(Bloomberg) — When the Federal Reserve raises interest rates, US households — in aggregate — usually get a boost to interest income that outweighs the extra cost of servicing debt. Not this time.

Most Read from Bloomberg

The annual interest bill that Americans pay on mortgages, credit cards and other debt has climbed by almost $420 billion since the Fed started tightening policy in March 2022, according to the latest numbers from the Bureau of Economic Analysis. The rise in interest income over the same period was only about $280 billion.

The upshot: Unlike every other Fed hiking cycle of the past half century, the latest one triggered a sharp decline in household net interest income.

Of course, the direct effect on interest costs and income is only one of the ways that Fed rates shape American household finances. A more important one is via the job market. When monetary policy tightens, businesses have to pay more to service their own debt, so they often seek to trim costs elsewhere by laying off workers or keeping wages down, though that hasn’t happened yet in the current cycle.

Still, research by Bloomberg Economics shows that net interest income, which was still considered a plus for consumer spending at the start of 2022, had become a significant drag by the middle of last year.

Floating Rates

There’s likely a combination of reasons the Fed’s hikes over the last two years had a different effect than in earlier cases.

On the spending side, interest costs rose faster this time because Americans now have a larger share of their debts in consumer credit, which is quicker to reprice and saddles borrowers with bigger bills when rates go up. Mortgages, by contrast, are mostly locked-in beyond the Fed’s reach.

Read More: Americans Now Pay as Much Interest on Other Debt as on Mortgages

As for interest income, one reason it’s lagged is that banks were slow to pass on higher rates to depositors — they’ve come under fire for that all over the world. And after about 15 years in which rates were near zero much of the time, savers may have gotten out of the habit of moving cash between accounts in search of better returns.

Another is that wealth has shifted out of the kind of holdings that pay interest, and into stocks. During the pandemic, for the first time on record, dividends overtook interest payments as a source of unearned income for Americans.

To be sure, aggregate numbers rarely tell the whole story, and in the case of interest income and payments they tell even less of it than usual.

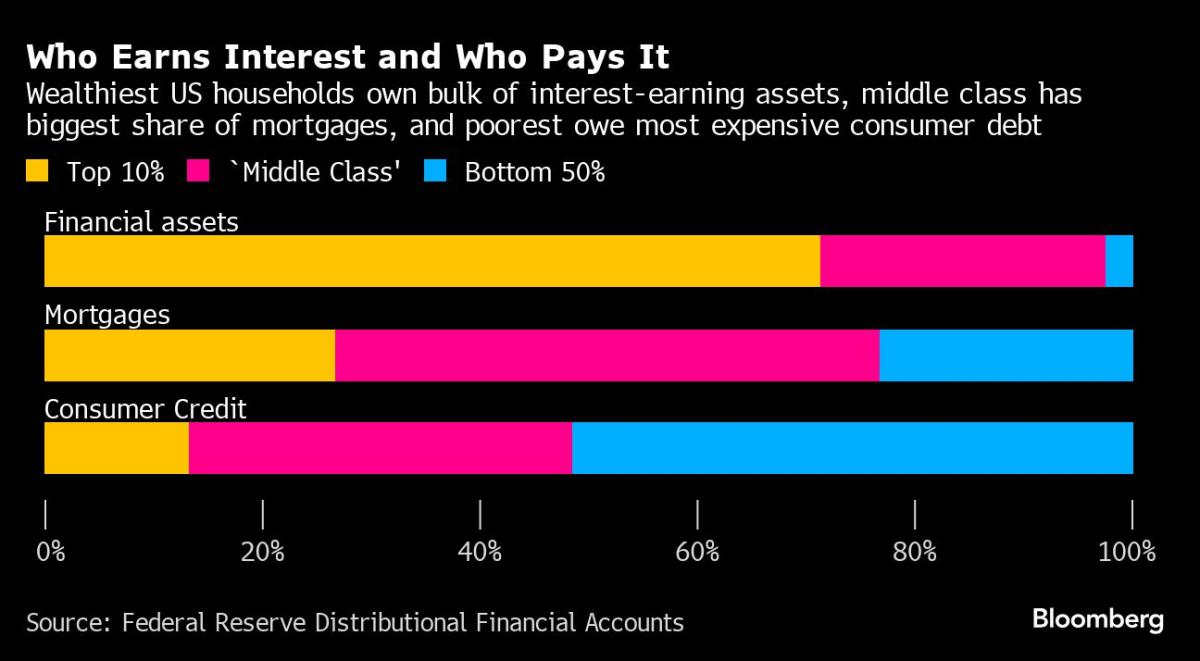

That’s because the people who earn more when rates go up are generally not the same people who face bigger bills. Ownership of interest-earning assets skews toward the wealthiest, while Americans with the most expensive kinds of debt are more likely to be lower earners.

As well as widening inequality, that distribution has consequences for the economic impact of rate increases.

Put simply, the payouts tend to go to savers who are less likely to give the economy a boost by spending each extra dollar on goods and services. By contrast, the bills land on the doorsteps of households who probably would’ve used those dollars to buy stuff — if they didn’t now have to spend them on servicing debt instead.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.