Investors with a high risk appetite can consider gaining exposure to companies in emerging economies. In addition to portfolio diversification, you may gain access to some of the world’s fastest-growing economies. One such region is Latin America, where Nu Holdings (NYSE:NU) has gained traction. Based in Brazil, NU stock has trailed the broader markets since its IPO in December 2021. Down 23% from its all-time high, NU stock is attractively priced and has significant upside potential in the upcoming decade.

I remain bullish on NU stock due to its widening portfolio of products, which should lead to a rapidly expanding customer base and an uptick in sales and earnings.

An Overview of Nu Holdings

Founded in 2013, Nu has successfully disrupted the financial services segment. It is one of the largest digital financial services platforms globally, serving roughly 90 million customers across Brazil, Colombia, and Mexico.

Over the years, Nu has leveraged its technology expertise to create financial solutions for individuals and businesses. Nu offers credit and debit cards to customers. It also offers mobile payment solutions and savings accounts. Further, you can buy cryptocurrencies through the Nu application, making it easier to gain access to another asset class.

The NuInvest product enables customers to invest in equities, fixed-income, options, exchange-traded funds, and multi-market funds. Moreover, you can apply for personal unsecured loans or BNPL (buy now pay later) solutions as well, making Nu a one-stop shop for the new-age banker.

Nu raised $2.3 billion in its IPO and has since added 65 products and features to its application.

How Did Nu Perform in Q3 2023?

In Q3 2023, Nu added 5.4 million customers, and this figure comes in at 18.7 million in the last 12 months, allowing the company to end the quarter with 89.1 million customers. Nu is now the fifth-largest financial institution in Latin America by customer count. Its customer base surpassed 84 million in Brazil, accounting for 51% of the country’s adult population.

Nu’s monthly average revenue per active customer grew by 18% year-over-year to $10. Additionally, its growing customer base and higher spending allowed it to report revenue of $2.1 billion in Q3 2023, an increase of 53% year-over-year.

In its annual report for 2022, Nu emphasized that its spending on customer acquisition is quite low as it has gained a majority of customers organically and through word of mouth. Further, in Q3, its average cost to serve per active customer remained unchanged at $0.9, resulting in solid bottom-line growth.

Nu reported an adjusted net income of $355.6 million in Q3, up from just $63 million in the year-ago period. An asset-light model, coupled with low operating expenses and robust gross margins, has allowed Nu to improve earnings at an accelerated pace in 2023.

A Focus on Earnings

The banking industry is quite cyclical, and several financial institutions wrestle with lower earnings and cash flows during periods of economic downturn. Nu has managed to increase its customer count significantly despite a challenging macro environment, resulting in stellar revenue growth.

It also ended Q3 with an efficiency ratio of 35%, which is remarkable for a growth stock, as Nu’s operating leverage improved for the seventh consecutive quarter. Generally, an efficiency ratio of less than 50% is considered to be good.

In the last two years, Nu has almost doubled its customer count while its sales have grown by 344%. Comparatively, the company reported a loss of $34.3 million in Q3 2021 and has since focused on margin growth amid a difficult macro environment.

What Next for NU Stock?

After gaining massive traction in Brazil, Nu is positioned to increase its presence and market share in several other Latin American markets. It can also enter other developed international markets, including the U.S., Canada, Australia, and Europe.

According to Wall Street, Nu’s growth story is far from over, as the company is forecast to end 2024 with sales of $10.7 billion, up from just $4.8 billion in 2022. Comparatively, its adjusted earnings are forecast to improve to $0.35 per share in 2024, up from -$0.08 per share in 2022.

So, NU stock trades at 4x forward sales and 26.1x forward earnings, which is not very expensive. While the sector price-to-earnings multiple is far lower at 10.3x, it primarily includes valuations for legacy banks, including Citi (NYSE:C), Wells Fargo (NYSE:WFC), and JPMorgan (NYSE:JPM). Nu’s stellar growth metrics allow it to command a premium valuation.

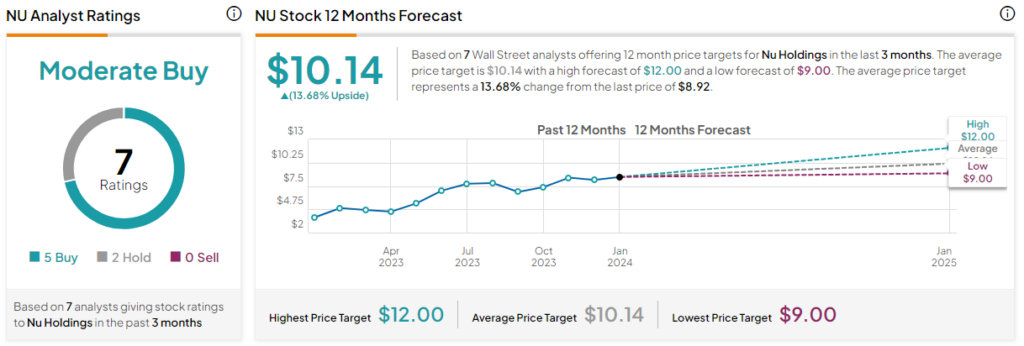

Is NU Stock a Buy, According to Analysts?

Out of the eight analysts covering NU stock, six recommend a Buy, two recommend a Hold, and none recommend a Sell, giving it a Strong Buy consensus rating. The average NU stock price target is $10.14, 13.7% above the current price.

The Takeaway

Nu has a strong record of improving operating leverage as the business continues to scale, resulting in sustained gross profit growth and margin expansion. The steady expansion of its loan portfolio and superior asset quality should allow Nu to grow at an industry-leading pace in 2024 and beyond, while its attractive valuation boosts the stock’s investment case.