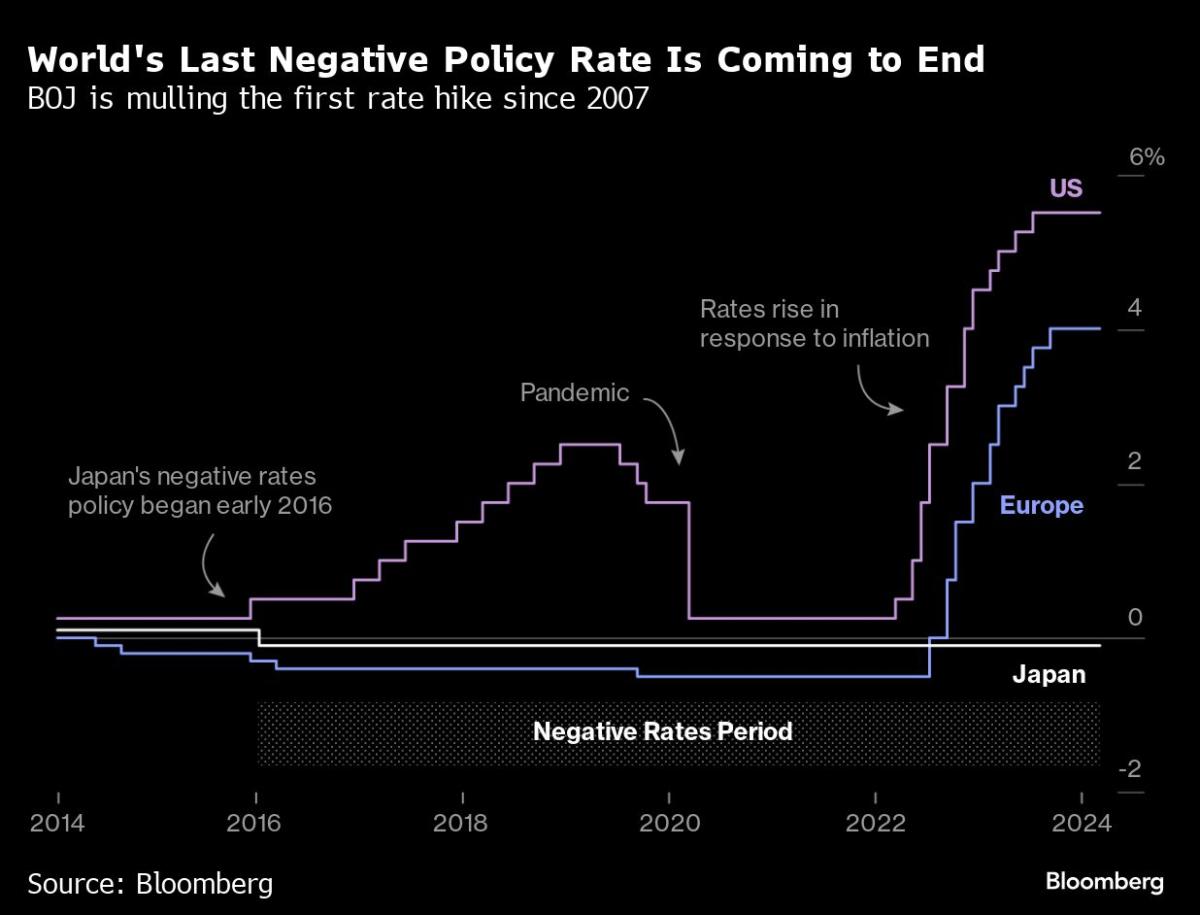

(Bloomberg) — Asian shares marginally fell before a Bank of Japan policy decision where authorities are likely to bring an end to the world’s last negative rates regime.

Most Read from Bloomberg

Japan’s Nikkei 225 index of blue chip stocks slipped while the broader Topix index swung between gains and losses. South Korean equities declined over 1% as funds sold their tech stakes following Nvidia Corp.’s decline in post-market trading after unveiling its new AI chip.

Contracts for Hong Kong and US shares pointed to losses. That followed Monday’s rebound on Wall Street ahead of a raft of other central-bank decisions this week from the US to the UK.

In Japan, some 90% of central bank watchers see the chance of authorities ending the negative rate on Tuesday at the meeting’s conclusion, with the nation’s first interest rate hike in 17 years. The yen steadied amid a news report the BOJ is also poised to end its policy of guiding government bond yields — known as yield curve control.

Bank officials are also considering ending their buying of exchange-traded funds and real estate investment funds, according to people familiar with the matter. Traders betting on the BOJ outcome boosted their positions in yen futures to the highest since 2007.

