Buying when other investors are worried is not an easy task, but it is one of the most reliable ways to find discounted stocks. You just have to go in with a grain of salt, making sure that you focus on buying good companies that are capable of withstanding whatever negatives have other investors concerned about the future.

Today it looks like there is a long-term opportunity to buy Canadian Imperial Bank of Commerce (NYSE: CM), Bank of Nova Scotia (NYSE: BNS), and Toronto-Dominion Bank (NYSE: TD) while they still appear to be trading at a discount.

A word about Canadian banks

CIBC, Scotiabank, and TD Bank, as they are more commonly known, all share one important feature. As Canadian banks, they are subject to far more stringent regulations than in most other countries, like the United States.

The largest Canadian banks, a group that includes the three listed here, have been afforded a somewhat protected status. This is because Canada doesn’t seem to like bank mergers, so smaller competitors don’t have the opportunity to get big, larger banks can’t merge to join the ranks of the giants, and even industry giants have a hard time buying smaller Canadian banks to increase their scale.

On top of that, Canada’s banking regulations tend to result in banks taking a conservative approach to business operations. That’s true in both their home market and abroad (the banks above have some exposure to non-Canadian markets as they seek to grow over time).

So Canadian banks are a good option for more conservative dividend investors. CIBC, Scotiabank, and TD Bank held their dividends steady during the Great Recession, when many of the largest U.S. banks ended up cutting theirs.

Canadian Imperial Bank of Commerce

A little over 70% of CIBC’s business is derived from its home market. That’s higher than the two other banks here and something of a worry for investors today.

Canada’s property market has been on a tear, but rising interest rates have Wall Street worried that loan defaults will become an issue. That’s entirely possible, but CIBC has a strong tier 1 capital ratio of 13% (higher is better) and a long history of supporting its dividend through difficult times (it wasn’t cut during the Great Recession, for example).

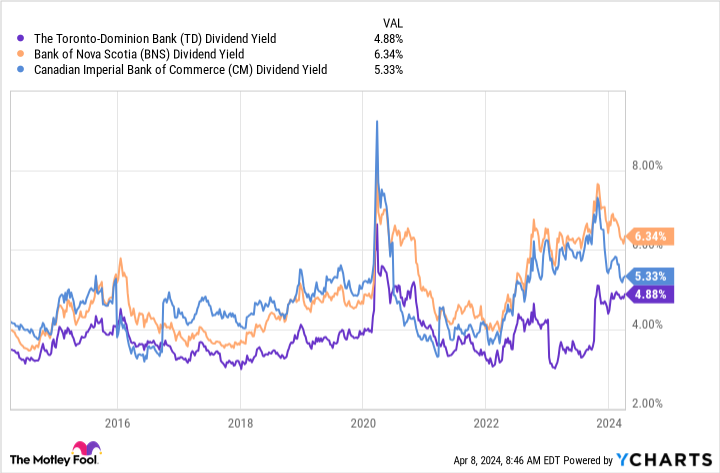

The worries have subsided a bit, with CIBC’s stock rallying a little of late. But the negative view hasn’t fully gone away, with the 5.3% dividend yield still near the high end of the 10-year yield range. If you can handle a little near-term uncertainty, this Canadian focused bank is worth a deep dive.

Bank of Nova Scotia is changing things up

Scotiabank’s stock has also been rallying of late, but its 6.2% dividend yield remains near the high end of its historical range, as well. The story, however, is vastly different than CIBC’s.

Scotiabank’s most notable attribute is its exposure to South America. That region was expected to grow more quickly than the mature Canada and U.S. However, Scotiabank hasn’t been able to turn that opportunity into financial growth. Thus, investor concerns have left it trading with a higher yield than its peers.

Management is shifting gears in an effort to boost lagging financial performance, including in metrics like earnings growth and return on equity. Part of the strategy is to exit less desirable South American markets to focus on more attractive ones, like Mexico.

The key to the story right now is that the payout ratio is above the company’s target range, but management is OK with this over the short term. The company expects improved performance driven by the business overhaul to bring the payout ratio back into the desired range over time.

Assuming you can sleep well amid a corporate reshuffle, this high-yield stock looks like it will be getting safer over time.

Toronto-Dominion Bank is going the wrong way

TD Bank’s share price has been falling, driving the yield higher, while most of its peers have seen improving stock prices, and falling yields. The bank’s roughly 5% dividend yield is near the highest levels in recent history. Using that as a rough gauge of valuation, TD Bank is probably the most discounted stock here.

The story is twofold. There’s the exposure to the Canadian housing market. But TD Bank is also dealing with a big setback in its U.S. growth plans.

An acquisition was called off by U.S. regulators worried about the bank’s money laundering controls. That means that U.S. acquisitions are probably off the table for a period of time (though the bank can still open new locations organically). There’s also likely to be a fine involved.

But TD Bank’s tier 1 capital ratio is the third highest in North America at 13.9%, so it seems ready to weather any hardships that might come its way. And while growth might slow down, it hasn’t stopped.

Now is a good time to jump aboard this North American banking giant as it muddles through a rough patch. Investors will probably give the stock a higher valuation once acquisition-led growth resumes in the U.S. market. Meanwhile, you can collect a generous dividend yield while you wait for that to happen.

Collect the high yields while you can

There are legitimate reasons for investors to be worried about CIBC, Scotiabank, and TD Bank. But these conservative Canadian banks have worked through hard times before and continued to reward income investors very well. If you can think like a contrarian, taking the long-term view, now is the time to consider these Canadian banks and their historically attractive dividend yields.

Should you invest $1,000 in Toronto-Dominion Bank right now?

Before you buy stock in Toronto-Dominion Bank, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Toronto-Dominion Bank wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $533,869!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 8, 2024

Reuben Gregg Brewer has positions in Bank Of Nova Scotia and Toronto-Dominion Bank. The Motley Fool recommends Bank Of Nova Scotia. The Motley Fool has a disclosure policy.

3 High-Yield Bank Stocks to Buy at a Discount was originally published by The Motley Fool