(Bloomberg) — Federal Reserve Chair Jerome Powell is expected to double down on his message that there’s no rush to cut interest rates, especially after fresh inflation data showed that price pressures persist.

Most Read from Bloomberg

Powell is headed to Capitol Hill, where he’ll deliver his semiannual monetary policy testimony to a House committee on Wednesday and a Senate panel on Thursday. The US central bank chief and nearly all of his colleagues have said in recent weeks that they can afford to be patient in deciding when to cut rates given underlying strength in the US economy.

The “danger of moving too soon is that the job’s not quite done, and that the really good readings we’ve had for the last six months somehow turn out not to be a true indicator of where inflation’s heading,” Powell said in an interview with CBS’s 60 Minutes on Feb. 5.

That cautious approach has been validated in recent weeks by data showing inflation picked up last month. But it’s not likely to satisfy Democrats, who are anxious about how the path of rates could affect the November presidential election and down-ballot races. They’re expected to press the Fed chief on why officials are keeping borrowing costs so high, risking damage to the economy, when they’ve made so much progress on inflation.

The data highlight for the week will be the monthly jobs report on Friday. Economists project payrolls growth moderated in February to 200,000 following a 353,000 surge a month earlier that was the largest in a year. The jobless rate is seen holding at 3.7%, while hourly earnings growth probably cooled.

On Wednesday, the Fed will issue its Beige Book survey of regional business contacts from across the country. Other data in the coming week include separate February surveys of purchasing managers at service providers, as well as figures on the January trade balance and job openings.

What Bloomberg Economics Says…

Powell is expected to maintain a hawkish stance in his semiannual testimony to Congress, signaling to markets that the Fed is in no hurry to cut rates. If that leads to tighter financial conditions, it will keep the pressure on the economy and raise the chance of additional lagged impacts from monetary policy.”

— Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou. For full analysis, click here

Elsewhere, other political set-piece events from China’s National People’s Congress to the UK budget will draw attention, as will rate decisions in the euro zone and Canada that are expected to show no change.

Click here for what happened last week, and below is our wrap of what’s coming up in the global economy.

Asia

The National People’s Congress in China will be at the center of attention in Asia as investors, economists and policymakers watch for signs that Beijing is prepared to take more significant stimulus measures.

China’s growth target for the year may also offer clues on how aggressively the country’s leadership will pursue a recovery. The latest price data and cumulative trade figures for January and February will indicate how severe China’s slide into deflation is becoming, as well as the lack of major support for the economy via exports.

February inflation figures for Tokyo are likely to show a strong uptick as the impact of subsidies a year ago fades, an outcome that could fuel bets on a March rate hike from the Bank of Japan at a time when the labor market has tightened.

Board member Junko Nakagawa will provide the latest signaling from the central bank on Thursday.

Economists in Australia will fine-tune their growth forecasts on Tuesday after current account data comes out. Gross domestic product is due the following day, with tepid growth expected to continue.

Growth figures for South Korea are likely to stay largely unchanged after a revision, but consumer prices are expected to heat up again in data due on Wednesday.

Malaysia is expected to keep rates unchanged at 3% on Thursday.

