’s looking like this could be DocuSign’s first year as a profitable company since its founding in 2003.

That’s a major milestone, and it happened after DocuSign brought on Allan Thygesen, a former executive at Alphabet‘s Google, as CEO in September of 2022. In just a year, he helped bring financial health to DocuSign.

DocuSign’s transformation under its new CEO

When he took over the CEO spot, Mr. Thygesen acknowledged DocuSign “didn’t fully address the changing market dynamics, nor mature our operations and systems sufficiently” in response to the huge demand for online services generated by the COVID-19 pandemic’s lockdowns, which dropped off after those lockdowns were removed.

But he has a vision for the company that holds promise and seems achievable. He stated, “We see opportunities beyond the replacement of paper signatures to deliver innovative new experiences and to integrate more deeply with partner applications.”

To that end, DocuSign announced a partnership with Facebook parent Meta last November, and continues to deepen its relationship with Microsoft by expanding its e-signature integrations to more products, most recently to Microsoft Power Pages.

Mr. Thygesen mentioned “innovative new experiences,” and one of these involves contract lifecycle management (CLM). With CLM, DocuSign’s platform handles the entire workflow around business contracts digitally, including document creation and routing contracts for necessary approvals and reviews.

CFO Blake Grayson noted that the company’s CLM business saw year-over-year double-digit growth in Q3, although DocuSign doesn’t release financial details specific to CLM.

To buy or not to buy DocuSign

Under Allan Thygesen, DocuSign generated record free cash flow (FCF) in Q3, reaching $240.3 million, a significant increase from the prior year’s $36.1 million. FCF provides insight into the cash available for DocuSign to invest in its business, pay debt obligations, and repurchase shares. Its strong FCF results allowed the company to buy back 1.8 million shares in Q3.

DocuSign also exited the quarter with a solid balance sheet. Its Q3 total assets were $3.3 billion, compared to $2.4 billion in total liabilities. Its cash and equivalents alone were $1.2 billion.

From a financial perspective, DocuSign is delivering solid results under Mr. Thygesen. Moreover, DocuSign stock’s average price target among Wall Street analysts is $59.77, indicating some upside potential from where the stock is at currently.

When you take these factors into consideration, along with the impressive results achieved with Allan Thygesen at the helm and the stock’s recent price drop, now looks like a good time to buy DocuSign shares.

Should you invest $1,000 in DocuSign right now?

Before you buy stock in DocuSign, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DocuSign wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Robert Izquierdo has positions in Alphabet, DocuSign, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, DocuSign, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Is Now the Time to Buy DocuSign Stock? was originally published by The Motley Fool