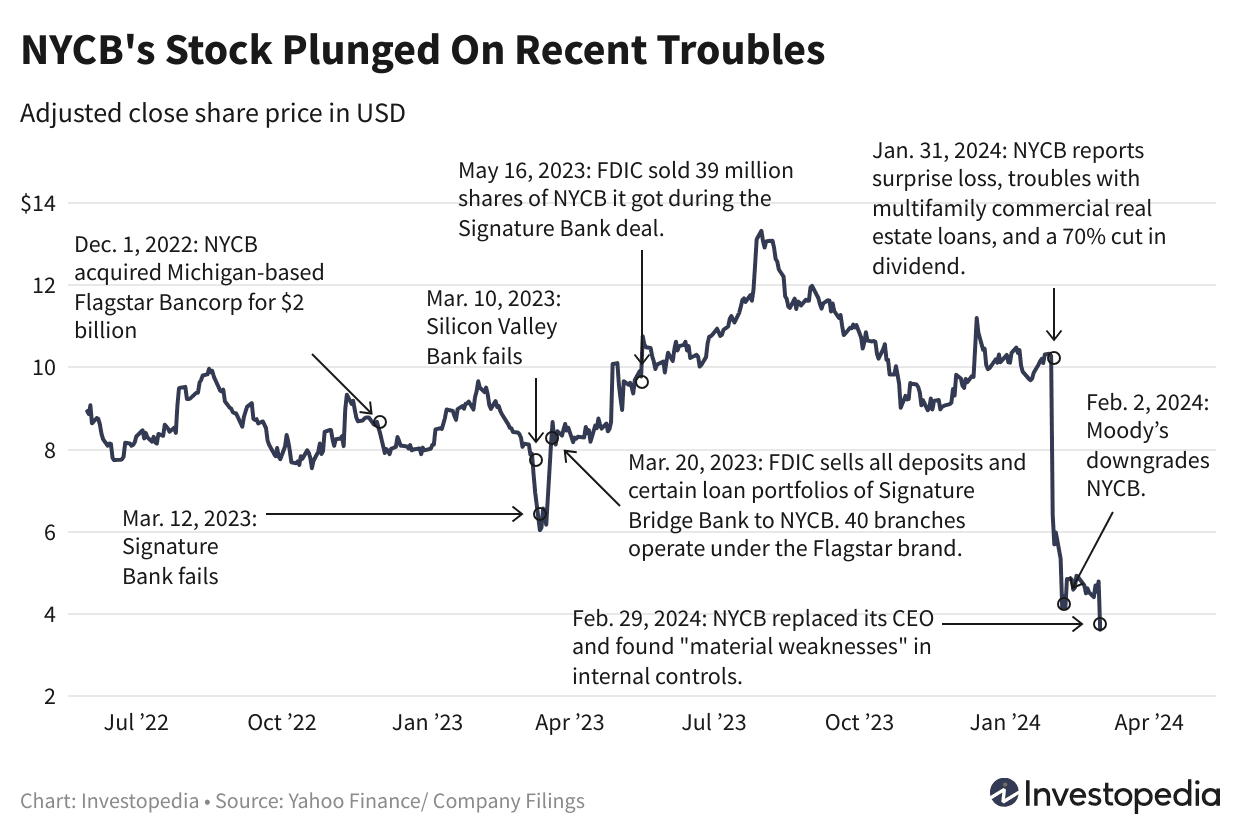

New York Community Bancorp’s (NYCB) shares plunged nearly 25% Friday, a day after the company admitted to identifying “material weaknesses” in controls, reported a surprise write-off of an additional $2.4 billion loss and sacked its chief executive of nearly 30 years.

Here’s what you need to know about the ailing bank’s troubles:

Bigger loss and “material weakness” in controls

New York Community Bancorp announced that it had identified “material weaknesses” in the company’s internal controls related to internal loan review, resulting from ineffective oversight, risk assessment and monitoring activities.

“This review of internal controls could lead to additional CRE-related reserve building, particularly related to the company’s NYC rent-regulated multifamily exposure,” Wedbush analysts wrote in a note Friday. (More on commercial real estate and regulated multifamily building exposure below.)

It also tacked on an additional $2.4 billion loss via a goodwill non-cash impairment charge to the $260 million fourth-quarter shortfall it reported in January.

