Justin Sullivan

Introduction

Writing about bank-issued preferred stock generates high read counts, indicating their interest to the Seeking Alpha community. Having reviewed preferred stocks from other large US banks, this time I chose the two lowest coupon issues available from Wells Fargo & Company (NYSE:WFC), currently the third-largest bank in the US as measured by Total Assets.

- Wells Fargo & Company 4.37 DP A PFD CC (NYSE:WFC.PR.C)

- Wells Fargo & Company DEP CL A PFD DD (NYSE:WFC.PR.D)

After comparing the yields of all five similar preferred stocks, the Pfd DD issued offers the best combination of yield and call protection. That said, another major bank I see having like risk levels, has preferred stocks with much higher yields. That bank is listed later.

Understanding Wells Fargo & Company

Seeking Alpha provides this description of the bank (condensed):

Wells Fargo & Company, a financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally. The company operates through four segments: The Consumer Banking and Lending segment offers diversified financial products and services for consumers and small businesses. The Commercial Banking segment provides financial solutions to private, family owned, and certain public companies. The Corporate and Investment Banking segment offers a suite of capital markets, banking, and financial products and services, such as corporate banking and investment banking. The Wealth and Investment Management segment provides personalized wealth management. The company was founded in 1852 and is headquartered in San Francisco, California.

Source: seekingalpha.com WFC

In the most recent SEC 10-K report, Wells Fargo described their business as such:

Wells Fargo & Company is a corporation organized under the laws of Delaware and a financial holding company and a bank holding company registered under the Bank Holding Company Act of 1956, as amended (BHC Act). Its principal business is to act as a holding company for its subsidiaries. References in this report to “the Parent” mean the holding company. References to “we,” “our,” “us” or “the Company” mean the holding company and its subsidiaries that are consolidated for financial reporting purposes.

At December 31, 2023, we had assets of approximately $1.9 trillion, loans of $936.7 billion, deposits of $1.4 trillion and stockholders’ equity of $185.7 billion. Based on assets, we were the fourth largest bank holding company in the United States. At December 31, 2023, Wells Fargo Bank, N.A. was the Company’s principal subsidiary with assets of $1.7 trillion, or 90% of the Company’s assets.

Source: Wells Fargo 10-K

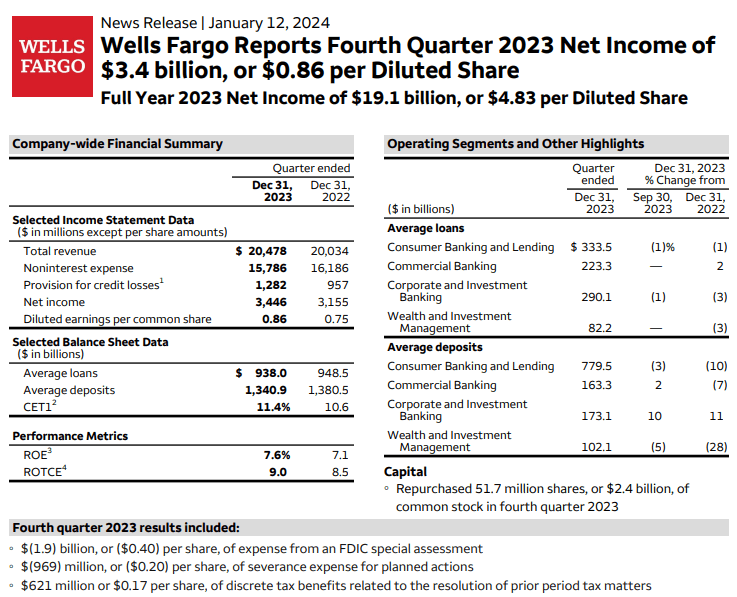

The following is from the Wells Fargo 4th quarter report.

{kind=link}

EPS improved to the point that only 2021 shows better results over the past decade, while Revenue Per Share was at record levels. Income seekers are still experiencing dividend levels far below what they reached before COVID, though both 2022 and 2023 saw the amount climb.

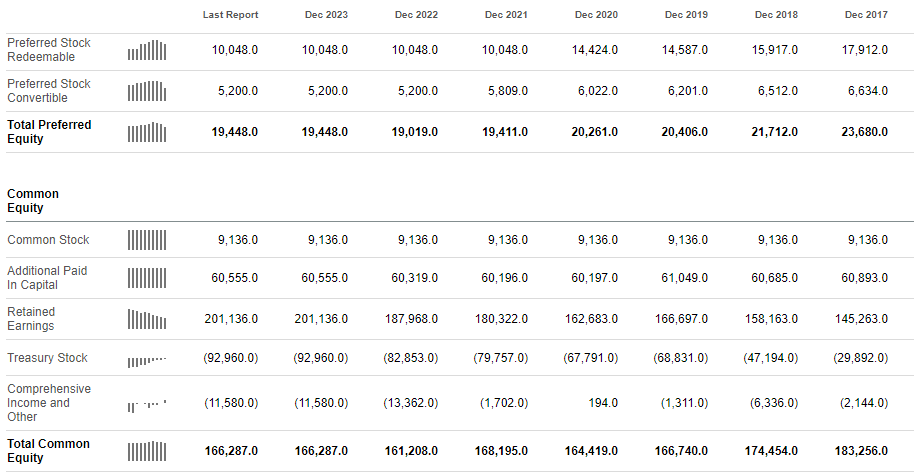

Results for the quarter showed improvements over the same time in 2022 for both EPS and ROE. The Wealth Management division though showed disappointing results. Right or wrong, my main ratio for preferred stockholders is how much common equity is there to cover all the outstanding preferred stock shares. For that, we turn to the Balance sheet.

