Forget about Gamestop (NYSE:GME) and AMC Entertainment (NYSE:AMC). Robinhood Markets stock is the picks-and-shovels way to invest in the resurgence of meme stocks.

With meme stock mania seemingly heating back up, investors are eyeing shares of some of 2021’s big meme stocks again. But rather than chase shares of a specific meme stock, the smart way to invest in the theme of retail investors piling back into the market is to invest in Robinhood Markets, which will continue to benefit from the influx of retail investors and increased trading volume.

In this sense, Robinhood can be thought of as the picks-and-shovels way to play a return of retail activity. Unlike Gamestop or AMC, I believe it’s a great stock in its own right and doesn’t need any short squeeze to head higher.

I’m bullish on Robinhood stock based on its excellent user and deposit growth, its positioning as a picks-and-shovels play on increasing activity from retail investors, and its successful foray into new areas like IRAs and credit cards. The latter initiative is transforming Robinhood from a retail brokerage to a comprehensive financial powerhouse.

Meme Stock Reawakening

As you’ve likely seen by now, a Tweet from Keith Gill, aka Roaring Kitty, the ringleader behind Gamestop’s massive 2021 rally that set off the original “meme stock” mania, marked his return to the platform after a multi-year hiatus. Many investors took this as a signal to rush into Gamestop and other meme stocks of that era, sending shares of these stocks on a wild ride this week.

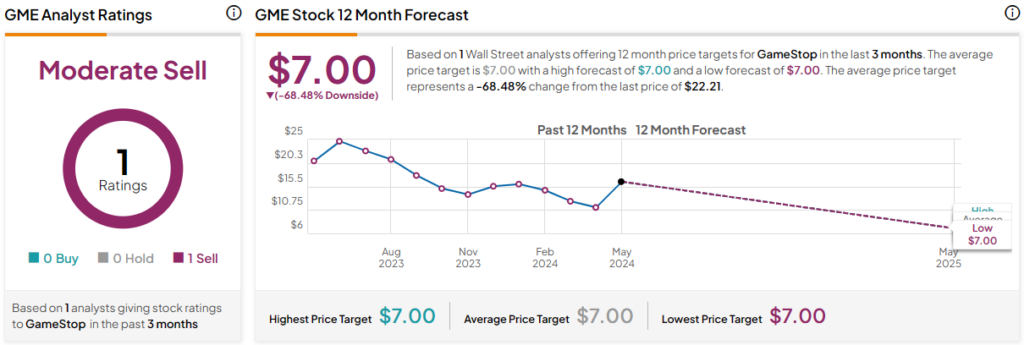

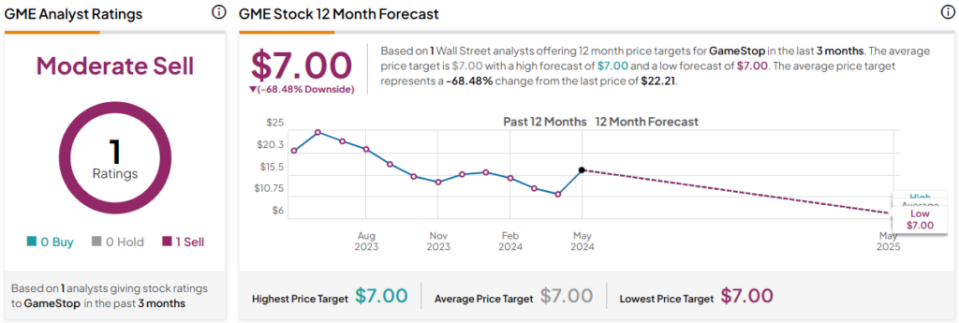

However, most of these investors would admit that this is a troubled company with less-than-promising long-term prospects, and the stock has considerable downside risk. For example, the GME stock’s price target of $7 shows that even after the recent pullback, the stock still has downside potential of 68.5% (see below). Meanwhile, Robinhood is a thriving, growing business with a bright future.

Picks-and-Shovels Play

As the go-to brokerage app for many new investors and retail investors, Robinhood is well-positioned to capitalize on an influx of new traders and a spike in trading activity. Currently, Robinhood is the #11 finance app in Apple’s App Store, trailing everyday payments apps like Cash App and Venmo but leading the likes of Fidelity, Charles Schwab (NYSE:SCHW), and Wells Fargo (NYSE:WFC), a considerable achievement for the much smaller company.

