A Citi analyst recently upgraded his price target on high-yield energy stock Devon Energy (NYSE: DVN) from $52 to $55, signaling a potential 13.6% upside. Coupled with the current 5% dividend yield, this presents a promising opportunity for investors. Here’s a look at what makes Devon Energy such an attractive stock for Wall Street and retail investors.

Citi’s upgrade

The upgrade is interesting because it highlights the improvements in Devon Energy’s assets, notably its natural gas assets. This is often overlooked when investors assess the stock. It shouldn’t be because Devon has sizable gas reserves, and the collapse in the price of gas is a big reason for the decline in the company’s dividend in 2023.

Devon Energy’s reserves

The company has a lot of proved developed and undeveloped reserves in gas and natural gas liquids.

|

Resource |

Proved developed and undeveloped reserves at YE 2023 |

Proved developed and undeveloped reserves (in billions of barrels of oil equivalent*, MMBoe) |

|---|---|---|

|

Oil |

786 million barrels |

786 MMBoe |

|

Gas |

3,182 billion cubic feet |

530 MMboe |

|

Natural Gas Liquid (MMBbls) |

500 million barrels |

500 MMboe |

Data source: Devon Energy presentations. *Oil equivalent converts all resources to an equivalent measure based on energy output. 6 thousand cubic feet of natural gas = 1 barrel of oil

Why Devon Energy’s dividend declined in 2023

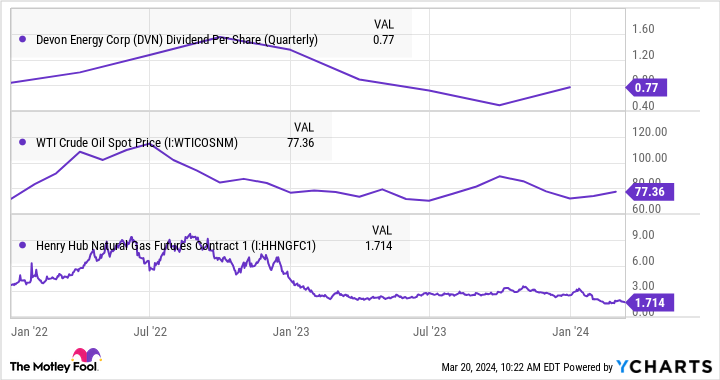

The chart below demonstrates the significant decline in the price of gas since the start of 2022 (down more than 50% over the period, while the price of oil is up double digits over the same period). The decline played a role in the reduction of Devon Energy’s variable dividend. For reference, the company pays a quarterly fixed dividend of $0.22 a share and a variable dividend from the remaining free cash flow (FCF) after the fixed dividend has been paid and share buybacks have occurred.

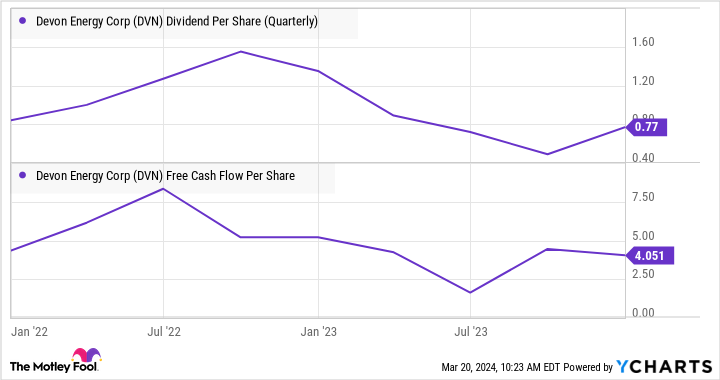

The chart below shows how the decline in FCF per share led to a decline in the dividend. I’ve also included Devon’s outstanding shares to demonstrate that management’s buybacks have resulted in a decline in the share count, which is good for ongoing holders as it increases their claim on cash flows.

The critical point is that the main reason for the fall in the dividend from 2022 to 2023 (which partly caused the disappointing share price performance) is lower FCF due to lower gas prices. Devon increased its revenue from oil production (despite a 6% decline in the realized price of oil) from the first quarter of 2022 to the fourth quarter of 2023.

Why Devon Energy can outperform in 2024

I’ve focused on Devon’s gas operations to lead into why the stock is attractive for investors right now.

First, the decline in the price of gas means oil is a more significant part of its overall revenue at present. By my calculations its oil production has gone from 75% of revenue in the first quarter of 2022 to 82% in the fourth quarter of 2023. With the price of oil above $80 a barrel, Devon’s prospects look good in 2024.

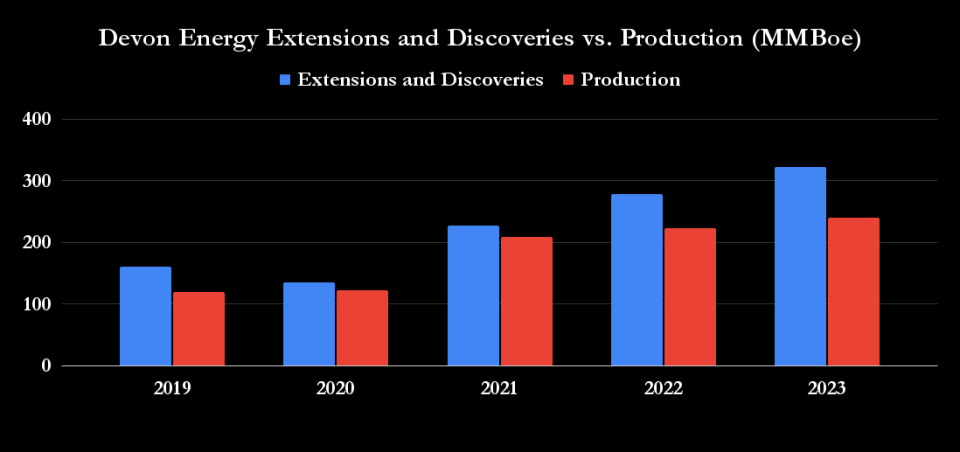

Second, as the Citi analyst intimated, Devon is a good operator of assets and is also good at improving its reserves. As you can see below, its extensions and discoveries have outpaced production over the last five years.

Third, on the fourth-quarter earnings presentation, management estimated its FCF yield (at the then share price of around $44) would be 9%, assuming a price of oil per barrel of $75 and 13% at a price of oil per barrel of $85. Interpolating those numbers with today’s share price of $48.30 produces an FCF yield of about 10% for a price of oil per barrel of $80. It’s a figure that implies Devon can pay an extremely attractive dividend in 2024 while also making share buybacks.

Is Devon Energy a stock to buy?

All told, investors shouldn’t underestimate the impact of falling gas prices on Devon’s dividend cut in 2023. However, with gas a lower part of its revenue and the price of oil remaining relatively high, the company is set to make substantial returns to investors this year.

As such, the Citi analyst is right to highlight the investment case for the stock, and Devon stock has upside potential.

Should you invest $1,000 in Devon Energy right now?

Before you buy stock in Devon Energy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Devon Energy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 21, 2024

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Wall Street Just Got More Bullish on This High-Yield Energy Stock was originally published by The Motley Fool