(Bloomberg) — US funding markets are offering signs of encouragement to the Federal Reserve as it determines exactly how and when to slow the pace at which it drains excess cash from the financial system.

Most Read from Bloomberg

Short-term funding markets have been stable, and for now, stress free. That offers considerable flexibility and a positive backdrop as Fed officials meet this week — and likely discuss the path ahead for quantitative tightening, or QT.

To Mark Cabana, head of US interest-rates strategy at Bank of America Corp., policymakers will have to explain “how comfortable are they pulling that cash out of a banking system” that seems to prefer having elevated reserve and cash levels, he said on Bloomberg’s Surveillance.

Read More: The Fed Has a Lot of Questions to Answer About Its Balance Sheet

Here are short-term markets, measure and facilities market participants are watching as the Fed assess QT:

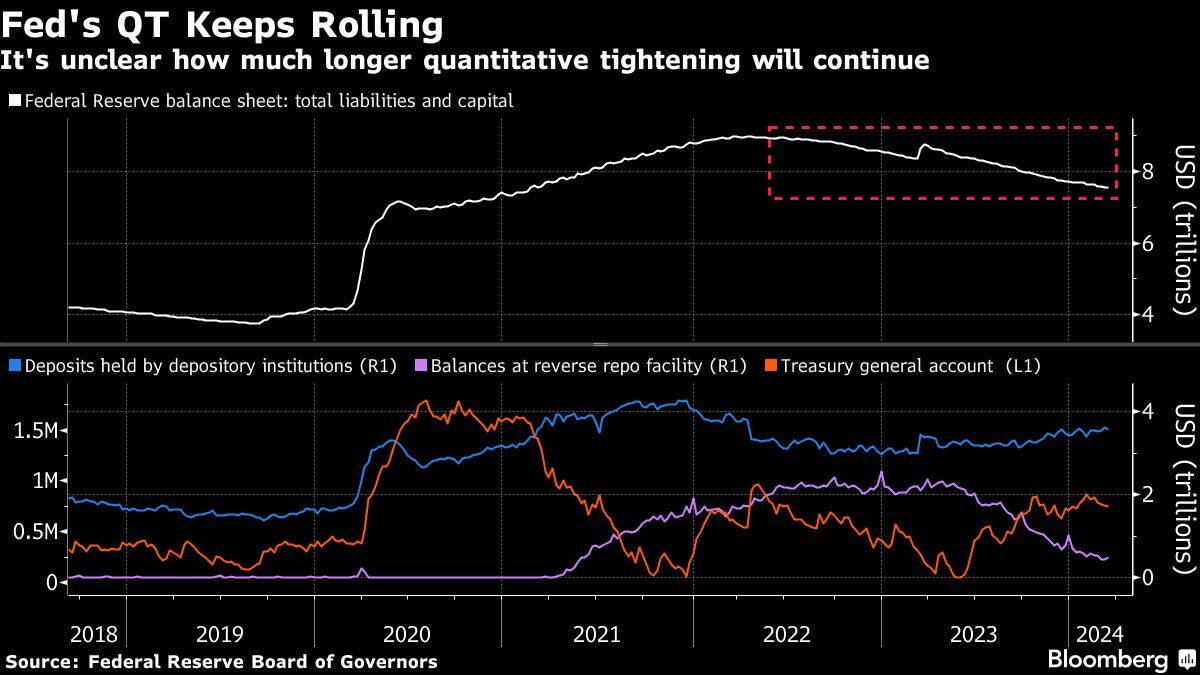

Bank Reserves and Reverse Repo

As the Fed carries on with QT, most market watchers expect usage to keep falling at the Fed’s overnight reverse repo facility, or RRP — a barometer of excess liquidity in the financial system. Balances have already dropped by about $1.7 trillion since June 2023.

Angst has been building around what happens when the RRP is completely empty, an eventuality that Barclays Plc sees possible as soon as the end of April. At that point, the Fed’s balance sheet unwind will likely start draining bank reserves.

Questions linger about how much cash can leave those coffers before institutions grow uncomfortable. Some Wall Street strategists insist that demand is higher than officials think due to the fact that banks have been paying more to retain those excess reserves.

Funding Rates

As reserves dwindle, the spread between the effective fed funds rate and the repo-related Secured Overnight Financing Rate is expected to eventually widen.

The rationale is that if reserves become more scarce, investors will rely more on the private market for repo. That will in turn put upward pressure on market rates and related benchmarks, like SOFR. The gap between SOFR and the fed funds rate on an overnight basis is currently 2 basis points in favor of the central bank benchmark. Swap markets indicate the spread is likely to be inverted about a year from now.

T-Bill Supply

While the Fed has been letting Treasury securities roll off its balance sheet, the US government has ramped up borrowing via larger public debt auctions.

Even as the Treasury has boosted the size of its coupon auctions, bill supply has born the brunt of the increases, having raised about $2.4 trillion on net since the beginning of 2023 — the bulk of which came after the debt ceiling was resolved in June.

This impact has shown up in the pricing of T-bills relative to other risk-free rates, like those on overnight index swaps. Securities are finally yielding more than OIS, but the narrow gap suggests appetite for short-dated government debt is still robust.

FX Swaps

Beyond US-based instruments, foreign-exchange swap markets may be affected by the Fed balance-sheet reduction. Cross-currency basis swaps tied to the euro and British pound could widen as US reserve balances are poised to drop faster than the excess liquidity at the European Central Bank and Bank of England.

The ECB’s reserves will only slow after the full redemptions of its long-term refinancing operations. And since the Bank of England started QT in September, its balance sheet runoff has accelerated — though usage of its short-term repo facility is marginally used.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.