After the disclosure, Fitch Ratings downgraded the bank saying the “remediation of the material weakness will be executed over the near term.”

Incomplete Information

Analysts at Piper Sandler fear that since the assessment is incomplete, there could be more bad news in store.

“We fear that there could be additional issues that get raised as a new team takes the reins. None of that gives us comfort in recommending to investors that they should buy the stock,” they wrote in a note Thursday.

Since Moody’s downgraded NYCB’s credit rating in early February, the bank has not provided more information about its deposits, which is leading analysts at DA Davidson to infer that they have fallen.

“The question is by how much? And will likely be down even more on Friday,” DA Davidson’s Peter Winter wrote in a research note.

Reading Too Much Into CEO Change?

The bank also replaced CEO Thomas Cangemi, who has been with the company for nearly three decades, with former Flagstar Bank CEO Alessandro DiNello. New York Community Bank acquired Flagstar in December 2022.

While a top-level executive shake-up can sometimes make investors nervous, analysts were not surprised.

“During the investor call on February 7, with Sandro answering 99% of investor questions, it was pretty clear that in addition to becoming elected to executive chairman, Sandro was taking over the day-to-day operations of the company,” DA Davidson’s Winter wrote. “So it comes as no surprise that Tom stepped down from the bank as these issues and extremely poor 4Q results where under his watch.””

Keefe, Bruyette & Woods analysts were similarly unfazed by the shakeup, saying, it “shouldn’t be all that unexpected given Mr. DiNello was appointed Executive Chairman on Feb. 6.”

What’s Ailing NYCB?

NYCB has a big red flag that many other regional banks don’t have: an $18.3 billion portfolio of loans made to rent-regulated multifamily buildings in New York City. That equaled roughly 22% of all of the bank’s loans at the end of December.

High interest rates, persistent inflation and plummeting property values are putting owners of such buildings in a bind, jeopardizing their ability to pay back loans. Add to that, the city’s strict 2019 rent stabilization legislation, which basically makes it harder for landlords to hike rents in order to pay for things like renovations.

“Valuations for many buildings are dipping below the outstanding principal balances on related mortgages,” wrote David Chiaverini, an analyst at Wedbush Securities, in a February note.

He outlined an anecdote of a real estate broker who purchased a rent stabilized building in 2017 for $12.5 million, and sold it last year for $6 million after pouring $1 million into renovations, implying all of the owner’s equity was erased and the bank also took a loss on the loan.

NYCB Is Not Alone

Almost a year ago, a string of bank failures put regional banks in focus. Exposure to commercial real estate loans was hailed as the next big risk to such banks, which were scrambling to retain customer trust and deposits.

While most of the alarms were sounded around loans for office properties, risks presented by loans to multifamily rent-stabilized properties became apparent after NYCB’s struggles came to light.

Regulators and analysts have so far categorized NYCB as an outlier but have admitted that loans to rent-regulated multifamily units present a broader risk to other exposed banks as well.

A lot of commercial real estate loans, including those for multifamily units, are starting to come due, but high interest rates are making it harder to refinance them.

“I’m concerned. I believe it’s manageable although there may be some institutions that are quite stressed by this problem,” Treasury Secretary Janet Yellen told the House Financial Services Committee in early February.

NYCB Could Shore Up Liquidity Via Asset Sale Like Others Before

“They have to build liquidity and to build capital and they have to attempt to reduce concentration,” Chris McGratty, managing director at Keefe, Bruyette & Woods said in a February phone interview prior to the recent announcements. “What they need is time.”

The bank is likely to sell non-core assets and reduce risk-weighted assets. “Basically, everything is on the table,” McGratty said. He cited PacWest as having navigated last year’s difficulties, first through asset sales before it was finally sold to Banc of California (BANC).

NYCB Depositors May Breathe Easier Than Investors, For Now

While investors may have a hard time digesting the wild ride that NYCB stock has been on, depositors of NYCB should remember that the Federal Deposit Insurance Corporation (FDIC) provides deposit insurance for up to $250,000 worth of deposits.

As of February 6, roughly 72% of NYCB’s $83 billion total deposits were FDIC insured. Uninsured deposits, which likely exceed the $250,000 deposit insurance limit, stood at $22.9 billion.