For the record, attempting to perfectly time your trades’ entries and exits is usually a bad idea. Predicting a stock’s (or the broad market’s) short-term ebb and flow simply can’t be done with any consistency.

As a means of optimizing the balance of risk and reward, though, sometimes there’s a case to be made for hurrying up or holding off on a new position.

Google parent Alphabet (NASDAQ: GOOG)(NASDAQ: GOOGL) is forcing such a choice on interested investors right now. While this Thursday’s earnings report in and of itself isn’t a reason to buy or sell the stock, if you were mulling a purchase of Alphabet shares anyway, you might want to go ahead and take the plunge now. Here’s why.

There’s a reason the previous post-earnings stumble didn’t last

Don’t misread the message: If you choose to step into a new Alphabet stake after it posts its first-quarter numbers after Thursday’s close on April 25, you’ll be fine. A year from now, you probably won’t care either way or even remember if it mattered.

However, there’s a reasonably good chance Alphabet stock’s going to move higher rather than lower in response to its Q1 numbers.

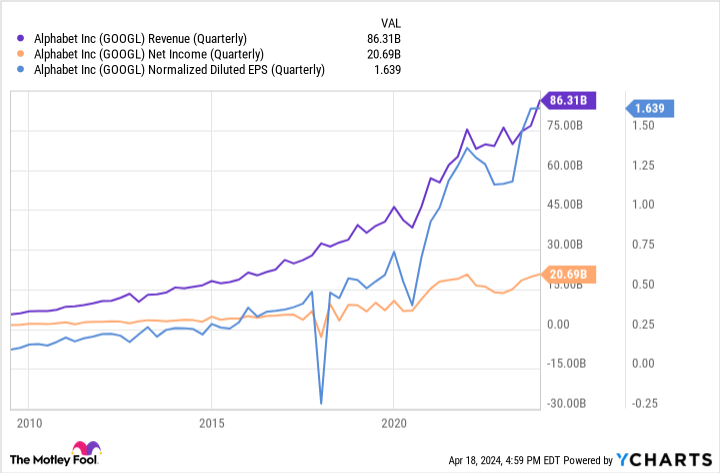

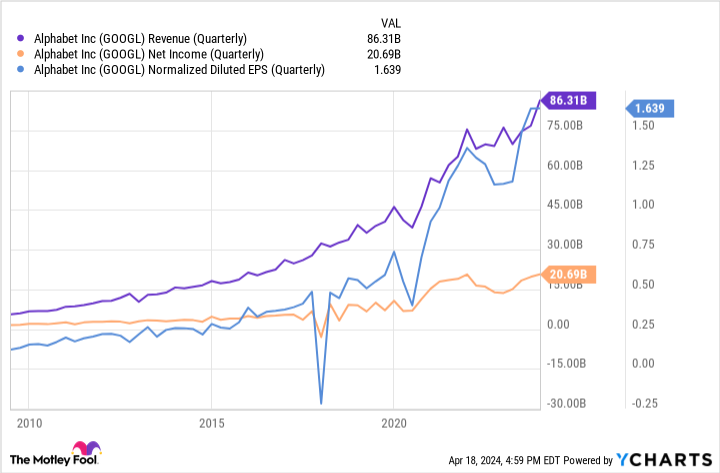

That wasn’t the way it happened a quarter earlier. Although the company topped both its revenue and earnings estimates, its ad revenue of $65.5 billion fell just a bit short of the $65.9 billion analysts were anticipating. Since this is Alphabet’s single-biggest business, the stock tumbled more than 7% on the news.

Then a funny thing happened. Although shares waffled a bit for the next couple of trading days, within a couple of weeks they were well above its post-earnings low. Now, nearly three months later, Alphabet stock is above its previous pre-earnings peak.

What gives? It’s not a tough matter to figure out. With some time to consider all the numbers, investors decided they liked Alphabet’s fourth-quarter results after all.

