If you’re an individual investor who wants to invest like a billionaire fund manager, I’ve got good news. Following billionaires is relatively easy because the U.S. Securities and Exchange Commission makes anyone who manages over $100 million in assets report their trading activity every quarter.

In the last three months of 2023, several prominent billionaires bought shares of 23andMe (NASDAQ: ME) even though the stock has been plunged from its previous peak.

Before plowing any of your hard-earned money into the genetic testing stock, it’s important to remember that even the most successful investors can be wrong from time to time.

Here’s a closer look at 23andMe to see if buying the stock on the dip makes sense for most investors.

23andMe is attracting billionaire investors

23andMe’s first three years as a publicly traded, consumer-based DNA testing business have been difficult for its investors. The stock is down about 97% from the all-time high it reached three years ago, but billionaire hedge fund managers are expecting a rebound.

During the last three months of 2023, billionaire fund managers scooped up millions of shares.

|

Billionaire Fund Manager(s) |

Fund |

Shares Acquired in Q4 2023 |

Shares Owned on Dec. 31, 2023 |

|---|---|---|---|

|

David Siegel and John Overdeck |

Two Sigma Investments |

699,669 |

871,795 |

|

Jim Simons |

Renaissance Technologies |

660,900 |

3,478,061 |

|

Ken Griffin |

Citadel Advisors |

467,246 |

1,717,743 |

|

Jeff Yass |

Susquehanna International |

374,705 |

596,862 |

Table by author. Data source: 13f.info

Why billionaires are buying 23andMe

You’re probably familiar with 23andMe’s consumer-focused business that provides ancestry and medical information for a combination of upfront and recurring fees. With genetic data from millions of customers, it can offer drug developers unprecedented insight that could help them discover new drug candidates.

In October, GSK (NYSE: GSK), a giant pharmaceutical company, extended a five-year collaboration with 23andMe to conduct drug target discovery. GSK paid 23andMe $20 million upfront for a one-year, nonexclusive data license. Plus, 23andMe could receive milestone payments when new drug candidates succeed in clinical trials. 23andMe could also earn royalties if a new drug candidate it helps GSK discover goes on to earn approval from government regulators.

In addition to a data licensing operation, 23andMe is developing new drug candidates of its own. Earlier this month, the company began a clinical trial with an experimental cancer therapy tentatively named 23ME-1473. If the results, which are expected in 2026, read out positively, the stock could soar.

What the bears say

Investors should temper their enthusiasm for 23andMe’s data licensing operation. Its exclusive contract with GSK ended last July, but GSK is still the only company paying for access to 23andMe’s data trove.

23andMe has more than 14 million customers worldwide. This is a large sample, but it most likely leans toward wealthier, more educated consumers. This limitation could explain why 23andMe still hasn’t signed up any new big pharma clients.

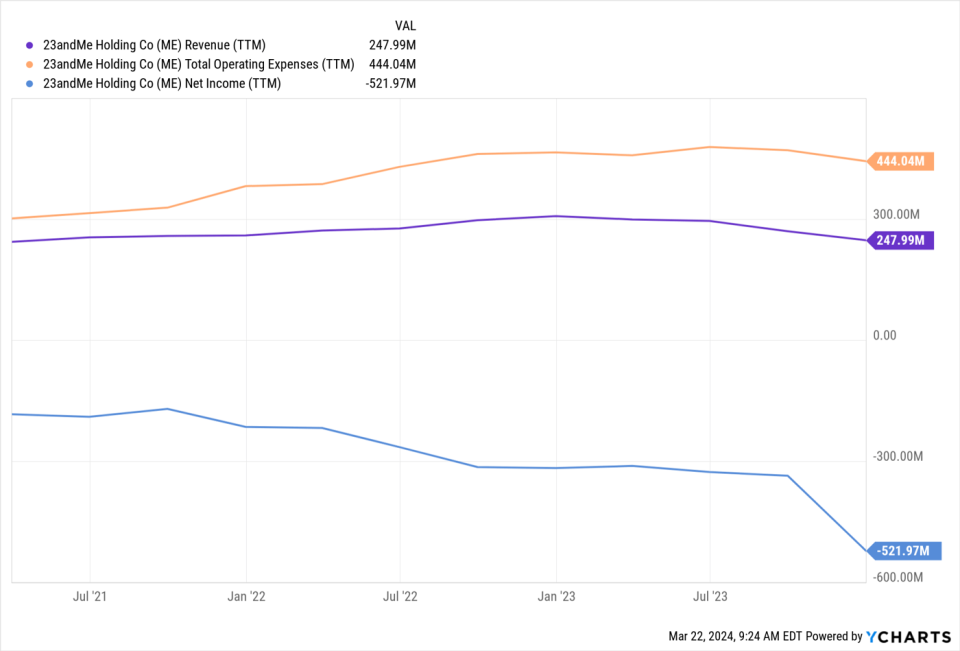

Total revenue during the last three months of 2023 fell about 33% year over year due to lower fees for a nonexclusive license from GSK. As a result, 23andMe’s losses accelerated to nearly $522 million in the calendar year 2023.

In addition to a data licensing segment that isn’t going anywhere fast, 23andMe’s attempt to make genetic testing a subscription service isn’t working out, either. Management expects total revenue to fall from $299 million in fiscal 2023 to a range between $215 million and $220 million in fiscal 2024, which ends on March 31.

Falling revenue from both consumer services and research services means investors are relying on 23andMe’s drug development programs. Unfortunately, the vast majority of drugs that begin clinical trials never become commercial products.

A buy now?

At recent prices, 23andMe sports a minuscule $208 million market cap. With expectations this low, the stock could rocket higher if upcoming clinical trial results show signs of success.

Before you plow any of your own hard-earned money into 23andMe, though, it’s important to realize it’s extremely risky. The company finished December with just $242 million cash after that $522 million loss in 2023.

If upcoming clinical trial readouts aren’t rousing success, 23andMe stock could fall much further. Billionaires have purchased millions of shares, but the positions make up less than 0.1% of their total portfolios. If you’re willing to take a chance on this risky stock, it’s best to follow the professionals and make it a similarly small portion of your portfolio.

Should you invest $1,000 in 23andMe right now?

Before you buy stock in 23andMe, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and 23andMe wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 21, 2024

Cory Renauer has no position in any of the stocks mentioned. The Motley Fool recommends GSK. The Motley Fool has a disclosure policy.

Billionaires Are Snapping Up Beaten-Down 23andMe Stock. Should You Follow Their Lead? was originally published by The Motley Fool