Polaris (NYSE: PII) has grown into the leading powersports vehicle manufacturer in North America, with its sales rising sixfold since 2000. Over this time, Polaris has more than tripled the total returns of the S&P 500 index.

However, over the last decade, it has been an entirely different story. Despite doubling its revenue across the last 10 years, Polaris’ total returns have declined by 16% as the market continuously assigned lower and lower valuations to the company’s share price over time.

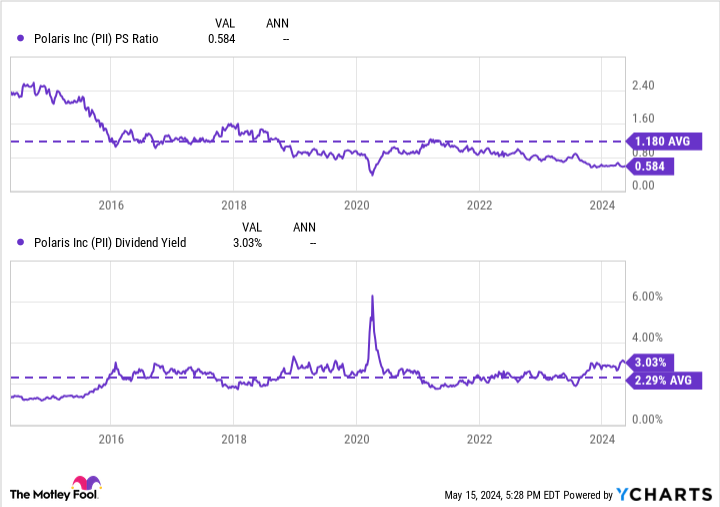

Now trading at its lowest price-to-sales (P/S) ratio since 2000 (outside of the 2009 and 2020 crashes), has Polaris become too intriguing to pass up — or is it a doomed business worthy of a deeply discounted valuation? Here’s why I’m thinking the former.

A market leader with a knack for finding new customers

Polaris operates through three business segments: Off-road (all-terrain and utility vehicles, plus snowmobiles), On-road (Indian and Slingshot motorcycles), and Marine (pontoons and deck boats). While the company’s segments are varied across many use cases, its operations are highly cyclical, as evidenced by the fact that its sales have declined for three consecutive quarters.

With its consumers hampered by rising inflation and higher interest rates, Polaris saw sales decline another 20% in the first quarter of 2024. Despite this underwhelming earnings report, there were four takeaways hidden within that highlight why Polaris could prove to be an exciting investment at today’s once-in-a-decade valuation.

No. 1 or No. 2 share in each of its markets

Polaris holds the No. 1 market share in North America in its largest sales cohort, off-road vehicles, and the top spot in pontoons and deck boats. Meanwhile, it holds the No. 2 spot in the snowmobile and motorcycle markets, rounding out a portfolio with healthy market shares in all of its niches.

What stood out in its last earnings call, though, was that even though sales plummeted 20%, Polaris grew market share in all of these groups except for snowmobiles. These gains emphasize that recent struggles have been industrywide and that, comparatively speaking, Polaris continues to outperform its niche.

Reliable utility vehicle demand

The company’s utility off-road vehicles make up over 40% of Polaris’s sales and have been historically reliable due to their importance to the end markets they serve. With customers ranging from farmers and ranchers to government departments, militaries, and enterprises, these utility vehicles are not really discretionary purchases and are vital for many work purposes.

Dominating this niche in the powersports market, Polaris somewhat protects itself from an industry often viewed as entirely discretionary and recreational.

Ability to find new customers

While these loyal utility vehicle customers create a valuable installed base of sales, the company’s ability to attract new customers remains as strong as ever. This fact was evident in the company’s recent results, as management believes that 70% of its sales in the first quarter came from customers new to Polaris vehicles.

One reason for this success is the company’s Polaris Adventures team, which partners with local outfitters to rent vehicles for an array of unique ride experiences across the United States. This unit has provided over 1.5 million rides since 2017 across its 250 locations, and management believes customers are twice as likely to buy a Polaris vehicle after going on an Adventures ride.

The potential for falling inflation and interest rates

CME Group recently calculated that the odds of the Fed cutting interest rates in September increased from 65% to 73% after a better-than-expected inflation report. While higher inflation and interest rates are not doomsday-like issues for Polaris, lower figures are certainly better for its consumers as their dollar would go further and financing would become cheaper. Should things keep trending toward lower inflation with a few interest-rate cuts, the discretionary verticals that struggled in the first quarter could rebound amid higher consumer confidence.

A once-in-a-decade opportunity

While these four factors make Polaris an intriguing investment proposition on their own merit, the company’s once-in-a-decade valuation makes it even more alluring.

Trading at just 0.6 times sales and with a 3% dividend yield that is 30% higher than its 10-year average, Polaris is undeniably cheap. Despite this deep discount, the company has delivered positive earnings per share and free cash flow (FCF) every year since it went public in 1987.

Thanks in part to this steady FCF generation, Polaris has increased its dividend payments for 29 consecutive years. Even after this incredible run of dividend payments, its payouts still only used 48% of the company’s FCF during a challenging last 12 months, leaving room for future increases.

While dividend growth has slowed in recent years, the reason why should be music to investors’ ears. Forgoing significant dividend increases in favor of large stock buyback plans, the company has capitalized on its discounted valuation lately, retiring 14% of its outstanding shares over the last decade.

Thanks to this shrewd allocation of cash returns to shareholders, along with the company’s surprisingly robust operations and discounted valuation, Polaris looks to be a magnificent stock to buy and hold for years.

Should you invest $1,000 in Polaris right now?

Before you buy stock in Polaris, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Polaris wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $578,143!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Josh Kohn-Lindquist has no position in any of the stocks mentioned. The Motley Fool recommends CME Group. The Motley Fool has a disclosure policy.

A Once-in-a-Decade Opportunity: 1 Magnificent Dividend Stock Down 36% to Double Up On Right Now was originally published by The Motley Fool