Sometimes good just isn’t good enough. That’s exactly what Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) investors can say after its latest results came out, as they were pretty good by most standards, yet the stock tumbled more than 7% following the report.

However, I think this represents a great buying opportunity, as investors aren’t seeing the full picture of how strong Alphabet’s business is.

Q4 was solid all around for Alphabet

Alphabet is better known by some brands underneath their umbrella — Google, YouTube, and Android are all Alphabet products. But there’s one key theme among its lineup: advertising.

Advertising revenue makes up 76% of Alphabet’s total, so as the ad market goes, so does Alphabet. In late 2022 and early 2023, this wasn’t a great business to be in, and Alphabet struggled. However, it has begun to recover, which resulted in Alphabet’s ad revenue increasing 11%. A key highlight in this division was YouTube, whose ad revenue increased by 16%. This shouldn’t be a surprise, as YouTube is the most popular streaming platform in terms of minutes viewed per day.

If ads do well, so does Alphabet. However, other stronger portions of the business are doing incredibly well but are just smaller, so they don’t sway the results as much.

One of those is Google Cloud, Alphabet’s cloud computing product. Cloud computing is becoming a vital part of infrastructure, as many businesses are switching their workloads to the cloud. Additionally, cloud computing is a key part of artificial intelligence (AI), as it allows companies to gather and store data easily and then use Google’s computing resources to create powerful AI models. Google Cloud is a popular choice for AI start-ups, and more than 70% of generative AI unicorns (private companies worth more than $1 billion) utilize Google Cloud.

Google Cloud’s revenue rose 26% in Q4 to $9.2 billion, with an operating margin of 9%. While this is below the companywide operating margin of 27%, Google Cloud is still building its infrastructure and is laser-focused on capturing market share instead of profits. This division should be able to achieve an operating profit margin of 30% when fully developed, so this segment will be a long-term boost to Alphabet.

There wasn’t anything wrong with Alphabet’s quarter, and with earnings per share rising from $1.05 in last year’s Q4 to $1.64 this year, everything appears to be healthy at Alphabet, which is why I think right now is a fantastic time to buy shares.

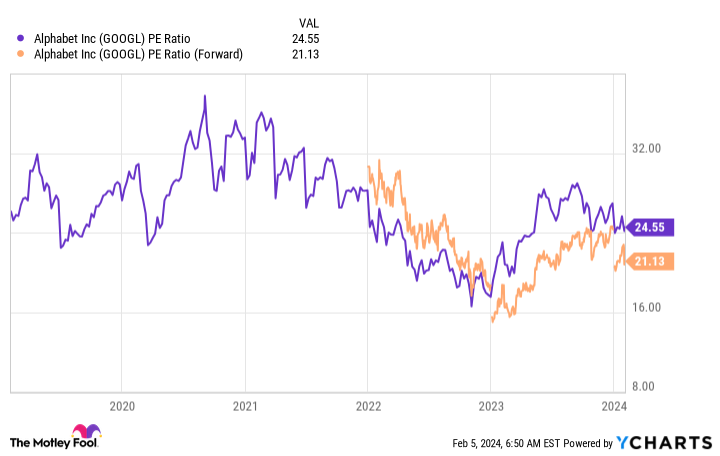

Alphabet is far cheaper than other tech giants

Compared to its big tech peers, Alphabet’s stock is cheap.

Not only is Alphabet cheaply priced compared to historical trends, but it’s also far cheaper than Microsoft (37 times trailing and 35 times forward earnings) and Apple (29 times trailing and 28 times forward earnings).

If Alphabet had the same valuation as Microsoft, it would be valued at $2.68 trillion — not far off of Microsoft’s $3.06 trillion valuation.

Alphabet is reasonably priced and slated to have another strong year. Unlike its peers, it doesn’t have a premium valuation, so you’re not at risk of overpaying. As a result, it’s one of the best stocks to buy right now despite what the stock price has done lately.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 5, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Microsoft. The Motley Fool has a disclosure policy.

Here’s Why I’m Buying the Dip on Alphabet’s Stock was originally published by The Motley Fool