Genuine Parts (NYSE:GPC) is highly regarded by income investors. It is an esteemed member of the elite group of stocks known as Dividend Kings. With 68 years of consecutive dividend hikes, the automotive, replacement, and industrial parts specialty retailer boasts one of the most commendable track records. Thus, shares rarely trade at a discount. With strong earnings growth contrasting last year’s soft share price action, the valuation has slipped to attractive levels. I have, thus, grown bullish on this quality operator.

Dividend Kings Rarely Go on Sale

Through my experience researching dividend growth stocks, I have realized that the members of an elite group of dividend stocks rarely go on sale. These tend to be high-quality companies with excellent track records of earnings and dividend growth. Accordingly, investors are usually willing to pay a premium valuation for these stocks.

This seems to hold true both for Dividend Aristocrats (stocks that have increased their dividends for 25+ years and are members of the S&P 500 (SPX)) and Dividend Kings (stocks that have increased their dividends for 50+ years, irrespective of index inclusion). As a result, I have found that buying these stocks when their valuations correct to more reasonable levels can end up being a wise decision.

I believe this holds true for GPC stock today. But before we go deeper into this, let me commend this stock for its almost unparalleled track record of annual dividend increases. You see, Genuine Parts is not “just” a Dividend King, with only 55 other companies boasting this title, but its 68-year dividend growth track record is the second-longest in the world.

The only other company boasting a lengthier track record is American States Water (NYSE:AWR), with 69 years. Genuine Parts shares second place with Dover Corp. (NYSE:DOV) and Northwest Natural Gas (NYSE:NWN), which have also grown their dividends for 68 consecutive years.

Speaking of quality growth track records, Genuine Parts has maintained a commendable pace of growth over the years despite being a well-matured company with decades of consistent growth. For context, over the past 10 years, Genuine Parts has grown its earnings per share and dividend per share at a compound annual growth rate (CAGR) of 7.8% and 5.9%, respectively. FY 2023 was no different. In fact, EPS reached another record, with growth even reaccelerating.

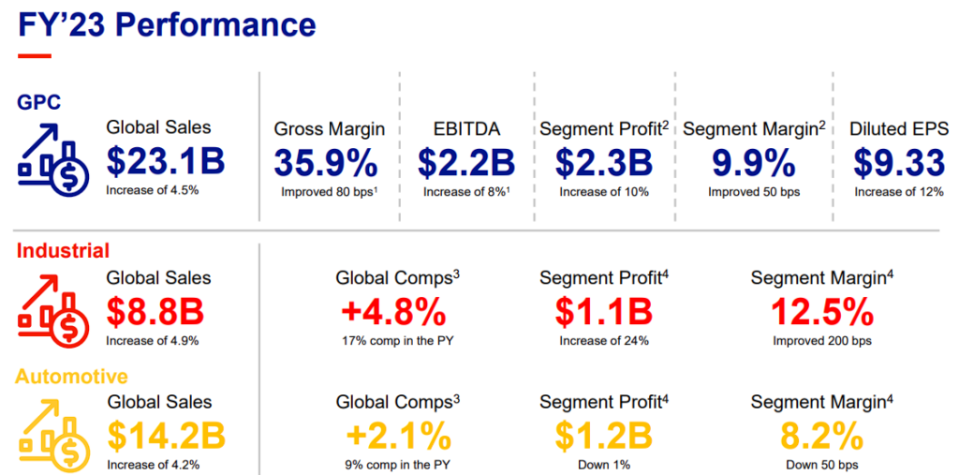

FY 2023: Another Year of Record Earnings

As mentioned earlier, Genuine Parts posted strong earnings growth in FY 2023. Given that the share price doesn’t seem to have responded accordingly, the stock’s valuation appears to be hovering at attractive levels. Thus, let’s take a look at Genuine Parts’ FY-2023 report, in which the company celebrated another year of record earnings.

For the year, Genuine Parts posted record revenues of $23.1 billion, an increase of 4.5% compared to the previous year. The 3.1% growth in comparable sales and 2% growth stemming from acquisitions more than offset the 0.4% headwind from FX movements and another 0.2% headwind from other effects.

Along with modest revenue growth, Genuine Parts recorded a gross margin of 35.9% and a segment margin of 9.9%, up 80 basis points and 50 basis points, respectively. Also, the company repurchased 1.8 million shares for $261 million, reducing its share count by about 1%. All these factors combined led to earnings per share coming in at a record $9.33, up 12.3% on a GAAP basis, or up 11.9% on an adjusted basis.

Management expects that the company’s earnings growth momentum will persist in FY 2024, forecasting that adjusted earnings per share will land between $9.70 and $9.90. This implies a year-over-year expansion of 5% at the midpoint despite a tough comp coming off of FY 2023.

The Valuation Has Fallen Below Past Averages

As stated above, Genuine Parts achieved notable earnings growth in FY 2023, setting the stage for FY 2024 to be another year of record earnings. Despite this, the share price has experienced soft action lately, leading to a modest valuation compression. Currently trading at a forward P/E of 15.7x, Genuine Parts trades below its historical average of about 18x.

Above-average interest rates somewhat justify a below-average multiple. However, the notable earnings growth in FY 2023, coupled with analysts’ expectations of a 7% CAGR over the next five years, enhances Genuine Parts’ investment appeal. When considering the company’s excellent qualities and growth track record, this creates an attractive risk/reward investment case, in my view.

Is GPC Stock a Buy, According to Analysts?

Checking Wall Street’s view on the stock, Genuine Parts has a Moderate Buy consensus rating based on three Buys and three Holds assigned in the past three months. At $157.67, the average Genuine Parts stock price target suggests 5.1% upside potential over the next 12 months.

The Takeaway

To sum up, Genuine Parts presents a compelling investment case for dividend growth investors. Boasting an exceptional 68-year track record of dividend growth plus competitive earnings and dividend growth rates to this day, the company proved its commitment to reward shareholders a long time ago.

With earnings growth poised to remain robust and in line with its historical average over the medium term, Genuine Parts likely presents an appealing entry point today. This is especially true as the stock trades at what seems to be a rather attractive valuation.