(Bloomberg) — The gloomy mood of US consumers amid a surprisingly strong economy has befuddled many economists, but a paper by researchers from the IMF and Harvard University, including former Treasury Secretary Lawrence Summers, proposes that elevated borrowing costs may solve the mystery.

Most Read from Bloomberg

The paper argues that increases in the cost of living due to higher financing expenditures faced by consumers — which are not factored into inflation — underpin the recent divergence between official inflation data and consumer sentiment.

Quite simply, consumers are including the cost of money in their perspective on their economic health, while economists are not, the researchers found.

“The current methodology excludes a central part of consumers’ financial well-being,” they wrote.

By many measures the US economy is booming. Unemployment is historically low, and the number of jobs has increased every month since December 2020. On top of that, the inflation rate is cooling, and the economy is growing faster in the US than in most other large countries. Yet US consumer sentiment remains well below pre-pandemic levels.

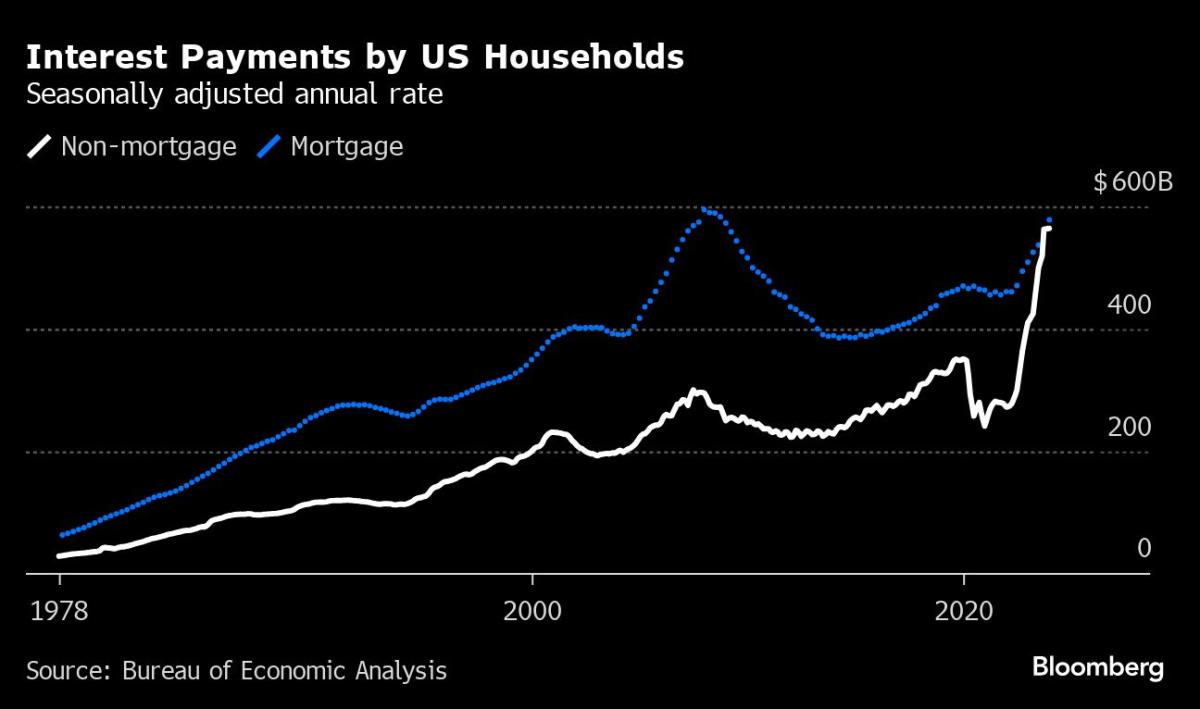

The authors believe the disconnect is explained by the cost of money, which ramped up significantly as the Federal Reserve raised interest rates beginning in March 2022 to combat high inflation. That’s driven up the amount consumers pay to cover outstanding debt.

For example, while the cost of a car is included in the Consumer Price Index, the cost of financing the car is absent. The paper proposed alternative measures of inflation that “explicitly incorporate the cost of money.”

The cost of money also shapes consumer sentiment through the use of credit cards and other forms of financing, according to the paper. Consumers have become more reliant on credit cards for purchases since the pandemic. Many have felt the sting as unpaid balances mount. The cost to finance that debt is a considerable factor in many consumers’ cost of living.

Understating credit

“Measurements of the cost of living that exclude financing costs or do not separate them out from the overall costs of purchases will understate the pressure under which consumers, who rely on credit for many purchases, have found themselves following the recent tightening of monetary policy,” wrote the authors, who also included Marijn A. Bolhuis of the International Monetary Fund and Karl Oskar Schulz at Harvard.

The inclusion of borrowing costs into an alternative measure of CPI inflation significantly narrows the gap between predicted and actual consumer sentiment. More than 70% of the average gap in economic sentiment last year can be explained by the alternative measure, the authors said.

CPI didn’t always exclude financing costs. In a 1983 redesign of the index, however, housing prices and financing costs were dropped for technical reasons in favor of owners’ equivalent rent, a measure of how much an owner would pay to rent the same property.

The latest bout of inflation may force policymakers to reassess the relationship between interest rates, inflation and sentiment. But, more time is needed, according to the researchers.

“Some models may not work anymore, but we cannot yet know if we are in a new economic paradigm,” the authors said.

–With assistance from Ben Holland.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.