(Bloomberg) — Asian shares traded mixed at the start after Wall Street slumped on Friday amid signs US inflation is stickier than expected. Chinese stocks are poised for a strong open after a week-long holiday.

Most Read from Bloomberg

Japan’s Topix Index traded slightly higher, while the Nikkei 225 fluctuated with shares in gaming company Nintendo Co. falling as much as 8.5%. Australian stocks were slightly higher. Contracts for Hong Kong equities climbed, while those for the US were little changed after the S&P 500 dropped 0.5% on Friday.

There was no cash trading of Treasuries on holiday in the US. They fell on Friday, with two-year yields up seven basis points to 4.65% after the producer price index rose on a sizable jump in costs of services.

The yen steadied around 150 per dollar with the greenback weakening against all of its Group-of-10 peers.

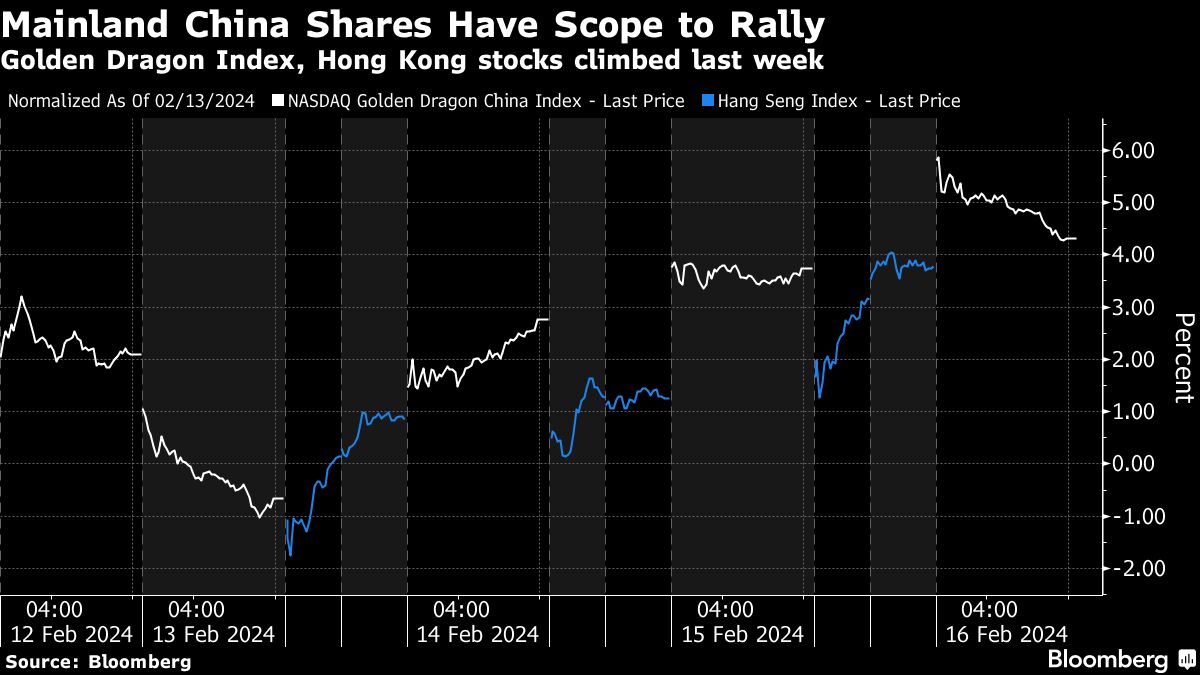

Chinese shares will be in focus in Asia as they resume trading following the week-long Lunar New Year break after the central bank held the interest rate on one-year policy loans at 2.5% while injecting a small amount of cash into the financial system.

Prior to the PBOC’s announcement, buoyant travel and tourism data suggested consumption has revved up even as the broader economy struggles with deflation and a property crisis. The sentiment has helped the benchmark gauge of stocks in Hong Kong rally 3.8% since it reopened on Wednesday while the Nasdaq Golden Dragon Index jumped 4.3% for the week, underscoring room for onshore shares to play catch-up.

“The early read from Chinese New Year data, from holiday hotel sales to Macau visit numbers, points to bright spots in services-related industries,” said Linda Lam, head of equity advisory for North Asia at Union Bancaire Privee. “A-shares should open on a stronger note, continuing the share price recovery on the back of state support,” she said, referring to Chinese stocks traded on the mainland.

Oil fell, but remained near the highest level this year as persistent tensions in the Middle East added a risk premium to the market.

Elsewhere, US and global stocks are yet to respond to the sell-off in Treasuries this month as a string of better-than-expected economic data drove traders to roll back their once-aggressive rate-cut bets so much that their expectations are now approaching the Fed’s own 75 basis-point forecast this year. Swaps are pricing about 90 basis points of rate cuts in 2024 — from more than 150 basis points at the start of February.

Goldman Sachs expects the rally in the US to continue, with the S&P 500 reaching 5,200 by year-end as the resilient US economy drives company profit growth, strategists led by David Kostin wrote in a note to clients. The new target implies a 3.9% jump from Friday’s close.

UBS Group AG’s wealth management unit also has a positive view on equities once the Federal Reserve starts cutting rates, particularly in small-cap stocks as consumer spending should stay healthy given the strength of the labor market.

“Fed rate cuts are likely still not far off, despite mixed comments from top officials,” said Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management. “While we do not expect the path toward lower inflation and lower rates to be smooth, we maintain the view that a soft landing for the US economy favors quality bonds and equities.”

This week, traders will be keeping an eye on European inflation data as well as earnings from Nvidia Corp. and mining giants BHP Group and Rio Tinto Plc to help gauge the health of the global economy. Meantime, conflict in the Middle East is set to drag on as negotiations aimed at securing an Israel-Hamas cease-fire and the release of hostages haven’t progressed as hoped, Qatar’s foreign minister said.

Some of the key events this week:

-

Reserve Bank of Australia Feb. meeting minutes, Tuesday

-

China loan prime rates, Tuesday

-

BHP Group Ltd earnings, Tuesday

-

European Central Bank publishes euro-area indicator of negotiated wage rates, Tuesday

-

Rio Tinto Plc earnings, Wednesday

-

Eurozone consumer confidence, Wednesday

-

Nvidia Corp earnings, Wednesday

-

Federal Reserve Jan. meeting minutes, Wednesday

-

Atlanta Fed President Raphael Bostic speaks, Wednesday

-

Eurozone CPI, PMI, Thursday

-

European Central Bank issues account of Jan. 25 meeting, Thursday

-

Fed Governor Lisa Cook, Minneapolis Fed President Neel Kashkar speak, Thursday

-

China property prices, Friday

-

European Central Bank executive board member Isabel Schnabel speaks, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures were little changed as of 8:18 a.m. Tokyo time. The S&P 500 fell 0.5% on Friday

-

Nasdaq 100 futures rose 0.2%. The Nasdaq 100 fell 0.9%

-

Japan’s Topix index rose 0.2%

-

Australia’s S&P/ASX Index 200 rose 0.2%

-

Hong Kong’s Hang Seng futures rose 0.1%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.0785

-

The Japanese yen was little changed at 150.11 per dollar

-

The offshore yuan was little changed at 7.2100 per dollar

-

The Australian dollar rose 0.1% to $0.6539

Cryptocurrencies

-

Bitcoin rose 0.5% to $52,117.42

-

Ether rose 1.1% to $2,877.91

Bonds

Commodities

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.