CrowdStrike (NASDAQ: CRWD) outspoken Co-Founder and CEO George Kurtz went on the offensive during the last quarterly conference call and the market reacted well to what he had to say. As a result, shares of the leading endpoint-cybersecurity software provider have held on to most of their 200%-plus gain since the start of 2023.

Kurtz threw some subtle shade at numerous cybersecurity peers on the last earnings update, even name-dropping Palo Alto Networks (NASDAQ: PANW) as CrowdStrike’s unified platform is attempting to gobble up market share of a fiercely competitive security-software market. (For the record, Palo Alto’s CEO, as well as Zscaler‘s (NASDAQ: ZS) and Cloudflare‘s respective co-founders and CEOs, also tend to talk a lot about their peers’ failings on quarterly calls with investors.)

Peeling away all of cybersecurity leaders’ chutzpah reveals solid reasons investors should still be paying attention to CrowdStrike and might even consider buying shares even as it trades near all-time highs.

A market ripe for consolidation

All of the cybersecurity pure-play leaders (which exclude big, diversified tech companies, including the Magnificent Seven, all of which have various types of cybersecurity offerings) have been talking a lot about “platforming” in the industry. What’s that?

After years of fast-evolving, enterprise security needs, accelerated by the advent of cloud computing and the pandemic, organizations have a multitude of cybersecurity vendors to choose from. But the leaders — CrowdStrike in endpoint security for things like laptops and other mobile devices, Palo Alto Networks and Fortinet (NASDAQ: FTNT) in older network security, and Zscaler in cloud-based network security — are looking to expand their offerings and provide their customers with more of an all-in-one package. Not only would fewer vendors simplify a security team’s life, but consolidation can also lead to better outcomes.

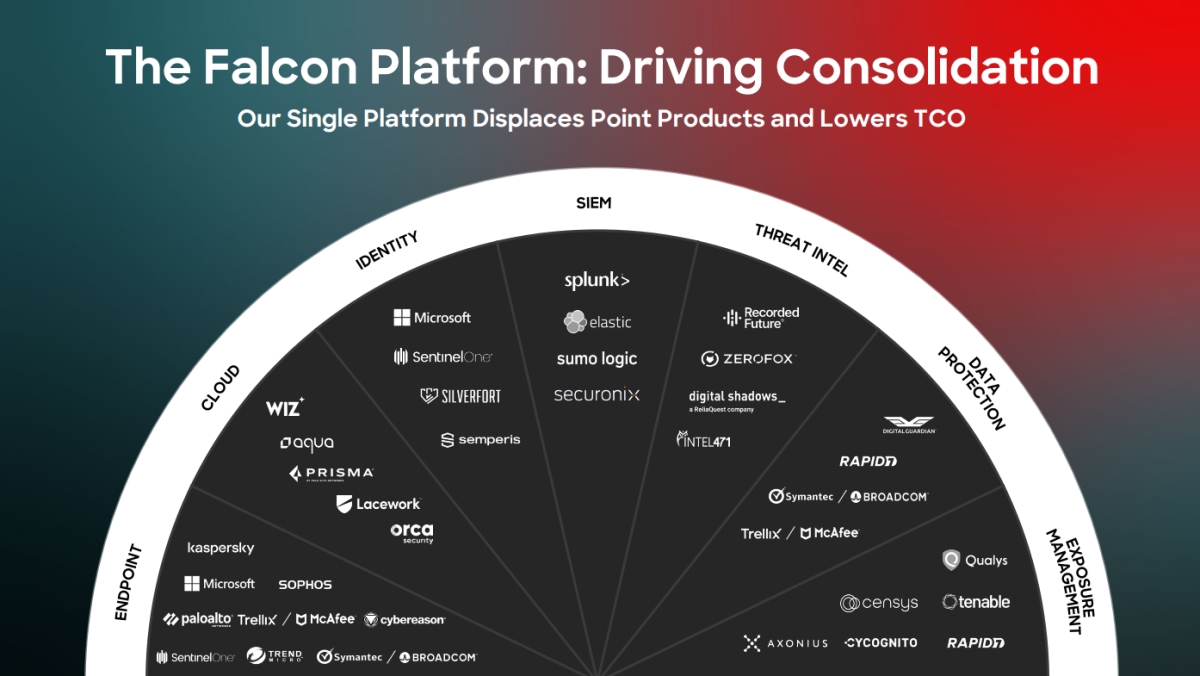

CrowdStrike in particular thinks this latter point works in its favor. Kurtz and company often talk up CrowdStrike’s single platform that covers multiple needs in software security. That can make keeping tabs on security a cinch, rather than having to manage multiple modules and dashboards with disparate data (see chart below).

All of this talk about displacing smaller players to consolidate the complicated cybersecurity field has some truth to it. The biggest four players have been growing their sales at a faster-than-industry-average pace for some time, which, overall, has been outstanding at a low-teens percentage rate of growth. CrowdStrike has been a particular standout over the last five years, as it just achieved its first year with sales exceeding $3 billion.

CrowdStrike’s enduring advantage in the security software race?

CrowdStrike, in spite of all its spectacular growth, hasn’t appealed to a broad group of investors since its initial public offering (IPO) in 2019. That’s because up until the second half of fiscal 2024 (the 12-month period ended in January 2024), CrowdStrike operated at a generally accepted accounting principles (GAAP) loss. Of course, the company always showed promise of eventually achieving GAAP profitability. Its free cash flow (FCF) has been positive and rising for a long time.

However many investors who favor a “value” have called out high amounts of employee stock-based compensation (which is excluded in the FCF calculation) as a sore spot. There’s good reason to worry about stock-based compensation, as it can excessively dilute existing shareholders. However, CrowdStrike has now successfully scaled its business to profitability on all counts, which could please a new group of would-be owners of the stock. And on a per-share basis (which accounts for a growing share count), the argument that stock-based compensation is diluting shareholders hasn’t held much weight.

More importantly than CrowdStrike’s fist-pumping about its software technology, profit metrics like this help confirm that a company also has the right business model to succeed over the long term. To be clear, CrowdStrike still has lots of progress to make on this front. But as it extends its cybersecurity platform, the profit margins should continue to tick higher.

This is no cheap stock, so not all value investors will want to bite. CrowdStrike currently trades for over 80 times this year’s expected GAAP earnings per share and over 60 times next year’s early expectation for earnings. Nevertheless, with the company expecting to grow its revenue by another 30% in calendar year 2024, there’s a lot to like about CrowdStrike if you plan to buy and hold for the long term. I recently nibbled a bit more of this stock, and it will remain on my watch list.

Should you invest $1,000 in CrowdStrike right now?

Before you buy stock in CrowdStrike, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and CrowdStrike wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 11, 2024

Nicholas Rossolillo and his clients have positions in CrowdStrike, Fortinet, and Palo Alto Networks. The Motley Fool has positions in and recommends CrowdStrike, Fortinet, Palo Alto Networks, and Zscaler. The Motley Fool has a disclosure policy.

Is CrowdStrike Stock a Buy Right Now? was originally published by The Motley Fool