The market has gone on an up-and-down roller-coaster ride over the last few years, but for Peloton Interactive (NASDAQ: PTON), the ride has been nothing but downhill. The early-pandemic favorite is off 96% from the all-time high it touched in 2021, meaning if you invested $1,000 in Peloton at its peak, your stake would be worth about $40 today.

Peloton investors who bought in 2021 will likely never break even on the stock, but that doesn’t mean it’s destined to go down forever. And the business — perhaps ever so slightly — is starting to turn things around. Does that mean Peloton stock is set to climb in 2024?

Embracing partnerships and rentals

After the dramatic ouster of founder and CEO John Foley in 2022, Peloton brought in Barry McCarthy to help fix the mess the previous executive team had left. After overexpanding its production capacity and making some poor acquisitions, Peloton was burning more than $1 billion in free cash flow a year and building up inventory far beyond customer demand levels. This put the company at risk of going out of business unless changes were made, and fast.

McCarthy was the chief financial officer of Netflix from 1999 to 2010, and he held the same role at Spotify from 2015 to 2020, giving him a ton of experience managing consumer technology businesses. He took some drastic measures with Peloton in his first few quarters on the job, including conducting four rounds of layoffs, blowing out the buildup in inventory, and starting to sell the company’s products on Amazon. Peloton may not be thriving like it was during 2020, but on the other hand, it’s not at risk of filing for bankruptcy next quarter.

Now, with those defensive moves completed and the business on more stable footing, McCarthy is looking to go back on the offensive a bit. Peloton is inking partnerships for both its hardware and fitness content with companies like Lululemon, and organizations like the University of Michigan, Liverpool Football Club, and the National Basketball Association. It now has three tiers for its fitness app — free, standard, and App+ — with the goal of reaching more fitness enthusiasts who don’t want to buy one of its expensive pieces of exercise equipment.

Another initiative it’s undertaking in a move to increase the affordability of its offerings is renting out its exercise bikes. As of the end of its fiscal 2024 first quarter (Sept. 30), Peloton had 54,000 bike rental subscribers. For reference, it had just under 3 million total connected fitness subscribers. Management thinks the bike rental program can hit 75,000 customers by the end of fiscal 2024.

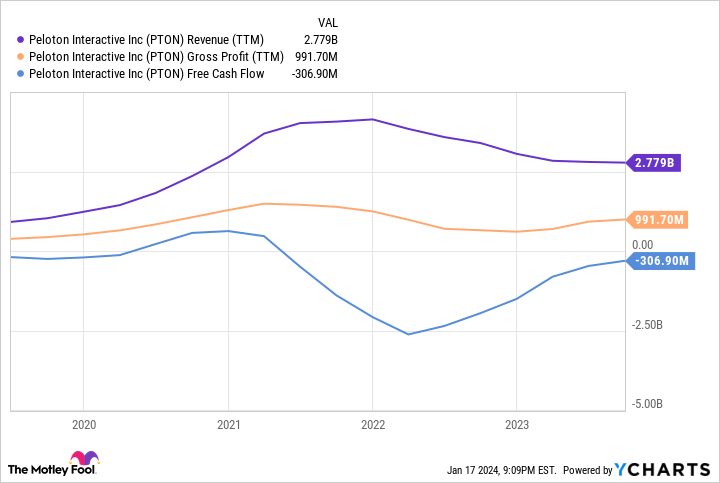

The numbers still look ugly, but they are getting better

Despite all these efforts from the new management team, Peloton’s business fundamentals are not pretty. In its last reported quarter, total revenue declined 3% year over year to $596 million. Its net loss was $159 million, although a lot of that came from non-cash restructuring charges.

But things aren’t all bad for Peloton. Gross profit was actually up 31% year over year due to a major recovery in the unit economics for its equipment sales, which had a negative 37.5% gross margin in the prior-year quarter. This is an example of the negative consequences that can happen when you drastically overbuild your inventory as Peloton did in 2022. It was forced to sell products at significant discounts and with negative gross margins.

Now, inventory levels are a lot healthier, and the company is working toward generating positive free cash flow again. Over the last 12 months, its free cash flow loss was just $307 million compared to $2.5 billion in cash burn at the start of 2022. It still needs to make more progress, but Peloton has improved the business significantly in the last two years.

Expectations are low

Despite these green shoots, Peloton stock continues to flounder. The company currently has a market cap of just $2 billion. Over the last 12 months, its revenue was $2.78 billion, giving the stock a price-to-sales ratio (P/S) of less than 1. That indicates the stock might be cheap.

But what really matters at the end of the day is profitability. Over the last 12 months, Peloton has generated $992 million in gross profits, and that metric should improve over the next few quarters. Today, its bottom-line net income and free cash flow numbers are negative, but with more cost-cutting, Peloton should reach profitability within the next few quarters. If it can again achieve $200 million in annual earnings — like when it peaked in 2021 — it will be trading at a low price-to-earnings ratio of 10.

The stock may be too risky for most. The business is definitely not perfect. But if you like Peloton’s turnaround plan, the stock could eventually prove to be a bargain at these levels.

Should you invest $1,000 in Peloton Interactive right now?

Before you buy stock in Peloton Interactive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Peloton Interactive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 16, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Amazon and Spotify Technology. The Motley Fool has positions in and recommends Amazon, Lululemon Athletica, Netflix, Peloton Interactive, and Spotify Technology. The Motley Fool has a disclosure policy.

Down 96% From Its Peak, Will Peloton Stock Finally Rebound This Year? was originally published by The Motley Fool