The UK stock exchange has fallen further behind its European peers after a resurgence of new listings on the Continent put London in the shade.

A bounceback of initial public offerings (IPOs) across Europe saw almost €5bn (£4.3bn) worth of new listings in the first quarter, but London contributed just over €300m of the total, according to figures from PwC.

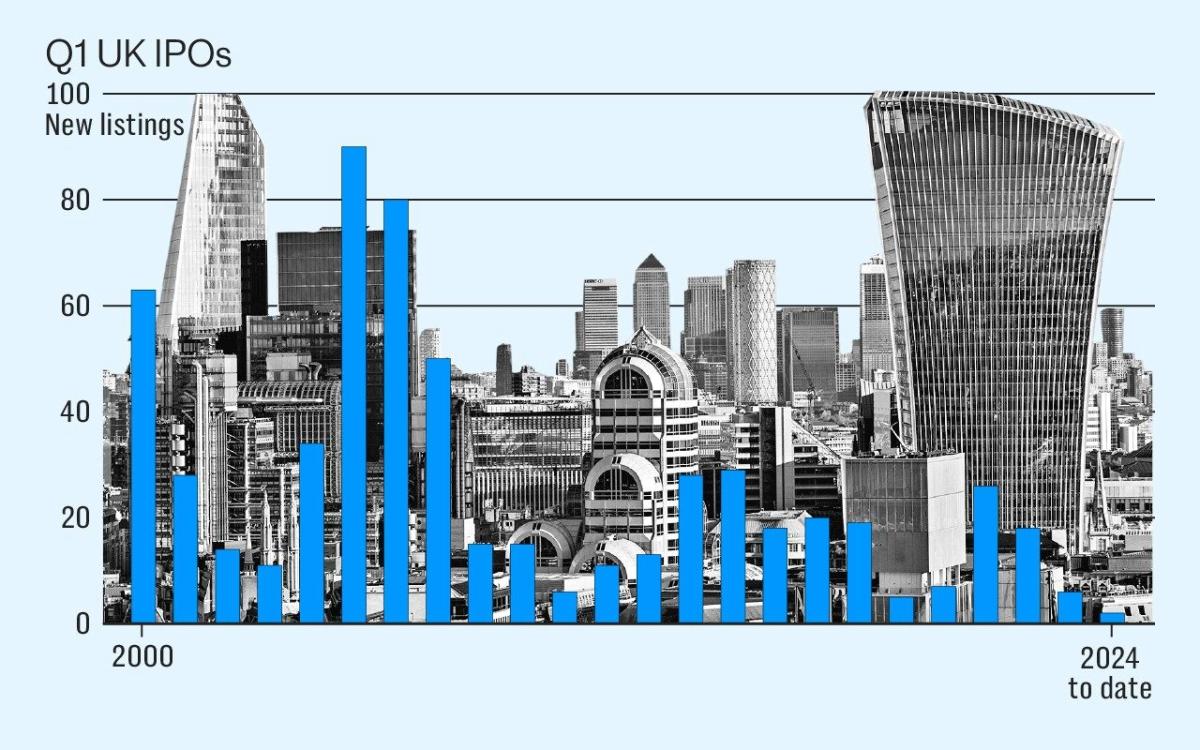

Europe’s IPO blossoming will do little to dispel concern that London’s once-dominant stock market is in trouble as its float famine continues.

The German, Swiss and Greek stock exchanges all outpaced London, as an IPO freeze triggered by gloomy economic data and high inflation started to thaw.

The blockbuster flotation of skincare brand Galderma on the SIX Swiss Exchange led the charge, raising €2bn.

Deutsche Borse, long considered the main European rival to the London exchange, also attracted two major new debuts.

Renk, a German manufacturer of tank engines, raised €450m while German perfume retailer Douglas raised €890m after its owner CVC Capital cashed out. Athens also saw the listing of the city’s Eleftherios Venizelos International Airport.

The blockbuster haul left London further in the shade, with the City’s listing of Kazakh airline Air Astana the best on offer at €324m.

