The rivalry between Advanced Micro Devices (NASDAQ: AMD) and Intel (NASDAQ: INTC) has persisted for decades. For most of that history, Intel was the world’s largest semiconductor company, dominating its rival.

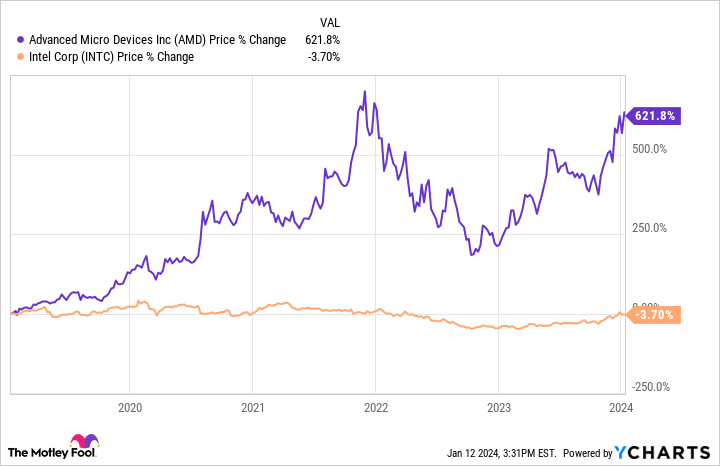

However, the dynamics of the rivalry shifted as Intel fell into decline and AMD reemerged as a leading CPU and GPU company. Over this time, AMD has gained a technical lead, taking market share from Intel in the client and data center spaces. Given those advances, it will surprise few that AMD stock has dramatically outperformed Intel over the last five years.

Still, artificial intelligence (AI) will likely increase demand for chips exponentially, a factor that should benefit all companies.

Moreover, under CEO Pat Gelsinger, Intel has more actively competed with AMD, releasing more advanced chips and remaking itself as a manufacturer. The question for investors is whether that will again make Intel a better investment.

The continuing battle

Interestingly, the recent CES 2024 didn’t reveal much about these companies’ never-ending competitive battle. AMD focused heavily on GPUs and APUs, while Intel revealed new lines of CPUs for desktops, laptops, and automobiles.

Nonetheless, both companies remain in a competitive battle in the CPU and GPU spaces. Intel made strides late last year to catch up and surpass AMD’s CPUs, and today, choosing the “best” CPU may come down to budget constraints and needs rather than a clear choice of one company over the other.

Also, Intel revealed to PCWorld its Battlemage GPU is “in the labs” and will come out later in 2024. Still, Intel’s move into GPUs is recent, while AMD has focused on that technology since CEO Lisa Su worked to revamp AMD in the mid-2010s. Thus, it is unclear how Intel will fare in this semiconductor niche.

Furthermore, AMD and Intel drastically differ in one area: production capabilities. AMD is a fabless design company. Thus, it designs chips and outsources production to Taiwan Semiconductor and others.

In contrast, Intel still produces most of the chips it designs and has repurposed production capabilities to serve as a manufacturer. It serves companies like Amazon and Cisco, and as the U.S.’s largest chip manufacturer, the ability to produce what it designs quickly and closely could serve as an advantage.

How financials compare

The semiconductor industry had recently experienced a down cycle; hence, neither company has revealed compelling financials. However, of the two names, AMD has been the growth leader, and even in a downturn, its revenue declines were not as dramatic as Intel’s.

In the first nine months of 2023, AMD’s net revenue came in at $16.5 billion, an 8% drop from the same period in 2022. Still, revenue grew 4% in Q3, so the recovery may already be underway.

Free cash flow also fell off a cliff from 2022 levels, when it generated almost $2.7 billion in free cash flow in the first nine months of that year. Nonetheless, cash flows remained positive, with AMD still generating $879 million in free cash flow in the first three quarters of 2023.

Intel suffered to a much greater degree, with its $39 billion in revenue for the first three quarters of 2023 dropping 21% yearly. Additionally, revenue fell by 8% in Q3, showing an industry recovery has not yet benefited the company.

Also, with Intel investing tens of billions in new fabs, its free cash flow came in at a negative $12 billion for the first nine months of the year. This improved from the $24 billion negative free cash flow in the year-ago period. Also, free cash flow was $943 million in Q3, indicating the worst could be over.

Furthermore, Intel reported net losses for the first three quarters of 2023, making a comparison by P/E ratios invalid. When looking at price-to-sales (P/S) ratios, AMD trades at 11 times sales versus just 4 for Intel. Still, with AMD in a much stronger financial position, it is arguably worth that premium valuation.

AMD or Intel?

Between these two companies, more conservative investors should probably choose AMD. Under Lisa Su, the company has proven adept at catching up or surpassing the technology of its competitors. Given the expected increase in chip demand, one can assume that AMD will be a primary beneficiary.

However, if making a more speculative investment, prospective buyers should probably consider Intel. Intel remains the largest fab company in the U.S., and many of the top chip design companies have become its clients.

Moreover, Intel’s efforts to improve its chips show it will no longer willingly surrender the technical lead to its competitors. Thus, its size advantage could bring higher returns, given the semiconductor stock’s low valuation.

Should you invest $1,000 in Advanced Micro Devices right now?

Before you buy stock in Advanced Micro Devices, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Advanced Micro Devices wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 8, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Will Healy has positions in Advanced Micro Devices and Intel. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Cisco Systems, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Better Semiconductor Stock: AMD vs. Intel was originally published by The Motley Fool