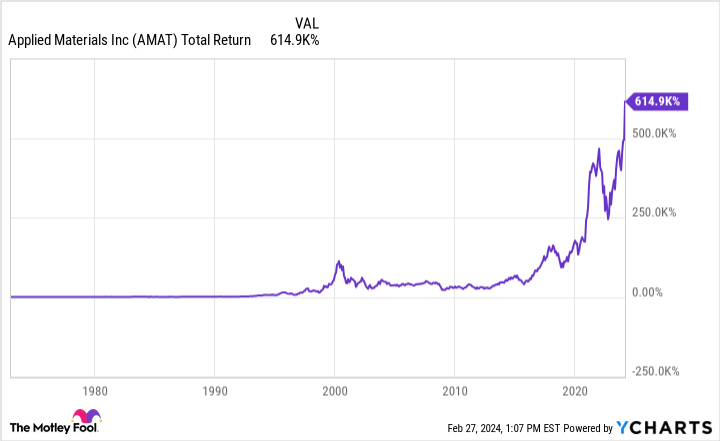

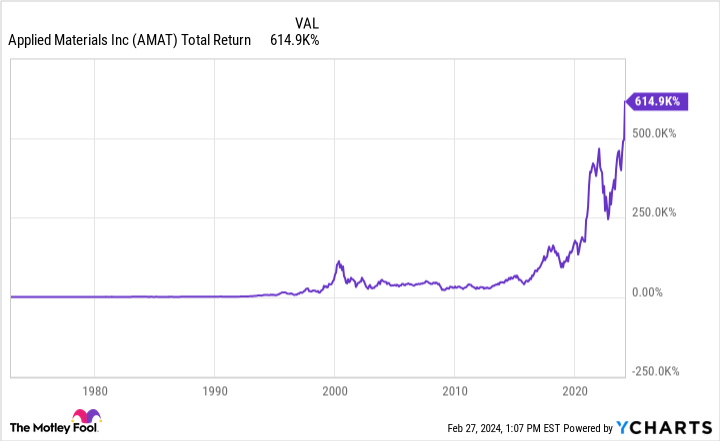

Applied Materials (NASDAQ: AMAT) is one of the most important companies you may have never heard of before. The semiconductor equipment maker — don’t worry, we’ll explain what that is — has posted phenomenal returns for long-term shareholders. Shares are up an astonishing 615,000% since its IPO in 1972, meaning every $1,000 invested at the IPO is worth over $6 million today.

With its dominant position in the semiconductor equipment market, a lot of these returns have come in the last five years, with shares up over 400% as investors get excited about the artificial intelligence (AI) revolution. This revolution needs the kind of products Applied Materials makes, and that’s been good for shareholders.

But will this party continue? Where will Applied Materials stock be five years from now? Let’s do some digging and find out.

AMAT Total Return Level data by YCharts

The backbone of AI development

Semiconductor equipment manufacturers help build tools that get used in computer chip factories. Making advanced semiconductors and computer chips — which go in smartphones, electric vehicles, and data centers — requires incredible precision and advanced techniques that have been built up over decades. Companies like Samsung and Intel have to use advanced tools if they want to manufacture cutting-edge computer chips. It simply can’t be done without them.

Applied Materials is one of the leading makers of semiconductor equipment and has been for decades. We don’t need to get into the dozens of products the company sells manufacturers, but it has an overarching goal of helping chip factories improve product quality, efficiency, speed, and cost for their computer chips. Generating over $26 billion in revenue last year, Applied Materials’ tools clearly are highly valued by manufacturers.

Smartphones and cloud computing have driven growth in the semiconductor sector over the past 15 years. The next 15 could be driven by growth in AI tools, which some analysts project could be a $1 trillion market by 2030. Regardless of the market size, Applied Materials will be crucial to the production of the computer chips powering this AI growth.

But what’s stopping someone else from replicating Applied Materials’ success? Decades of heavy spending on research and development. The company spends over $3 billion each year on R&D to keep widening this competitive advantage. This is why there are very few competitors in the semiconductor equipment space, because the incumbents have such a large advantage.

How big is the China risk?

Applied Materials is a wonderful business. But like most semiconductor businesses, it has a large presence in China, a region that typically makes up around 30% of its revenue. Political tension between the United States and China has caused the former to enact restrictions on sales of semiconductor equipment tools to the latter, most famously the advanced lithography machines from ASML. Tools from Applied Materials are affected by these new restrictions, with no telling how wide the limits will go.

In fact, the U.S. government has stepped up the pressure so much that it has now started a criminal probe against Applied Materials for evading export restrictions. Applied Materials still has a large business outside of China, but the risk of losing this segment is one that investors shouldn’t ignore.

Last quarter, 45% of Applied Materials revenue went to China, indicating that some of its customers may be over-ordering in the short term as a hedge against heavier restrictions. This could mean Applied Materials is seeing a pull forward in demand. And fines may arise from the criminal probe.

Temper your expectations

So where will Applied Materials stock be in five years? I think higher, due to its long-term competitive advantage, sector tailwinds, and relatively cheap valuation. Shares trade at a price-to-earnings ratio (P/E) of 24, which is below the market average. This seems cheap for such a dominant company in a growing sector.

But don’t expect the stock to soar over 400% in the next five years as it did in the last five. Five years ago, Applied Materials traded at a dirt-cheap P/E of under 10, with multiple expansions contributing a lot to shareholder gains. The stock can still do well, but headwinds could still arise from its exposure to China. Temper your expectations before buying Applied Materials stock at today’s prices.

Should you invest $1,000 in Applied Materials right now?

Before you buy stock in Applied Materials, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Applied Materials wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 26, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML and Applied Materials. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Where Will Applied Materials Stock Be in 5 Years? was originally published by The Motley Fool