Nvidia (NASDAQ: NVDA) became a hot stock last year when its shares soared 239% over the 12-month period. The company’s chips became the go-to for artificial intelligence (AI) developers worldwide, leading Nvidia’s earnings to skyrocket.

In 2024, Nvidia’s stock has continued to hit new heights, with its share price up 76% since the market closed out 2023. The tech giant remains on a promising growth trajectory, with its business likely to benefit from the tailwinds of AI and other tech sectors for years.

Nvidia’s meteoric rise has some analysts questioning how much room the company has left to run. However, its stock keeps defying expectations. Given the massive potential of AI and the chipmaker’s dominating position in the market, I wouldn’t bet against it over the long term.

So, here’s why Nvidia stock remains a screaming buy right now.

Profiting from tech tailwinds

As a leading chipmaker, Nvidia has a powerful position in tech. In addition to supplying its hardware to AI developers, the company’s chips power a wide range of devices, from cloud platforms to video game consoles, laptops, custom-built PCs, and more.

Nvidia is the primary supplier to Nintendo‘s Switch game console, a partnership that has put the chipmaker’s hardware into mainstream consumer use. The Nintendo Switch is the third-best-selling console of all time, selling 139 million units to date.

However, the best reason to invest in Nvidia remains its AI prospects. Data from Grand View Research shows the AI market hit close to $200 billion last year and is expected to expand at a compound annual growth rate of 37% until at least 2030. That projection would see the industry reach nearly $2 trillion by the end of the decade. There seems to be no end in sight to the soaring demand for AI GPUs, and that’s good news for Nvidia.

Last year, Nvidia’s head start saw it achieve an estimated 90% market share in AI chips, leading to soaring earnings.

In its most recent quarter (the fourth quarter of fiscal 2024, which ended in January), the company’s revenue increased by 265% year over year to $22 billion. Operating income jumped 983% to nearly $14 billion. This monster growth was primarily thanks to a 409% increase in data center revenue, reflecting a spike in AI GPU sales.

Additionally, Nvidia’s free cash flow is up 430% in the last year to more than $27 billion, significantly higher than chip rivals AMD‘s $1 billion and Intel‘s negative $14 billion. Despite new GPU releases from both competitors, Nvidia has more significant cash reserves to continue investing in its technology to retain market supremacy.

Nvidia is trading at its best value in months

Last year, Nvidia became the first chipmaker to achieve a market cap above $1 trillion. Its market cap is currently over $2 trillion, making Nvidia the world’s third-most valuable company, after Microsoft and Apple.

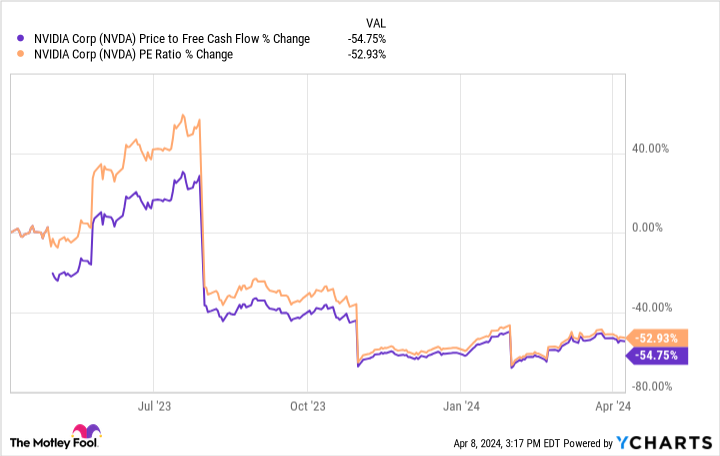

Nvidia has come a long way in a short time, yet its stock has actually become a better value over the last 12 months based on price-to-earnings and price-to free-cash-flow.

The chart below shows that Nvidia’s price-to-free-cash-flow and price-to-earnings ratios plunged in the last year, indicating its stock is at one of its best-valued positions in 12 months.

P/E is calculated by dividing a company’s stock price by its earnings per share (EPS). Meanwhile, the price-to-free-cash-flow ratio divides its market cap by free cash flow. These are helpful valuation metrics, as they take into account a company’s financial health. For both, the lower the figure, the better the value.

Nvidia’s plunging figures for both metrics make its stock an attractive buy given the bright promise for the business’s future.

Estimates indicate Nvidia will continue to outperform the S&P 500

Nvidia has an exciting outlook for the coming years; estimates of its earnings per share (EPS) are optimistic.

The chart above shows that analysts think Nvidia’s earnings could hit close to $36 per share by fiscal 2026. Multiplying that figure by its forward price-to-earnings ratio of 35 yields a stock price of $1,260.

If it hit that number that would be a stock rise of 44% over the next two years. That would not replicate the stock’s 2023 move, but would beat the S&P 500‘s 24% growth over the previous two years.

Nvidia still has much to offer new investors and is a stock worth considering right now.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Microsoft, and Nvidia. The Motley Fool recommends Intel and Nintendo and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Is Nvidia Stock a Buy? was originally published by The Motley Fool