(Bloomberg) — As a 20-year-old trainee at a now-defunct German bank, Robert Stheeman’s first job was running the industrial paper cutter to slice the coupons off bond certificates, sometimes 500 pages thick.

Most Read from Bloomberg

It was a role that set the course for a career that would take him to the top of Britain’s bond market, overseeing the biggest explosion of public sector borrowing in a generation.

In UK finance, there are few people as instrumental and long-lasting as Stheeman, who will have raised more than £3 trillion ($3.8 trillion) for the country when he steps down from a 21-year run as head of the debt office. To some London bond traders, that makes him “the most important person that the average person on the street has never heard of.”

Now as Stheeman prepares to retire, he says the challenge facing his as-yet-unannounced successor is how to ensure the liquidity and stability of the market that he helped create.

That task is getting more complicated as the UK gets ready for another borrowing spree this year — some £265 billion in all — and the central bank sells down its stash of gilts bought under quantitative easing. All of that debt will need to find buyers amid a glut of competing issuance from governments around the world.

“That’s why resilience of the market is so essential,” Stheeman said in an interview.

That resilience happens a few ways. For one, it’s about striking the balance between how much money the government needs to raise and how to make it palatable to investors whose taste for long or short-dated debt is constantly in flux. It’s also about ensuring the loyalty of a select group of investment banks, known as Gilt-edged Market Makers, even as hedge funds, algo traders and other kinds of players become a bigger part of the market.

The Debt Management Office acts as a go-between, turning the spending plans handed down by the Treasury into the nuts and bolts of bond sales. The department, which was spun out of the Bank of England in 1998 and has no say in fiscal policy, largely works behind-the-scenes, picking bond maturities to sell and making sure auctions run smoothly.

Bankers who’ve worked with Stheeman describe him as calm under pressure. Deutsche Bank’s Neal Ganatra said he helped instill confidence in the market, while Sam Hill at Lloyds Banking Group’s LBCM unit praised his “steady, predictable” approach to issuance.

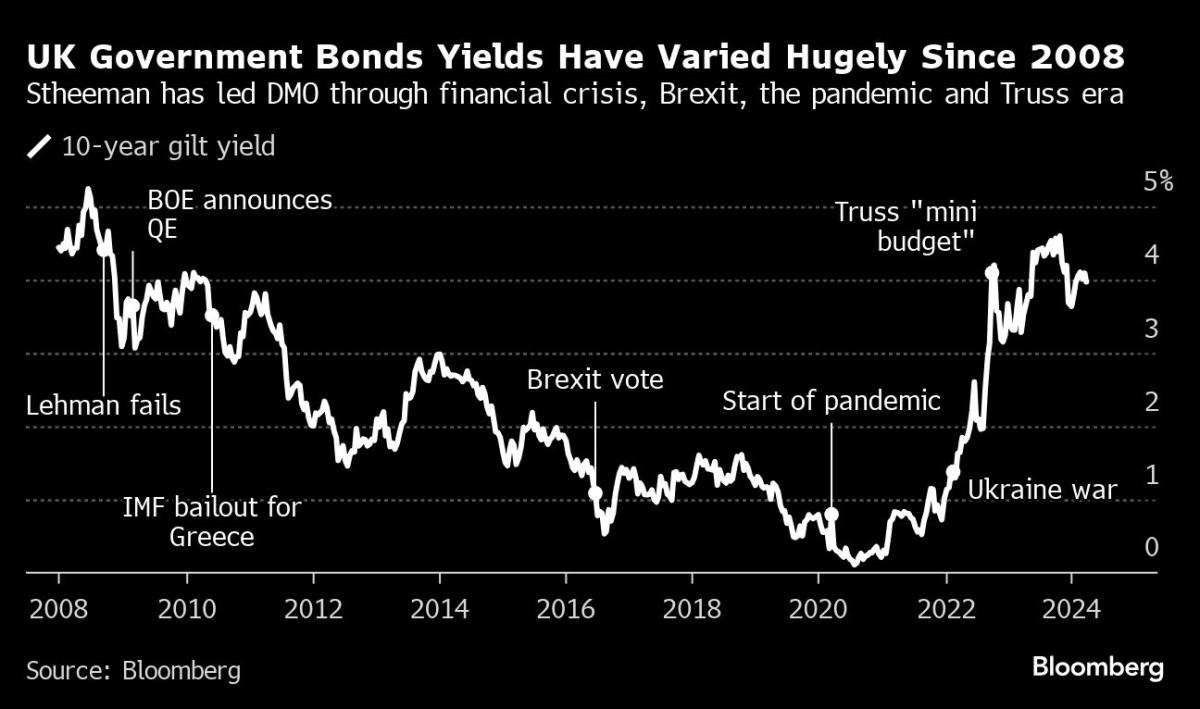

The role gave Stheeman a front-row seat to 2022 turmoil caused by UK Prime Minister’s Liz Truss unfunded tax cuts that unleashed the biggest bout of volatility in the gilt market’s history. For future politicians, he has a warning about the risk of ignoring markets.

“The market is not something that you can bludgeon into accepting your point of view,” Stheeman said. “It’s the market’s view that ultimately policymakers and politicians need to take account of. There’s no point in railing against that view.”

It’s an issue that has resonance given the US’s mammoth debt burden and the debate over whether a Trump-era package of sweeping tax cuts, due to expire at the end of 2025, will be extended. Last month, Phillip Swagel, director of the Congressional Budget Office, warned in an interview with the Financial Times that if the US government ignores the rising levels of federal debt, the country faces the risk of a Truss-style market shock.

Others like Treasury Secretary Janet Yellen have argued the extra borrowing is manageable, given that the larger public debt load hasn’t imposed much of an interest burden, at least so far.

The UK government will also be asking investors to buy more bonds. The DMO’s fundraising target for 2024 is the biggest-ever — excluding the emergency financing that followed the pandemic in 2020.

With so many bonds to sell, Stheeman’s successor will have to make tough decisions to keep the UK’s coffers full without overpaying. It’s a lesson that Stheeman himself learnt just a few years into his tenure at the DMO when the collapse of Lehman Brothers was roiling markets.

Then, at the height of the financial crisis, his office rejected a clutch of low-ball investor orders for a UK debt auction, reasoning that they offered poor value for taxpayers. That so-called failed auction in March 2009 prompted a slump in gilts, exacerbating the most volatile episode for UK debt in a decade, and eliciting a statement from the prime minister defending the market’s underlying strength. Stheeman, who was required to write a letter to the government explaining his decision, said his goal was to protect the UK taxpayer.

It’s an episode that gives Stheeman pause — even after all these years — as the only auction that ever stumbled on his watch.

“It was necessary,” he reflects. “It was a very, very intense day. But I didn’t leave the office at the end of the day feeling miserable.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.