Boeing (NYSE: BA) is, by far, the worst-performing stock in the Dow Jones Industrial Average so far in 2024. It is also one of just two stocks in the Dow that don’t pay dividends, the other being Salesforce.

Boeing shareholders are hoping the business can turn around and resume paying and growing its dividend. But in the meantime, there are other quality dividend stocks that have sold off but are still maintaining or even increasing their payouts. Here’s why Boeing, California Water Service Group (NYSE: CWT), and Deere (NYSE: DE) are worth buying now.

There’s a value case for buying Boeing stock

Lee Samaha (Boeing): The troubles at aerospace giant Boeing continue. Suppose it isn’t supply chain difficulties challenging its ability to ramp up airplane production in line with its medium-term plans. In that case, manufacturing quality issues and the need for a Federal Aviation Administration (FAA) audit into Boeing and its fuselage supplier Spirit AeroSystems production have the same impact.

With all that said, despite all its difficulties, Boeing is still winning orders and has a backlog of almost 5,600 airplanes. It’s not a question of if Boeing will deliver on the backlog, but more of a question of when and with how much profit margin.

Boeing’s plan, outlined on its investor day in November 2022, is to ramp up its 737 production rate to 50 planes a month and its 787 production rate to 10 airplanes a month in 2025 and 2026. In doing so, Boeing plans to hit $10 billion in free cash flow (FCF) in the time period.

While recent events have probably pushed back the date it will hit the $10 billion FCF level within that window, Wall Street still thinks Boeing will do so by the end of 2026. With the company’s market cap down by more than 23% in 2024 to $122 billion, there’s a value case to be made for the stock. While I think there are better ways to invest in the sector than buying Boeing, the stock will still interest value investors.

Now’s a good time to dip your toes into California Water Service Group

Scott Levine (California Water Service Group): Shares of California Water Service have plunged by about 11% since the start of the year. The third-largest regulated water utility by market capitalization, California Water Service has fallen out of favor with investors due to the uncertainty regarding its 2021 General Rate Case and a disappointing fourth-quarter 2023 earnings report. While unwelcome, these two factors should hardly be sufficient to dissuade income investors from picking up shares of California Water Service, which at their current price sport a 2.4%-yielding dividend — especially given the company’s track record of rewarding investors.

Regulated water utilities can’t arbitrarily start charging customers more whenever they see fit. They must instead undergo General Rate Cases — formal proceedings under which they request permission from the relevant public utility commissions and regulators to charge higher rates. It’s understandable, therefore, that investors are frustrated with the lack of clarity regarding the California Public Utilities Commission’s view of the company’s 2021 General Rate Case. Given their lack of confidence that the company will be allowed to charge higher rates, investors are likely concerned that management doesn’t have the same insight into its future cash flows, a factor that may affect the company’s ability to sustain its dividend.

But this isn’t California Water Service’s first rodeo. Founded in 1926, the company has an impressively long track record of annual dividend hikes: 56 straight years, a streak that makes it a Dividend King. Surely, the company has faced uncertainty regarding General Rate Cases before, and, despite this, management’s prowess at navigating turbulent waters has still left the company able to raise the dividend every year. That record of past performance provides no guarantee that it will continue hiking its payout annually in the future, but it does inspire confidence that management will be able to navigate the current challenges.

With shares valued at 13 times operating cash flow, just below its 5-year average cash flow multiple of 13.1, now seems like a great time to pick up shares of California Water Service.

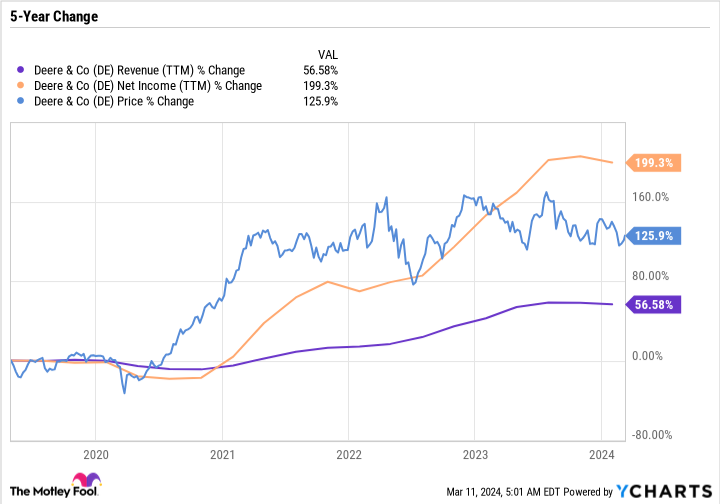

Deere is entering a slowdown, but the future is bright

Daniel Foelber (Deere): It’s been a rough start to the year for Deere. The stock is down more than 6% year to date and has gone practically nowhere for the last three years. But zoom out a bit further, and you’ll see that Deere has delivered explosive growth over the last five years, including tripling its net income.

A lot of the stock’s gains came in 2020 and the first half of 2021. But the earnings growth came in the years that followed. Deere’s recent performance illustrates why cyclical stocks can sometimes behave strangely.

Orders were flooding in for Deere’s products. The business was booming. But over the last couple of quarters, its top line went flat and then started to slightly decline. For example, in its fiscal 2024 Q1 (which ended Jan. 29), net sales fell 8% year over year. And diluted earnings per share fell 5%.

Even worse, Deere is forecasting fiscal 2024 net income of $7.5 billion to $7.75 billion. For context, it earned a record $10.2 billion in its fiscal 2023 and $7.1 billion in its fiscal 2022. So the earnings are falling just as quickly as they rose.

Over the last few years, investors have grown accustomed to Deere beating expectations. Now, the opposite is true. When it delivered its fiscal 2023 Q4 report in late November, Deere forecast fiscal 2024 net income of $7.75 billion to $8.25 billion, which is above its updated range. Investors already expect earnings to decline, but the market hates surprises. Deere needs to find its footing and prove that this is just another slowdown.

The best cyclical companies have a way of notching higher lows and higher highs. In other words, the lowest year of earnings during each downturn is higher than the low during the previous cyclical downturn. And each expansion period contains new record highs. Deere has plenty of long-term growth ahead and is an underrated artificial intelligence (AI) company — it consistently commits a lot of capital to research and development to prepare for the next evolution of agriculture.

It has been a winning strategy to buy Deere when it begins to fall out of favor on Wall Street. And although management has prioritized growth over its stock repurchases and dividend payouts, the stock still has a respectable yield of 1.6% at the current price. Deere is the complete package, and long-term investors would do well to take a closer look at the stock now.

Should you invest $1,000 in Boeing right now?

Before you buy stock in Boeing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Boeing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Salesforce. The Motley Fool recommends Deere. The Motley Fool has a disclosure policy.

If You Like Boeing Stock Down 23.9% This Year, Then You’ll Love These 2 Dividend Payers was originally published by The Motley Fool