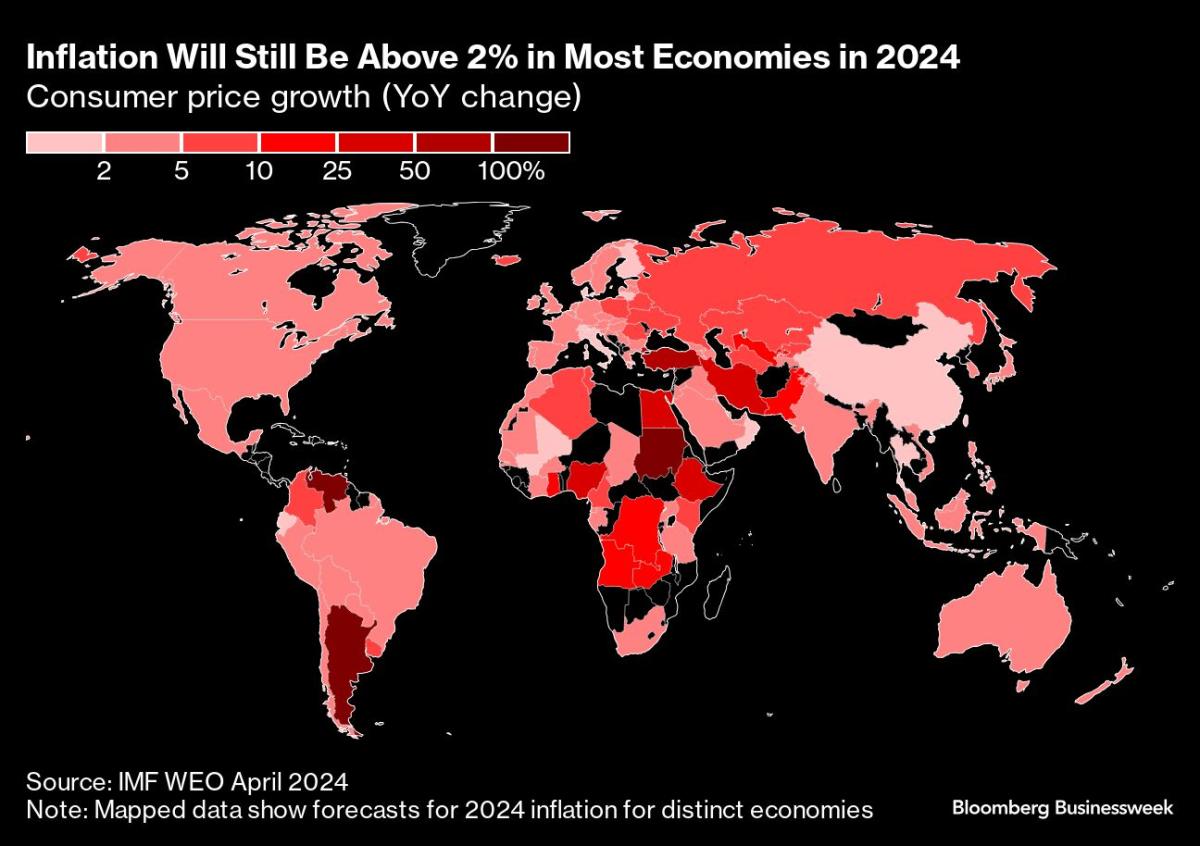

(Bloomberg) — Inflation-related releases across the Group of Seven will prime central bankers for crucial June interest-rate decisions, just as they meet in Italy to discuss the state of the world economy.

Most Read from Bloomberg

Days after US data revealed cooler-than-expected consumer-price growth, the UK, Canada and Japan will all publish numbers for April that are likely to go in the same direction. A euro-zone wage report, meanwhile, will also offer key evidence sought by policymakers.

Canada will be first, on Tuesday. While traders have pared back bets for a cut at its June meeting to less than 50% after recent hotter-than-expected jobs data, a fourth straight monthly easing of underlying price pressures in the inflation release would keep the door open for a reduction.

The next day, UK consumer-price growth is likely to have slowed drastically — by more than a percentage point — to near the 2% level targeted by Bank of England officials. With another monthly reading due on the eve of the June 20 BOE meeting, sustained evidence of dissipating inflation could give policymakers all the encouragement they need to reduce borrowing costs there too.

On Thursday, the European Central Bank will publish wage numbers, data it deems essential to judge underlying price dynamics. Growth in negotiated wages probably failed to slow significantly from the end of last year, heightening the case for caution as officials gear up for a widely flagged rate cut on June 6 and perhaps more easing after that.

What Bloomberg Economics Says:

“Data for early 2024 from Germany, France, Italy and Spain have already been published and they point to negotiated wages rising 4.3% year over year in the euro area during the first three months of the year. That’s only a slight slowdown from the 4.5% registered in 4Q23. A nearly steady pace of increase would be unlikely to derail the ECB’s first cut in June but will keep policymakers nervous about committing to additional easing.”

—David Powell, senior euro-area economist. For full analysis, click here

Finally, Japan’s data on Friday may show consumer-price growth, excluding fresh food, weakening to 2.2% from a year earlier, down from 2.6% in March. A deeper measure of inflation that strips out energy prices as well as fresh food is seen cooling to 2.5% after slipping below 3% in March for the first time since November 2022.

Bank of Japan officials are likely to draw different conclusions from their peers, though, as those readings would still extend the streak of outcomes at or above the 2% target to 25 straight months. As such, they would back the case for a rate hike as early as June 14 and no later than October, with the embattled yen serving as a risk factor for an early move.