Robinhood recently released updated metrics for April, showing that business is booming. An impressive 90,000 customers opened accounts during the month, meaning that Robinhood now has 24 million customers. Robinhood also took in $4.9 billion in deposits. This represents a 45% annualized growth rate versus March. With this influx, the company has now taken in $27.4 billion in deposits over the last 12 months, representing 35% annualized growth versus April 2023.

And keep in mind that these numbers are from before the meme stock resurgence kicked off in May. As more retail investors return to the market or are drawn to the market for the first time by news of the wild swings of meme stocks, Robinhood’s user and deposit growth should continue.

This growth prompted Bank of America Securities to give Robinhood a double upgrade from Underperform to Buy, based on “(1) rising retail engagement and accelerating organic growth; (2) positive operating leverage after large expense reductions; (3) attractive valuation following increases in EBITDA/EPS.” Bank of America increased its price target on Robinhood from $14 to $24.

Beyond meme stocks, Robinhood has made great progress in building the platform, expanding into new areas, and becoming a true financial ecosystem for its users.

Attacking New Verticals

This isn’t the same old Robinhood that it was in 2021 during the last meme stock frenzy. I previously covered Robinhood and its underrated transformation into a full-service financial ecosystem several months ago, and the stock has performed well since then. Robinhood launched IRAs last year and has made an aggressive move into the market by offering a 1% match on rollover deposits and a 3% match on deposits for Robinhood Gold members.

These maneuvers are helping it attract customers from its competitors. CEO Vlad Tenev says that the first quarter was the second quarter in a row in which the company had “net asset inflows from every other major brokerage — totaling $3 billion, more than twice our Q4 level.”

Robinhood is also making a splash in the credit card market with the launch of its upcoming Robinhood Gold card, which will be one of the offerings within its Robinhood Gold subscription service.

The eye-catching gold card, which is made of stainless steel and weighs in at 17 grams, offers users unlimited 3% cash back on all purchases. Tenev says that over one million customers have signed up for the Gold card waitlist and stated, “We can substantially grow Gold adoption as we roll out the card.” The card could be a major growth driver for Robinhood Gold membership, as only half of the people on the waitlist are current Gold subscribers.

Tenev says that Robinhood Gold subscribers hit 1.7 million during the first quarter after 260,000 new customers signed up. With these new offerings, Robinhood is smartly leveraging its success with retail investors in its brokerage business to move into new verticals, increase wallet share with its customers, and capture further growth.

Is Robinhood Stock a Buy, According to Analysts?

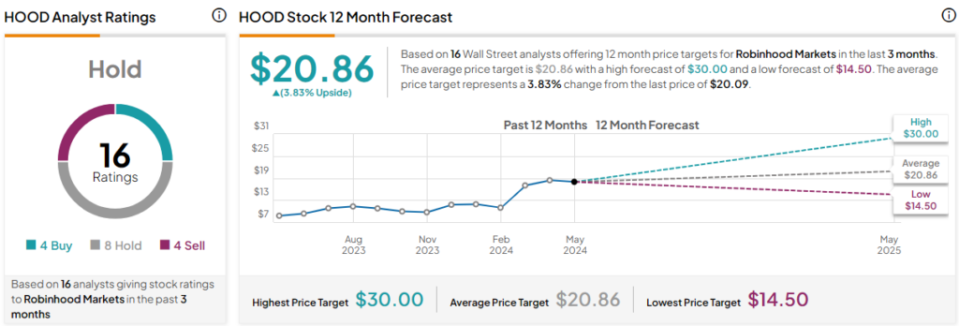

Turning to Wall Street, HOOD earns a Hold consensus rating based on four Buys, eight Holds, and four Sell ratings assigned in the past three months. The average HOOD stock price target of $20.86 implies 3.8% upside potential.

The Takeaway: An Up and Coming Financial Powerhouse

Rather than chasing after a stock like Gamestop during this meme stock revival, Robinhood could potentially be the best way to invest in a resurgence of retail investor activity. I’m bullish on Robinhood because of the strong user growth and deposit growth it has already demonstrated this year and because it’s well-positioned to capture further growth as more retail investors foray into the market.

Additionally, the company’s expansion into lucrative verticals like IRAs and credit cards and its momentum in these areas have the potential to transform it from a retail brokerage into a true financial powerhouse over time. This makes it an attractive long-term investment opportunity, in my view.