(Bloomberg) — Canadian oil driller Crescent Point Energy Corp. — which has overhauled its operations over the past five years — is changing its name to reflect its new identity.

Most Read from Bloomberg

The new moniker of Veren, a blending of the Latin word for “truth” and the English word “energy,” is being unveiled at an investor presentation Wednesday and will be voted on at the firm’s annual meeting in the coming months. The name Crescent Point referred to a road near the family cottage of one of the company’s co-founders.

For Chief Executive Officer Craig Bryksa, who took the reins in 2018, the change marks the culmination of his push to turn a producer with a reputation for excessive dealmaking and a grab bag of assets in Saskatchewan, Utah and North Dakota into a disciplined driller focused squarely on two Alberta oil and gas plays.

“The management team, the board, the corporate culture, the portfolio: Everything is significantly different than it was six years ago,” Bryksa, 47, said in an interview. “Being where we are today, on the back end of that transformation, we thought it was time to write the next chapter for this company.”

The overhaul began a little more than a year after Bryksa was named permanent CEO, starting with sales of assets in Utah and Saskatchewan, followed by acquisitions from Shell Plc and Paramount Resources Ltd. to build a presence in Alberta’s Kaybob Duvernay resource play.

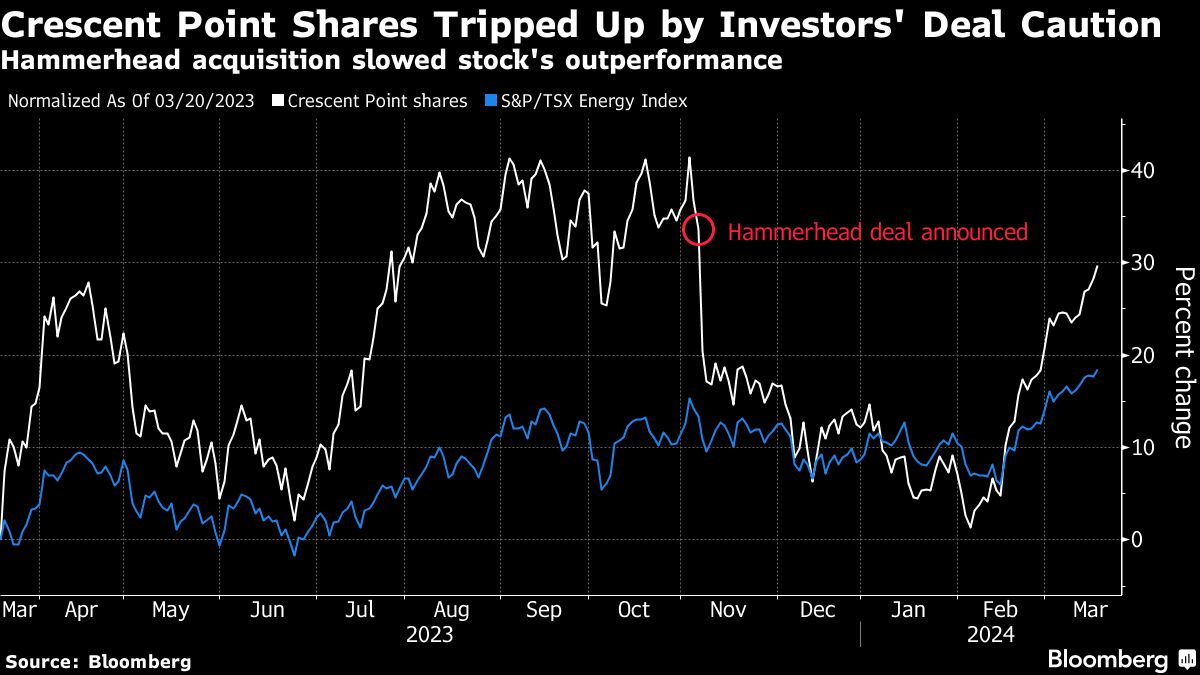

More recently, the company has established itself as a significant player in the province’s prolific Montney formation with a C$1.7 billion ($1.3 billion) acquisition from Spartan Delta Corp. and the C$1.96 billion takeover of Hammerhead Energy Inc. announced in November.

While Crescent Point’s shares are outperforming those of its Canadian energy peers, the Hammerhead deal has held back the stock and increased the company’s debt.

Bryksa said the opportunity to snap up those assets in what he called “the last deal we needed to complete the transformation” was fleeting and the company had to take it. The company will now take a “good long pause on acquisitions” and focus on reducing its debt and increasing the amount of capital it returns to shareholders through buybacks and dividends, he said.

The message has won over many of the analysts who cover the stock, with 15 rating the shares “buy” against one “hold” and no sell ratings. The main risks to the company are a drop in oil and gas prices and the execution of its drilling program, according to Royal Bank of Canada analyst Michael Harvey.

“Crescent Point’s future growth is highly dependent on continued drilling success within its development plays,” Harvey said in a recent note.

Still, Harvey rates the shares a buy and has a target price of C$13, up about 20% from current levels.

The other potential stumbling block for Crescent Point is that it’s paying down debt at a time when many other producers have already done so. That means they’re consistently shelling out 75% or more of their free cash flow to shareholders, compared with 60% for Crescent Point.

Bryksa counters that the company will be boosting production at a compound annual rate of 6% for the next five years, plus it has decades of drilling inventory ahead.

“Ideally, the market sees not only the competitive returns that are going to be coming their way, but also the sustainability of that,” Bryksa said. “We’ve completely rebuilt this portfolio, and we have the opportunity in front of us for not only five years or 10 years, but beyond that.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.