(Bloomberg) — As Joe Biden this week hailed America’s booming economy as the strongest in the world during a reelection campaign tour of battleground-state Pennsylvania, global finance chiefs convening in Washington had a different message: cool it.

Most Read from Bloomberg

The push-back from central bank governors and finance ministers gathering for the International Monetary Fund-World Bank spring meetings highlight how the sting from a surging US economy — manifested through high interest rates and a strong dollar — is ricocheting around the world by forcing other currencies lower and complicating plans to bring down borrowing costs.

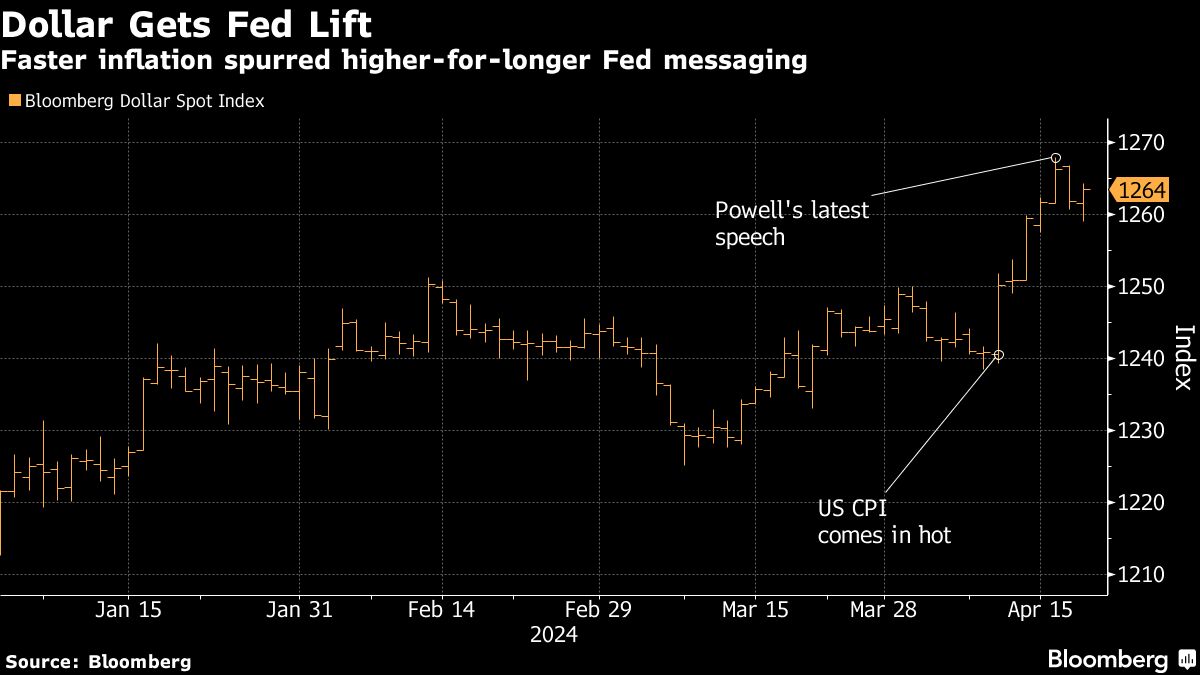

Just as officials began arriving in the US capital, Chair Jerome Powell on Tuesday issued a warning that the long-anticipated Federal Reserve interest-rate cuts will be delayed yet further due to disappointingly high US inflation readings.

That shift set the tone for the confab, triggering a global government-bond selloff that sent yields to the highest levels in months and put pressure on a raft of currencies including the yen, which hit the lowest since 1990 against the dollar. Japanese and South Korean authorities scrambled to talk up their currencies, Indonesia told state firms to hold off on big dollar purchases and Malaysia issued an intervention warning.

“Of course it is concerning,” as IMF Managing Director Kristalina Georgieva summed it up Thursday with reference to the dollar’s strengthening. “All eyes are on the US,” with many delegations in Washington questioning how long the Fed will be stuck before it lowers rates. “That’s what I hear from countries,” she said in an interview with Bloomberg Television’s Surveillance.

New forecasts released by the IMF show just how much of an outlier the US is. The fund boosted its 2024 growth outlook for the US to 2.7%, up from 2.1% in January — more than double the pace of each of its Group of Seven counterparts.

While that’s helping support global growth, it also means the US is “slightly overheated,” Georgieva said — thanks in part to Washington’s fiscal stance, with the budget gap pushing toward 7% of GDP.

Her colleague, IMF chief economist Pierre-Olivier Gourinchas, earlier in the week said the US budget stance creates “longer-term fiscal and financial stability risks for the global economy.”

German Finance Minister Christian Lindner was more blunt, calling out Biden administration industrial policies including the so-called Inflation Reduction Act, which offers subsidies for clean energy and the electric vehicle sector.

Lindner warned his own nation against adopting such a policy, saying Wednesday, “I don’t want to be impolite, but if we look at the economic development in the US, the inflation rate is higher again and this forces the Fed to react.”

Treasury Secretary Janet Yellen the same day heard her counterparts from South Korea and Japan complaining about the weakness of their exchange rates — offering a nod to their concerns in a joint statement with Asia’s top two allies.

Policy Independence

A common thread among many finance chiefs in Washington this week has been insisting on policy independence.

While Brazilian Finance Minister Fernando Haddad said the Fed’s delay will trigger a repricing across global markets, his central bank counterpart Roberto Campos Neto highlighted that his nation’s external accounts are very strong — helping differentiate its position relative to some others.

South African Reserve Bank Governor Lesetja Kganyago said, “We watch the Fed. We don’t follow the Fed.” Even so, he said on Bloomberg TV that “the actions of the Fed have got huge implications for global financial markets.”

There was also at least one expression of envy.

“I wish I had that unemployment rate,” Carlos Cuerpo, Spain’s economy minister, said in an interview with Bloomberg, noting the two-year US run with sub-4% joblessness.

Reckoning Coming

Still, a reckoning may be inevitable, in the view of European Commission Vice President Valdis Dombrovskis. “Obviously all this will warrant discussion in the US on the direction of fiscal policy and whether some more prudence is needed,” he told reporters.

US debt held by the public is expected to reach $48.3 trillion, or 116% of GDP by 2034, up from 97% at the end of 2023, according to the Congressional Budget Office.

It isn’t only US interest rates that are drawing global attention.

On his swing through Pittsburgh, Biden vowed to keep United States Steel Corp. American-owned and called for higher tariffs on Chinese steel and aluminum as he sought to woo union workers ahead of November’s election.

“America is rising,” Biden said. “We are the strongest economy in the world.”

Yet the renewed use of industrial policy, export controls and other protectionist measures is also stoking a backlash from trading partners.

“The subsidy race is a race to the bottom and we shouldn’t go in that direction,” European Central Bank President Christine Lagarde said.

Trade protection is likely only to intensify should former president Donald Trump win reelection. Trump’s plan to raise tariffs on US imports would spark a “free for all” in the global trading system that renders existing rules useless and hurts every economy, World Trade Organization Director-General Ngozi Okonjo-Iweala said.

“The big elephant in the room here is the US election,” said Marcelo Carvalho, London-based economist at BNP Paribas.

–With assistance from Alexander Weber, Maria Eloisa Capurro, Philip Aldrick, Viktoria Dendrinou, Christopher Condon, James Mayger, Yujing Liu, Yoshiaki Nohara, George Lei and Kamil Kowalcze.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.