Europe, Middle East, Africa

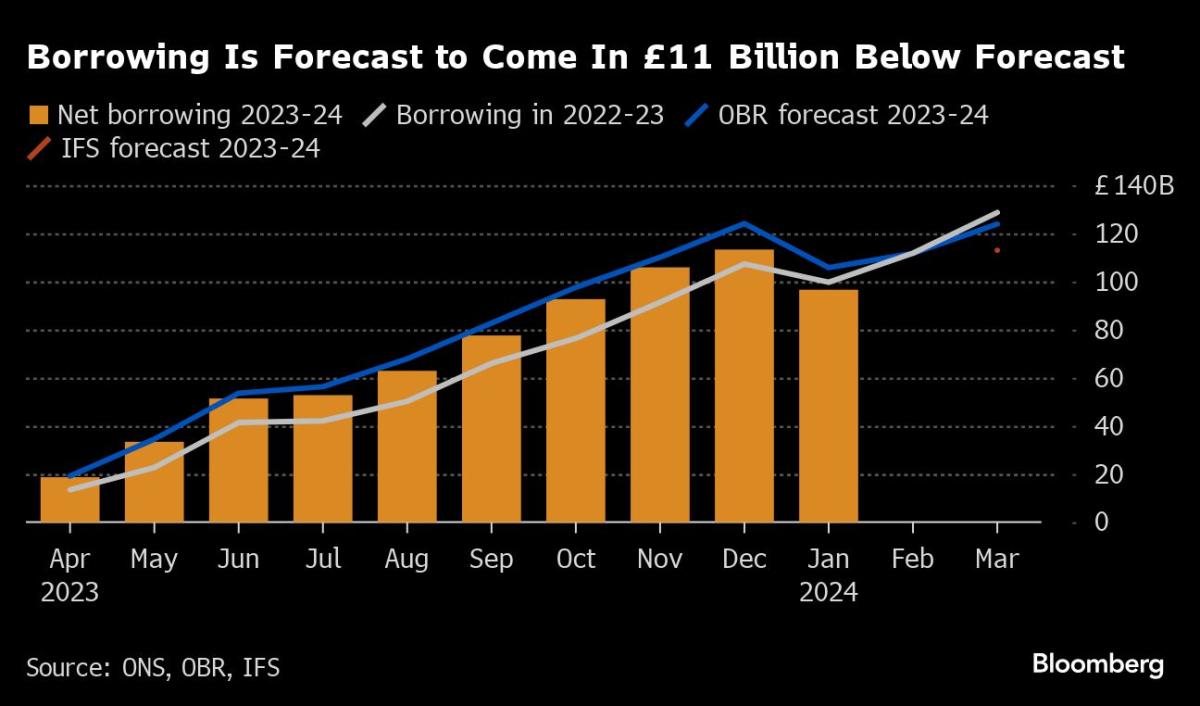

In the UK, Chancellor of the Exchequer Jeremy Hunt will unveil his budget on Wednesday in what could be the final such announcement before a general election that’s likely this year.

Speculation in recent days has centered on possible giveaways for voters, and an end to the “non dom” status used by wealthy foreigners. Hunt may have limited room for maneuver on tax cuts.

In the euro zone, the European Central Bank decision on Thursday will be the main event. Policymakers will unveil their first quarterly forecasts of the year, which may show that they’re moving closer toward delivering a rate cut in coming months.

Faster-than-expected inflation in numbers released on Friday could still give officials reason for caution, and they’re also awaiting data on wage deals to ensure that the full pace of consumer-price gains isn’t getting reflected in pay.

Data in the euro region will give a reading on the strength of manufacturing in key economies. Industrial numbers from Germany, France and Spain are all due.

Switzerland, whose central-bank chief just announced his departure for later this year, will release inflation on Monday that’s expected by economists to have slowed to 1.2%, the weakest since 2021.

Turning east, Polish monetary officials are anticipated to keep their rate unchanged at 5.75% on Wednesday, while their Serbian peers the next day will reveal if they’re opting to hold borrowing costs at 6.5% again.

In Turkey, analysts predict data on Monday will show inflation accelerated to 66% in February, an outcome that’s roughly in line with forecasts from the central bank.

And the next day in South Africa, a report is likely to show that the nation skirted a recession, helped by an expansion in its mining and manufacturing industries. The economy is forecast to have grown 0.3% in the fourth quarter of 2023.

Latin America

Brazil’s January industrial production data may show 2024 getting off to a strong start.

In Luiz Inacio Lula da Silva’s first year back in office, output averaged 0.1%, far below the 3.4% average seen during his first stint as president. Output averaged -1.2% over the next 12 years.

Brazil will also serve up the central bank’s weekly survey of economists, current account, foreign direct investment, monthly trade figures, bank lending and government debt data.

In Peru, most analysts have been looking fo the central bank to deliver a seventh straight quarter-point interest-rate cut to 6% at its meeting on Thursday. February inflation data posted Friday showing an unexpected jump in consumer prices likely complicates the decision.

On the ever-critical inflation front, the early consensus expects that consumer price data will show inflation slowed in Colombia and Mexico while rising slightly in Chile.

Mexico’s double-barreled posting Thursday of mid-month and February consumer price readings will likely show enough cooling to green light Banxico to deliver a much awaited rate cut at its March meeting.

In Colombia, both the headline and core readings will slow to keep BanRep easing on March 22, while Chile’s central bank — which sees inflation hitting the target in the first half — won’t be put off by the slight uptick reported here.

–With assistance from Paul Jackson, Vince Golle, Laura Dhillon Kane, Piotr Skolimowski, Paul Wallace, Monique Vanek and Robert Jameson.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.