(Bloomberg) — For Rick Plympton, there’s no going back to the pre-Covid economy. The chief executive officer of precision-lens maker Optimax Systems Inc. sees “shifting sands” in many aspects of his business.

Most Read from Bloomberg

It’s tough to find enough workers, prices of key inputs are more volatile and there are longer lags between ordering equipment and having it show up on the Ontario, New York firm’s shop floor. There’s also strengthened support in Washington for the US chip-making industry — which uses Optimax lenses — as politicians take in an altered geopolitical landscape.

Many of these changes aren’t temporary, in Plympton’s view. Tight labor markets “are going to be with us for decades,” he says.

But Federal Reserve Chair Jerome Powell isn’t ready to be so conclusive. “The pandemic is still writing the story of our economy right now,” he told House lawmakers March 6. “We should just be prepared to be surprised with the next chapter.”

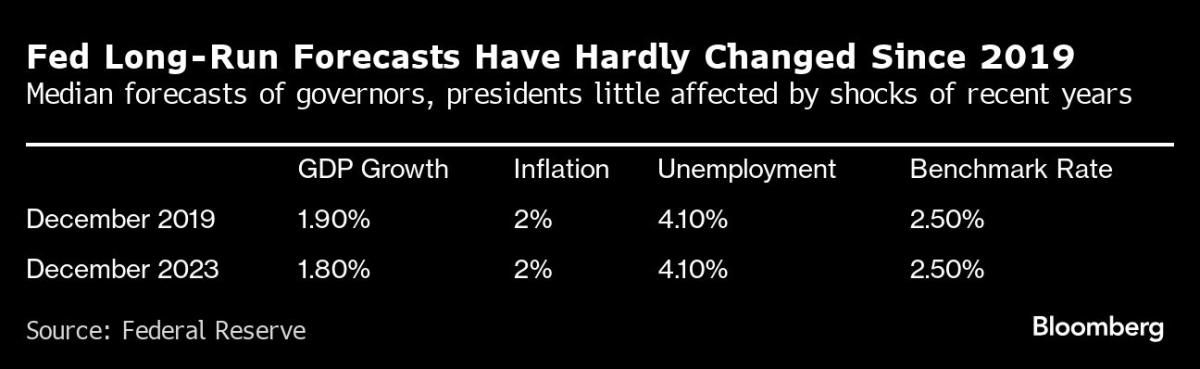

And economic projections for the long haul from Powell and his fellow Fed policymakers offer a picture of not much having changed despite the supply-chain, labor and geopolitical shocks of recent years.

Central banks serve as a nation’s economic narrator, offering descriptions of economic trends and explaining why their policy fits the contours of a particular moment. The lack of an overview from the Fed on why US growth has proven resilient to high interest rates sows volatility, as investors have to guess how they will respond. Rate volatility makes it hard for households and businesses to plan.

“Powell keeps talking about normalization and rebalancing, but you can’t go back to 2019,” says Jim Bianco, president of Bianco Research. “Whenever we have a big shock in the economy, like 2008 or 2020, the economy is changed.”

Never miss an episode. Follow the Big Take DC podcast on iHeart, Apple Podcasts, Spotify or wherever you listen. Read the transcript.

Bianco, who’s been analyzing the US economy and financial markets for more than three decades, reels off a list of features in the economy that seem new.

Consumers seem to have a higher propensity to spend – perhaps due to greater confidence in job security, or even a generational shift away from precautionary saving, with the aftermath of the 2007-09 financial crisis now more distant. The personal saving rate was less than 4% on average the past two years, compared with more than 6% over the decade through 2019.

Companies now seem to keep precautionary inventory on hand, with wholesale stockpiles running at a higher rate to sales now than pre-pandemic.

Then there’s the job market.

At Optimax, even salary hikes and a profit-sharing plan that distributes 25% of profits to employees hasn’t been able to lure enough workers. “Post-pandemic, we have more jobs than workers,” Plympton says in a telephone interview.

Drew Greenblatt, the president of Marlin Steel Wire Products in Baltimore, has the same challenge. As he walks through his cavernous shop floor and points to new precision tools that can turn out more parts per hour, he’s anxious over finding skilled staff to operate it. “It’s killing me,’’ he says. “I have all this technology, and it’s just sitting there.”

Such anecdotes help illustrate why the US unemployment rate is near historic lows, at under 4%, despite what Fed officials describe as a “restrictive” interest rate. Wage gains continue to run north of 4% annually, against an average of 2.4% over the decade through 2019. With demand still solid, companies are able to boost their prices as they contend with higher salaries.

For many investors, the economy looks more inflationary for the long haul, requiring higher interest rates. Futures trading suggests about a 3.5% benchmark Fed rate in a few years’ time — a full percentage point more than Fed policymakers’ latest long-run forecast, which is set to be updated at the March 19-20 policy meeting.

Monetary policy works as much through communication of the outlook as it does through increases or cuts in interest rates. If investors understand how the Fed is thinking about the state of the world, it reduces overall volatility and lowers the extra yield investors pay for risk.

In the past, Fed guidance helped to shape expectations. When economic growth picked up in the 1990s, then-Fed Chair Alan Greenspan highlighted a structural acceleration in productivity that meant inflation risks had diminished.

Today, Powell can call upon enormous resources in gauging what the post-pandemic shocks mean for the US economy. The Fed Board has two divisions that make domestic and international economic forecasts, as well as a policy strategy unit, in Washington. There were more than 700 full-time equivalent staff members for 2023, with a $202 million budget.

Still, there are big risks for a central bank coming to grand conclusions after an economic hurricane like the pandemic and the billions of dollars in fiscal and monetary policy support that followed it.

Fed officials still have scars from saying in 2021 that inflation was mainly a phenomenon of transitory supply-chain clogs, only to see it broaden out and exceed almost everyone’s expectations thereafter.

Today, declaring that the economy can sustain a faster pace of growth thanks to a new investment boom could risk being read as an endorsement of President Joe Biden’s policies, with the November election looming. Alternatively, stating that the US is now in for higher inflation and interest-rate settings for the long haul could play into Republican arguments. Powell saw the political sensitivity first-hand this month when he mentioned at a congressional hearing that immigration had taken some of the pressure out of the labor market. Lawmakers peppered him with comments on the point.

Lou Crandall, the chief economist at Wrightson ICAP LLC, says that staying away from a conclusive view of structural economic changes “strikes me as absolutely the right way to run policy.”

“At a time when trends are evolving faster than your expectations, it would be hard to be definitive about what this means for policy,” Crandall says.

Even so, not all central bankers have been timid about calling out new features in the economy.

Powell’s counterpart at the European Central Bank, Christine Lagarde, judged the world economy may be “entering an age of shifts in economic relationships and breaks in established regularities.” Speaking at the annual Jackson Hole, Wyoming conference last August, Lagarde pointed to three such breaks: changes in the labor market and the way people work, a transformation in energy markets, and the fragmenting of the world into competing blocs. While it’s unclear whether the shifts are permanent, they’ve been “more persistent than we initially expected,” she said.

Fed policymakers will have the chance at putting forward a fresh assessment of the economy’s underlying shifts when the central bank begins a new strategic review later this year. The last one, in 2020, focused on how to address persistent undershooting of the 2% inflation target. It proved ill-timed, as it wrapped up just before the cost of living began to surge.

Whichever way Fed officials lean this time, today’s challenges are if anything greater than the years before Covid struck.

The bottom line for Julia Coronado, partner at MacroPolicy Perspectives LLC: “We are in the middle of something that’s still incredibly difficult and volatile” to forecast.

–With assistance from Edward Bolingbroke and Alex Tribou.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.