And well they should. Overall revenue was up 13% year over year, with YouTube’s top-line growth of 15.5% taking up the slack seen on other fronts. Operating income for all of its advertising business was collectively up 32%.

In fact, the ad revenue that came up short of expectations was still up 11% year over year. In the meantime, all of its most important numbers rolled in better than expected, maintaining the company’s rekindled streak of earnings beats in addition to extending an uninterrupted (except for the second quarter of 2020, when the COVID-19 pandemic was in full swing) multiyear streak of year-over-year quarterly revenue growth.

It’s unlikely the market will make the same mistake with this stock again — at least not this soon. Indeed, investors may be underestimating Alphabet now, setting the stage for a post-earnings pop.

Two key catalysts for Alphabet stocks

Forecasters clearly got the company’s Q4 ad revenue wrong; they’ve probably adjusted their future calls accordingly in the meantime. Analysts may have even overcorrected them, in fact, just to be sure they don’t repeat the more serious mistake of overestimating how well a company is doing. (Underestimating a corporation’s performance is considerably more forgivable, particularly if you at least correctly predict in which direction its numbers are moving.)

There are a couple of potential catalysts lurking in the upcoming first-quarter report, however, that are more than a little likely to light a fire under this stock. The first of these catalysts is YouTube’s ad revenue.

As was noted, YouTube’s advertising sales were up a healthy 15.5% during the final quarter of 2023. The online video platform has continued to widen its reach, though. Video-viewership ratings house Nielsen reports that YouTube and Netflix are the only two major streaming platforms to grow their share of total U.S. view time during the first quarter of 2024. That being said, YouTube ultimately takes top honors here by virtue of generating more total view time than Netflix does.

Alphabet’s cloud computing business could also prove inspirational to onlooking investors. This arm swung to a profit in the first quarter of last year, and while it’s remained in the black and even widened its bottom line since then, this young business’s profitability has also remained difficult to forecast.

That’s been a source of short-lived setbacks for Alphabet stock in the meantime. As time marches on, though, the company’s cloud computing business is becoming more predictable, dialing back the risk of unpleasant surprises.

Alphabet also recently unveiled a home-grown artificial intelligence (AI) processor that can legitimately compete with AI hardware powerhouse Nvidia. This unveiling happened in conjunction with the launch of new updated coding options for AI-minded users of its chat-based personal assistant app Gemini. If the upcoming earnings conference call can successfully relay the potential of this new tech and these new tools, that too could prove bullish for the stock.

Analysts are already starting to see this potential, by the way, to the extent it might help the stock after Thursday’s Q1 report. For instance, JPMorgan believes the new-and-improved version of Google’s Gemini could accelerate the company’s cloud revenue growth to a pace of 20%, if not more.

Taking action now is the lower-risk move here, but…

Is this a guarantee that shares will fight their way higher following Thursday afternoon’s release of Alphabet’s first-quarter numbers? Of course not. There are always potential pitfalls. It’s also possible the market itself will be sinking then, dragging this stock lower with it despite a healthy quarterly report.

It’s also worth repeating that for long-term investors, any such short-term volatility doesn’t really matter. If you’ve got the itch to at least try to squeeze out a few dollars’ worth of additional profits on a position, though, the bigger calculated risk here is in waiting rather than acting before Thursday’s close. And if for some reason you don’t step in before Thursday and the stock ends up falling following the release of earnings, Alphabet shares are most definitely worth buying on that dip. Remember, the tumble following its Q4 results was certainly a great entry opportunity.

Oh, by the way, the analyst community expects Alphabet to report revenue of nearly $74 billion and earnings of $1.42 per share. Both numbers are measurably above year-ago comparisons.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $466,882!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 15, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, JPMorgan Chase, Netflix, and Nvidia. The Motley Fool has a disclosure policy.

Should You Buy Alphabet Stock Before Thursday? was originally published by The Motley Fool