(Bloomberg) — The Bank of England and the Federal Reserve were wrong to raise interest rates before starting to unwind quantitative easing, according to one of the BOE’s own researchers.

Most Read from Bloomberg

Both the UK and US central banks have been shrinking their balance sheets by selling assets bought over the last 15 years under QE, once borrowing costs had been cut close to zero.

However, they began so-called quantitative tightening only after raising rates to tame the surge in inflation in 2022. The decision was a mistake, according to Richard Harrison, a senior research and policy advisor in the monetary analysis directorate at the BOE.

“Optimal policy implies that balance sheet unwind will often begin before the policy rate has been raised from its lower bound, while UK and US policymakers have taken the opposite approach,” he wrote in the Staff Working Paper published online Friday by the BOE.

Harrison added that a very rapid balance sheet unwind, involving active asset sales as well as passive maturities, can be a “perfect substitute” for rate rises “in terms of their influence on the overall monetary policy stance.”

He stressed that the opinions were “solely” his and “cannot be taken to represent those of the BOE.” The paper also focused on overall “social welfare,” including growth, employment and inflation, and reflected broader objectives than straightforward inflation targeting.

The BOE, which has a 2% inflation target, has repeatedly said interest rates are its primary policy tool and QT operates “in the background.” The BOE has raised rates to 5.25% from 0.1% in December 2021.

Governor Andrew Bailey had originally planned to begin unwinding QE before raising rates, in line with the paper’s findings. In an opinion piece for Bloomberg in July 2020, shortly after relaunching QE in the pandemic, he wrote: “When the time comes to withdraw monetary stimulus, in my opinion it may be better to consider adjusting the level of reserves first without waiting to raise interest rates on a sustained basis.” He later changed his position.

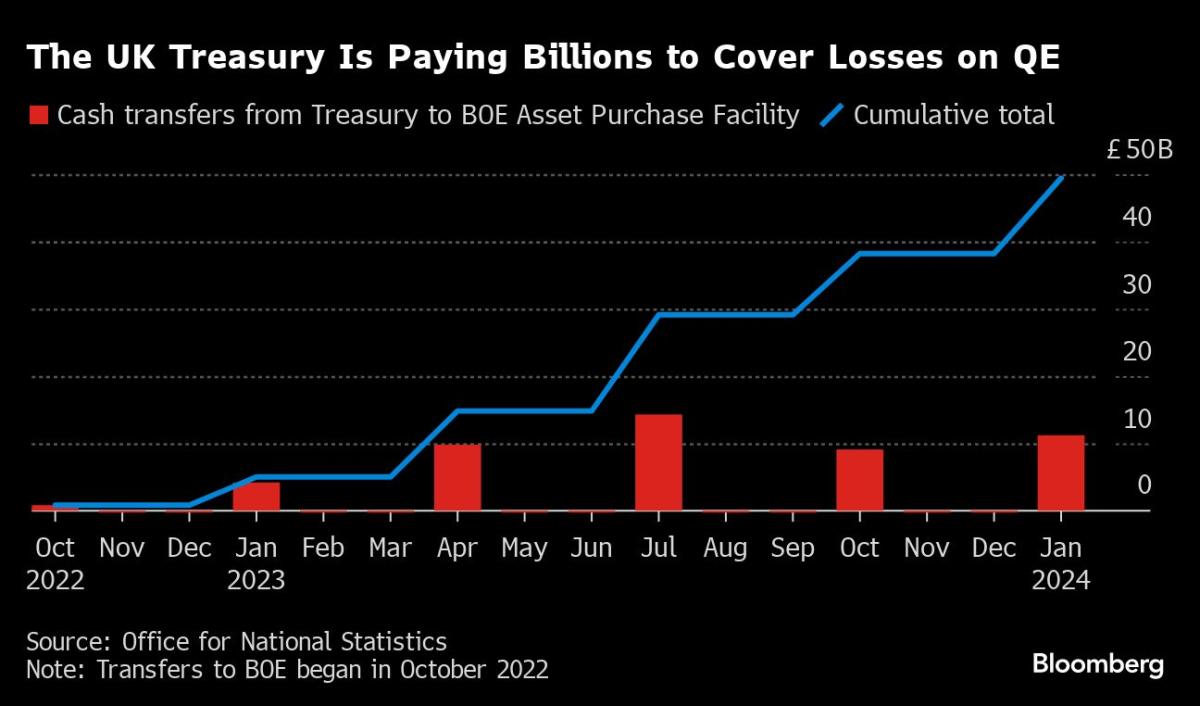

The bank has separately come under fire for billions of pounds of losses caused by QE that taxpayers must cover under a state guarantee agreed when the program began in 2009. The government has already transferred almost £50 billion to the BOE under the indemnity, a figure that could double over the lifetime of QT, according to the BOE.

The QT losses are the direct result of higher interest rates, which the BOE must pay on “reserves” created to buy the assets. Lawmakers in the UK parliament have urged the bank to consider “value for money” for the UK state in its QT decisions.

At its peak, the BOE had bought £895 billion of assets to shore up the economy and prevent deflation. The policy was used after rates were cut as low as they could go.

The reserves to buy the assets are effectively central bank deposits held by high street lenders.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.