seekingalpha.com Balance sheet

{kind=link}

Here we see that Total Common Equity has been unchanged since 2019, down from a peak the prior year. Offsetting that is WFC redeemed about 30% of the preferred stock outstanding during 2021, the results being a higher coverage ratio, which now stands at 8.6x, a very solid multiple! When you look at the current yields available, I see the market pricing in no chance of a missed payment, which stop the common stock dividend, and certain repayment if called. In line with that, the bank is redeeming one issue valued at $840m, improving the coverage ratio to 9.

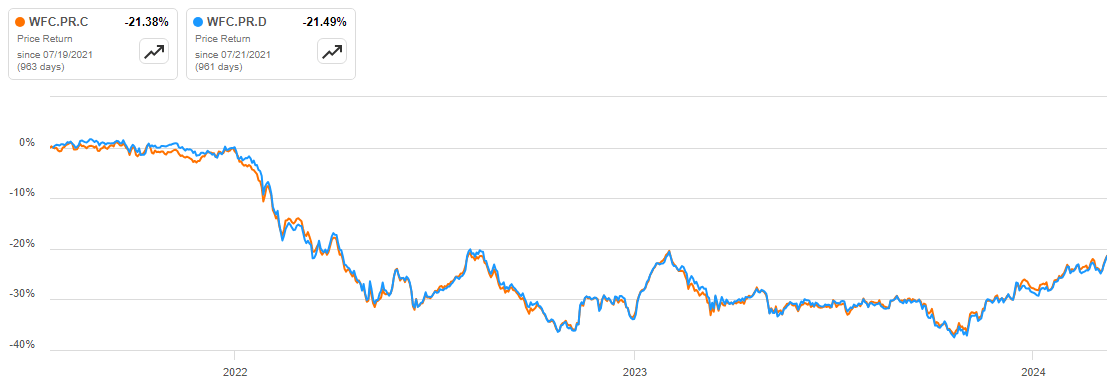

Preferred stock review

{kind=link}

As have most fixed income assets, prices started rising last fall with the hope that the FOMC would start cutting rates in early 2024. Compared to their floating-rate cousins, lower rates would benefit these fixed-rate preferreds more.

{kind=link}

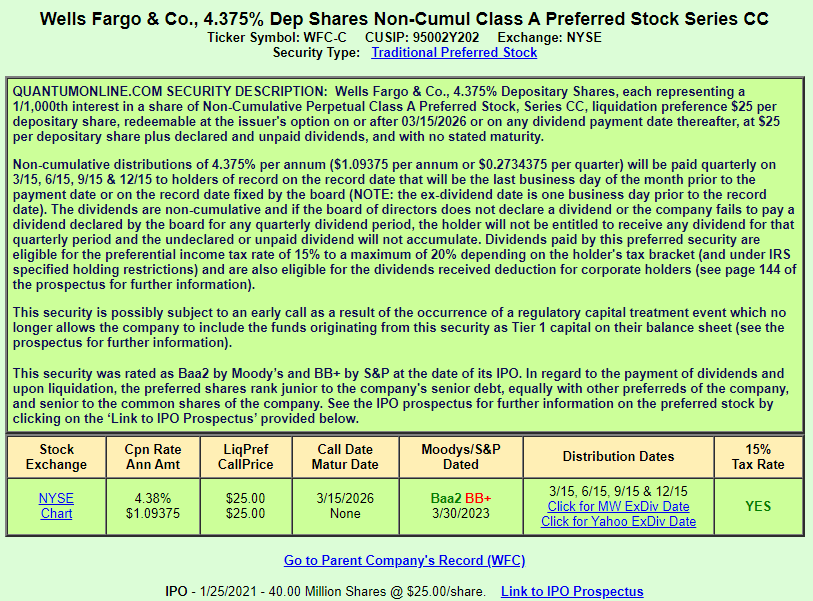

As you will see with the other preferred too, S&P rates both as non-investment-grade by one notch. That matches other US global banks where I think the best rating might have only been BBB-. This makes the holding ineligible for investment-grade funds and apparently “fallen angel” funds too as the VanEck Fallen Angel High Yield Bond ETF (ANGL) doesn’t own any Wells Fargo issues. That said, it…

Read More: Comparing Wells Fargo Series CC And DD Preferred Stocks (NYSE:WFC)