Earnings results often indicate what direction a company will take in the months ahead. With Q1 now behind us, let’s have a look at Roku (NASDAQ:ROKU) and its peers.

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

The 8 consumer subscription stocks we track reported a weaker Q1; on average, revenues beat analyst consensus estimates by 0.9%. while next quarter’s revenue guidance was 2.8% below consensus. Valuation multiples for many growth stocks have not yet reverted to their early 2021 highs, but the market was optimistic at the end of 2023 due to cooling inflation. The start of 2024 has been a different story as mixed signals have led to market volatility, and consumer subscription stocks have had a rough stretch, with share prices down 16.4% on average since the previous earnings results.

Best Q1: Roku (NASDAQ:ROKU)

Spun out from Netflix, Roku (NASDAQ: ROKU) makes hardware players that offer access to various online streaming TV services.

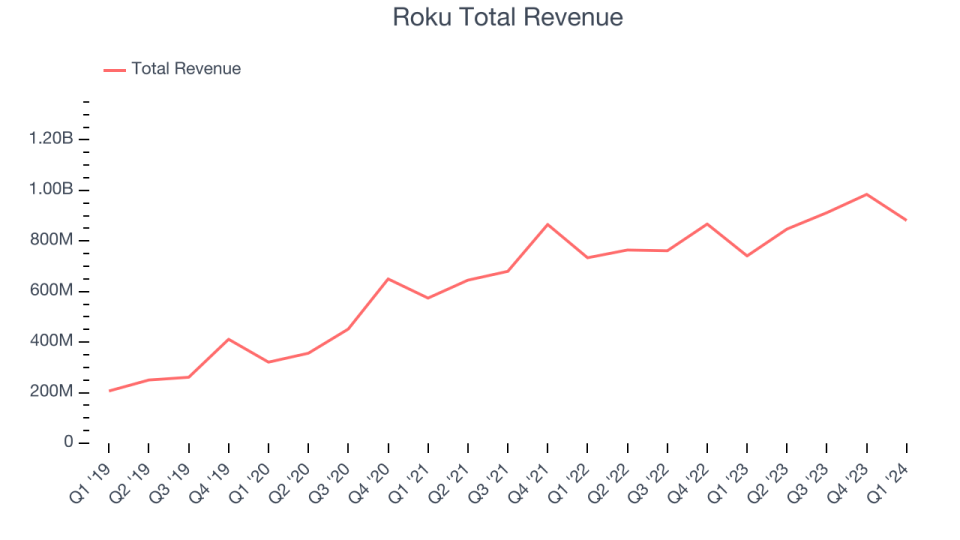

Roku reported revenues of $881.5 million, up 19% year on year, topping analysts’ expectations by 3.7%. It was a strong quarter for the company: Roku beat analysts’ revenue expectations and crushed adjusted EBITDA expectations. It also expanded its number of users. Guidance was similar to the results themselves, with Q2 revenue guidance roughly in line while adjusted EBITDA guidance was well ahead.

Roku scored the biggest analyst estimates beat of the whole group. The company reported 81.6 million monthly active users, up 14% year on year. The stock is down 13.9% since the results and currently trades at $54.1.

Is now the time to buy Roku? Access our full analysis of the earnings results here, it’s free.

Duolingo (NASDAQ:DUOL)

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

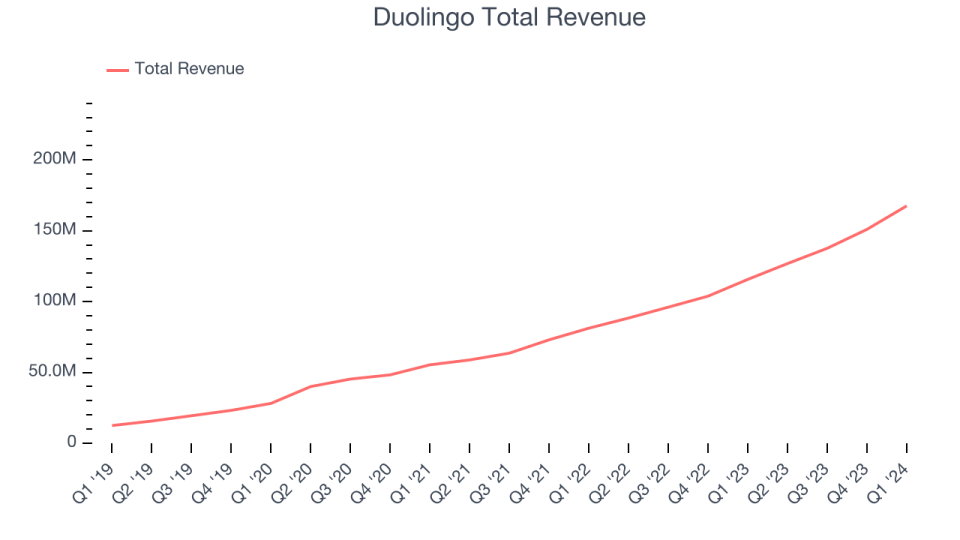

Duolingo reported revenues of $167.6 million, up 44.9% year on year, outperforming analysts’ expectations by 1.1%. It was a mixed quarter for the company: Duolingo delivered exceptional revenue growth, driven by more paid subscriber additions than expected. Its EPS also blew past analysts’ estimates. On the other hand, its revenue guidance for next quarter was underwhelming, though it upgraded its full-year revenue and EBITDA outlook, topping projections.

Duolingo scored the fastest revenue growth and highest full-year guidance raise among its peers. The stock is down 19% since the results and currently trades at $198.24.

Is now the time to buy Duolingo? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Chegg (NYSE:CHGG)

Started as a physical textbook rental service, Chegg (NYSE:CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Chegg reported revenues of $174.4 million, down 7.1% year on year, in line with analysts’ expectations. It was a weak quarter for the company, with a decline in its users and slow revenue growth.

Chegg had the slowest revenue growth in the group. The company reported 4.7 million users, down 7.8% year on year. The stock is down 57.7% since the results and currently trades at $3.04.

Read our full analysis of Chegg’s results here.

Netflix (NASDAQ:NFLX)

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

Netflix reported revenues of $9.37 billion, up 14.8% year on year, in line with analysts’ expectations. It was a mixed quarter for the company, with underwhelming revenue guidance for the next quarter and slow revenue growth.

The company reported 269.6 million users, up 16% year on year. The stock is up 7.4% since the results and currently trades at $656.1.

Read our full, actionable report on Netflix here, it’s free.

Udemy (NASDAQ:UDMY)

With courses ranging from investing to cooking to computer programming, Udemy (NASDAQ:UDMY) is an online learning platform that connects learners with expert instructors who specialize in a wide range of topics.

Udemy reported revenues of $196.8 million, up 11.6% year on year, in line with analysts’ expectations. It was a weak quarter for the company, with slow revenue growth and full-year revenue guidance missing analysts’ expectations.

The company reported 1.44 million active buyers, up 3.6% year on year. The stock is down 10.1% since the results and currently trades at $8.89.

Read our full, actionable report on Udemy here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.