Those data will arrive against the backdrop of a gathering of G-7 finance ministers and central bankers in the northern Italian lakeside resort of Stresa. The global economy features on the agenda, offering officials the chance to reflect on a diverging transatlantic outlook for rates: while Europe and Canada are leaning toward cuts, the US remains on a higher-for-longer path for now.

Elsewhere, the Federal Reserve will release minutes of its last meeting, and central bank decisions to keep borrowing costs on hold are likely from New Zealand to Turkey.

Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

US and Canada

The Fed will publish an account of policymakers’ April 30-May 1 gathering. In the press conference that followed that meeting, Chair Jerome Powell indicated rates will probably remain higher for longer because of lingering price pressures.

Several Fed officials have since echoed that sentiment, noting the need for more evidence that inflation is sustainably headed toward the Fed’s 2% goal.

Read more: Fed Officials Suggest Interest Rates Should Stay High for Longer

Vice Chair Philip Jefferson is among the central bankers due to speak or deliver remarks in the coming week. Fed Governor Christopher Waller is scheduled to speak on Tuesday on the economic outlook and policy.

The US economic data calendar is relatively light, with reports on April sales of previously owned homes on Wednesday and new houses the following day. Purchases of existing homes are seen little changed from the prior month, while contract signings on new houses are projected to have eased with mortgage rates back above 7%.

On Friday, data on April durable goods orders and shipments will include insight into companies’ appetite for capital investments. The University of Michigan will also issue its final May reading on consumer sentiment.

In Canada, aside from inflation data earlier in the week, retail sales numbers for March are due on Friday, offering insight into the strength of the consumer. The country’s two largest banks have already published analyses of customer credit and debit card data that suggest a slowdown in spending.

Asia

The People’s Bank of China is expected to hold its mortgage benchmark rates steady at the start of the week, keeping the five-year loan prime rate at 3.95% and 1-year at 3.45%.

Further out, the market has priced in modest cuts to the LPRs at some point over the next 12 months, as the PBOC aims to ramp up support for the property sector.

In New Zealand, the central bank is likely to maintain its hawkish hold on Wednesday even after inflation expectations cooled, as first-quarter consumer prices rose more than expected.

Elsewhere, central banks in Indonesia and South Korea are both seen standing pat while they eye potential reductions later this year, and the Reserve Bank of Australia publishes minutes from its May policy meeting.

Singapore, Hong Kong and Malaysia also release consumer inflation data. Australia, Japan and India get PMIs for May, and Japan, South Korea and New Zealand publish trade statistics.

Europe, Middle East, Africa

Purchasing manager indexes will be released for the euro zone and the UK on Thursday, giving a glimpse into the strength of manufacturing and services activity at the midpoint of the second quarter.

Consumer confidence in the euro area will also be published that day, while Britain’s latest reading of retail sales comes the following day.

BOE Governor Andrew Bailey delivers a lecture in London on Tuesday in honor of former policymaker Charles Goodhart. Concurrently, US Treasury Secretary Janet Yellen will be in Frankfurt to get an honorary doctorate at an event attended by ECB President Christine Lagarde and German Finance Minister Christian Lindner.

Fresh from their rate cut earlier this month, several Riksbank officials will speak in the coming week, starting on Monday with Governor Erik Thedeen.

At the other end of the wider region, data on Wednesday are expected to show South Africa’s inflation rate stayed steady at 5.3%.

Four key central bank decisions are scheduled:

-

Hungary is poised to cut the European Union’s highest rate on Tuesday, in what’s been flagged as the penultimate move before the end of the country’s monetary easing cycle.

-

The same day, policymakers in Nigeria are set to raise borrowing costs for an 11th straight meeting to show their resolve to crush inflation, now at a 28-year high. Analysts predict a full percentage-point increase, to 25.75%.

-

Officials in Egypt are poised to keep their rate unchanged at 27.25% on Thursday. Inflation has slowed for two straight months to 32.5%, and the central bank hopes a $50 billion-plus bailout will help it decelerate substantially by the end of the year.

-

The same day, Turkey’s central bank is forecast to hold its key rate at 50%, with monetary authorities believing inflation will soon peak at about 75% and then slow rapidly to below 40% by the end of 2024.

Latin America

Chile’s first-quarter output figures posted Monday likely jumped from year-end levels on the strength of falling interest rates, a firming labor market and higher global prices for copper, the country’s top export. The government on May 14 marked up its 2024 GDP forecast to 2.7% from 2.5%.

The country’s central bank on Thursday is all but certain to deliver a seventh straight rate cut from 6.5%, though faster-than-expected April inflation prints may cap the reduction to 50 basis points. Finance Minister Mario Marcel on May 16 said the easing cycle has quite a way to go.

Paraguay paused at 6% at last month’s meeting after eight rate cuts since August. Inflation ticked up to 4% in April, possibly keeping the central bank sidelined again this month.

In Mexico, the inflation-monetary policy dynamic is top of mind as stubbornly elevated consumer prices keep the central bank in a hawkish mood.

Though policymakers will get three more sets of inflation data, including this week’s mid-month prints, before their June 27 meeting, a rate cut next month is by no means a sure thing. The minutes of Banxico’s May 9 decision to pause may shed additional light on its new estimates for consumer prices.

Rounding out the picture in Latin America’s No. 2 economy, the final read on first-quarter GDP and March retail sales are also on tap.

–With assistance from Vince Golle, Robert Jameson, Laura Dhillon Kane, Tom Rees, Piotr Skolimowski, Monique Vanek, Paul Wallace and Alexander Weber.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.