“First off, they’re going to engineer a dovish hike,” Yue Bamba, head of Japan active investments at BlackRock Inc., said on the BOJ on Bloomberg Television. “We expect that they’re going to be very careful in their messaging to not disrupt markets and not alarm markets, and emphasize that this is going to be a highly gradual process, that they’re not rushing into anything.”

Australia’s central bank will also announce its rates policy on Tuesday and is widely expected to hold them at a 12-year high, with the economy showing signs of slowing further while unemployment trends higher.

Treasuries were little changed in early Asian trading. Yields on the two-year note hovered near 2024 highs Monday as expectations for Federal Reserve rate cuts continued to erode. The dollar was little changed.

Investors in Asia will be watching China, where the top securities regulator said the defaulted developer at the heart of the nation’s real estate crisis falsely inflated revenue by more than $78 billion in the two years leading up to its failure. China Evergrande Group and its massive debt have become symbolic of the nation’s stuttering economy, particularly in its property and construction sectors.

Jam-Packed Week

Back in the US, Wall Street is gearing up for more insights on the Fed’s resolve to ease as central banks set policy for almost half the global economy. The week features the world’s biggest agglomeration of decisions for 2024 to date, including judgments on the cost of borrowing for six of the 10 most-traded currencies.

“It’s a jam-packed week of central bank meetings,” said Win Thin and Elias Haddad at Brown Brothers Harriman. “There are sure to be some surprises and so today’s calm is likely to give way to greater volatility ahead.”

The S&P 500 halted a three-day slide, the Nasdaq 100 rose 1% and a gauge of the “Magnificent Seven” tech megacaps climbed twice as much. Alphabet Inc. jumped as Bloomberg News reported Apple Inc. is in talks to build Google’s Gemini artificial-intelligence engine into the iPhone. In late hours, Nvidia Corp.’s chief Jensen Huang revealed new chips aimed at extending his company’s dominance of AI computing.

Goldman Sachs Group Inc. economists led by Jan Hatzius changed their forecast to call for three quarter-point Fed cuts this year — instead of four. The change, which brings the forecast in line with the median forecast policymakers made in December, is “mainly because of the slightly higher inflation path,” they said.

Investors will be keenly focused on the US central bank’s projections — the dot plot — to gauge how many rate cuts policymakers are expecting to deliver this year.

Wall Street will listen carefully to any signs from Powell on the phase out of quantitative tightening, known as QT. While a handful expect the Fed to announce or even begin slowing the unwind of its balance sheet as early as May, others don’t see a tapering starting until the second half of the year.

In other markets, oil held a gain, with Ukrainian drone attacks on Russian refineries and OPEC+ supply cuts in focus. Gold traded steady after rising in its previous session.

Key events this week:

-

Reserve Bank of Australia rate decision, Tuesday

-

Bank of Japan rate decision, Tuesday

-

Germany ZEW survey expectations, Tuesday

-

European Central Bank Vice President Luis de Guindos speaks, Tuesday

-

US housing starts, Tuesday

-

Eurozone consumer confidence, Wednesday

-

Fed rate decision; Chair Jerome Powell holds news conference, Wednesday

-

Reddit’s IPO, Wednesday

-

ECB’s Christine Lagarde speaks, Wednesday

-

Eurozone S&P Global Services PMI, S&P Global Manufacturing PMI, Thursday

-

Bank of England rate decision, Thursday

-

US Conference Board leading index, existing home sales, initial jobless claims, Thursday

-

Nike, FedEx earnings, Thursday

-

Japan CPI, Friday

-

Germany IFO business climate, Friday

-

Atlanta Fed President Raphael Bostic speaks, Friday

-

ECB’s Robert Holzmann and Philip Lane speak, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures fell 0.2% as of 9:57 a.m. Tokyo time

-

Hang Seng futures fell 0.5%

-

Nikkei 225 futures (OSE) fell 0.7%

-

Japan’s Topix was little changed

-

Australia’s S&P/ASX 200 was little changed

-

Euro Stoxx 50 futures fell 0.2%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.0870

-

The Japanese yen was little changed at 149.20 per dollar

-

The offshore yuan was little changed at 7.2058 per dollar

-

The Australian dollar fell 0.1% to $0.6551

Cryptocurrencies

-

Bitcoin fell 0.4% to $67,072.23

-

Ether fell 1.4% to $3,457.75

Bonds

-

The yield on 10-year Treasuries was unchanged at 4.32%

-

Japan’s 10-year yield advanced one basis point to 0.765%

-

Australia’s 10-year yield advanced two basis points to 4.13%

Commodities

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.