PwC UK Capital Markets partner Vhernie Manickavasagar said the continental boom had been led by domestic companies and London remained the choice for international organisations.

“London is still the market people look to outside of their domestic market,” she said.

“The IPOs you’ve seen in Europe are domestic IPOs on the domestic market. Air Astana shows that London is still the market that Europeans go for when they want an international listing outside of their domestic market.”

She added that the revival on the Continent could prompt UK boardrooms to consider a float.

“People are now seeing that the markets are bouncing back but companies are only now starting to think through their processes, which means that they’re not going to come through until the end of the year.

“We are also going to have some significant changes (in London) which people are watching, and you’ve not had that in the European markets to the same extent.”

Better economic data has encouraged more companies to tap the stock market, making the lack of floats in London even more puzzling.

High stock market volatility puts off floating companies over fears the IPO will go badly but this has recently fallen.

Lower inflation and more predictable interest rate expectations have dampened down volatility, opening the door for more new listings.

One City broker blamed the drought on the lack of demand from UK fund managers and said the current level of IPOs in the London market was “woeful.”

The main London market welcomed just two new listings last quarter, according to Dealogic, which is the worst quarter in volume terms since the data company started collecting figures in 1995.

“There is no shortage of companies that could come and IPO on the exchange,” the broker said.

“You only need one or two big listings to start to get the dominos falling. The issue is with the demand. The good companies aren’t coming because [the fund managers] won’t back them.

“They won’t come to market until the demand side is fixed.”

Chancellor Jeremy Hunt has put forward a raft of reforms to try and fix the problem.

The Edinburgh Reforms, a package of measures to remove onerous listing restrictions on companies, have been coupled with supply side changes such as the British Isa to try and dispel the gloom hanging over UK stocks.

Allocations to UK equities have been on a steady decline for several years.

Estimates from Numis suggest that March saw another net outflow from UK equity funds of around £2.6bn, taking the total for the year to £4.6bn.

That means 2024 is on course for another year of net outflows, the ninth consecutive year when more money has left UK equity funds than has been added since 2015.

The less cash that flows into UK equities, the lower the valuations, which ultimately makes the UK market a less attractive place to list a company.

The UK valuation gap has been made even starker by the runaway success of the Nasdaq, where the “Magnificent Seven” – Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia and Tesla – has made London seem even more unattractive.

However City fund manager Gervais Williams, who heads equities at Premier Miton, said a string of IPO duds had left many sceptical about the quality of new listings.

“We’ve had a series of pretty rubbish IPOs,” he said.

“Whatever reason it isn’t working as well as it could do, especially given that supposedly we’re high grading the IPOs, given there aren’t that many of them.”

Significant IPOs in the London market, such as CAB Payments, have burned many fund managers. The stock, seen as a possible catalyst for a listing revival last year, has fallen 60pc since floating.

Looking ahead, the prospects of London attracting significant IPOs in future looks uncertain.

The possible listing of Unilever’s ice cream division could be a candidate for London, but chief executive Hein Schumacher recently said that Amsterdam was in the lead for any listing.

CVC, the private equity firm behind the Six Nations rugby tournament, is also set to list in Amsterdam rather than London in another major blow for the capital.

Flutter Entertainment is due to change its primary listing to New York from London following similar moves from companies including TUI, which shifted its main listing to Frankfurt.

Alongside this, a drumbeat of other candidates could follow.

Last week analysts at Deutsche Bank said FTSE 100 commodity trading giant Glencore could be the next company to up sticks from London and transfer to New York.

The group had already planned to spin out its coal unit and list this in New York rather than London, prompting speculation that the whole business could up sticks from London.

However, Mr Williams said there was still fund manager demand for good companies, citing the possible float of Raspberry Pi as a possible catalyst for more issues.

“I don’t think the market is entirely closed at all,” he said. “Clearly you’ve got to have some great issues and I think if you get two or three good issues then the market will open up again.”