(Bloomberg) — The Federal Reserve will begin in-depth discussions about its balance sheet this week, including when and how to slow the pace at which the central bank drains excess cash from the financial system.

Most Read from Bloomberg

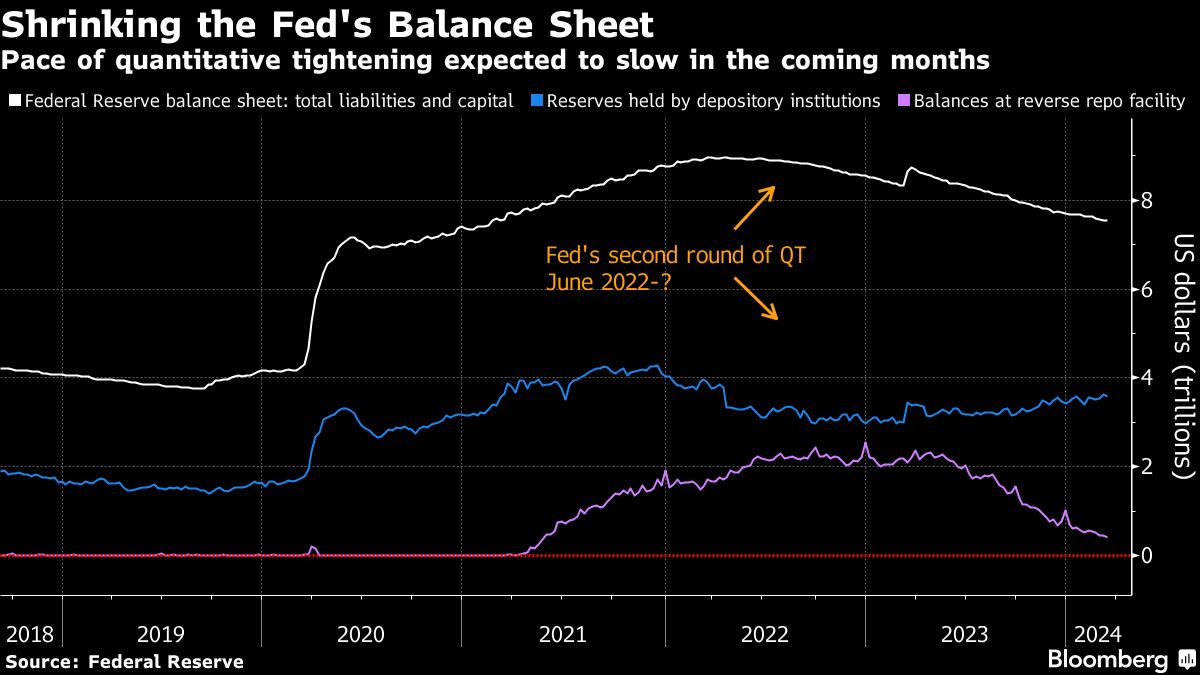

At the heart of this debate is how much more policymakers can shrink the Fed’s $7.5 trillion portfolio of assets before worrisome cracks — similar to those seen in 2019 ahead of an acute funding squeeze — start to appear.

Since 2022, the Fed has been letting as much as $60 billion in Treasuries and as much as $35 billion in agency-backed mortgage debt mature each month and roll off its balance sheet, a process known as quantitative tightening. But the central bank can’t maintain that pace forever.

Questions are mounting about what will motivate officials to slow the pace of runoff, the timing of such an announcement, how long the unwind can continue and what the central bank’s balance sheet will look like when it’s all over.

Why is the Fed talking about this now?

Policymakers are determined to avoid the type of market disruption that occurred the last time the Fed attempted to shrink its balance sheet.

In 2018, the central bank was letting as much as $30 billion in Treasuries and as much as $20 billion in agency-backed mortgage debt run off — roughly half the size of the current plan — before it decided to start slowing that pace the following year.

But by the time the Fed did so, market pressures were already evident.

The combination of increased government borrowing and a corporate tax payment created a shortage of reserves in September 2019, driving a five-fold surge in a key lending rate and a spike in the federal funds rate above the target range. The Fed was forced to intervene to stabilize the market.

Read More: Repo Market’s 2019 Blowup Is Haunting the Fed’s Latest QT Talk

Though market indicators suggest bank reserves are still abundant, there are some signs it might be time for the Fed to start thinking about the pace of QT.

What are officials watching?

Dallas Fed President Lorie Logan has said it’s time to begin planning an eventual slowdown of the balance-sheet unwind, emphasizing gauges she thinks should steer the runoff.

That includes balances at the overnight reverse repurchase agreement facility (RRP) — a barometer of excess liquidity in the financial system — which have fallen about $1.7 trillion since June and are hovering around $440 billion.

Officials are also watching for any signs of market stress. So far there haven’t been many, but bouts of volatility at the end of November and December did drive the Secured Overnight Financing Rate — a key benchmark tied to the repo market — to all-time highs.

When will tapering start?

That’s one of the biggest questions for the Fed at the moment.

Logan said earlier this month that the central bank needs to feel its way, noting that when RRP balances approach a low level it will be appropriate to slow the pace of runoff. But it’s unclear exactly when that will happen and whether that thinking is shared by other members of the Federal Open Market Committee.

That’s made it difficult for Wall Street strategists to discern when QT tapering will begin, with most forecasts stretching from May to September. This decision is entirely independent of when the Fed decides to lower interest rates.

Read More: Fed Seen Sticking With Three 2024 Cuts Despite Higher Inflation

Of the myriad factors that could delay the start, the most notable is tax season and the growth of the Treasury’s cash balance — one of the largest liabilities on the Fed’s balance sheet. A larger influx of tax receipts could lead the Treasury to issue less short-term debt, potentially driving more cash back to the RRP.

Logan has also underscored that slowing the pace of runoff does not mean stopping it.

How much longer can the Fed shrink its balance sheet?

Once the QT slowdown is underway, some think the Fed could continue unwinding its balance sheet well into 2025. However, that’s going to depend on the optimal level of reserves — an unknown point at which the financial system has enough liquidity and overnight market rates are steady.

Fed Chair Jerome Powell has said the central bank would like to have a buffer above the lowest comfortable level of reserves in the system but has provided no specific figure. A Fed survey of banks in September suggested that level of scarcity might be notably higher than policymakers think.

That’s partly because many banks now prefer to hold more reserves to ensure they have enough liquidity and are even paying up to protect their cash holdings.

Strategists from Bank of America and Morgan Stanley believe that once the reverse repo facility is completely empty, short-term rates from SOFR to fed funds will start moving higher within the central bank’s target range. This is because banks will likely continue doing everything they can to hold on to those reserves.

–With assistance from Catarina Saraiva.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.