Subscription management platform Zuora (NYSE:ZUO) reported results in line with analysts’ expectations in Q4 FY2024, with revenue up 7.4% year on year to $110.7 million. On the other hand, next quarter’s revenue guidance of $108.8 million was less impressive, coming in 2.8% below analysts’ estimates. It made a non-GAAP profit of $0.12 per share, improving from its loss of $0.04 per share in the same quarter last year.

Is now the time to buy Zuora? Find out by accessing our full research report, it’s free.

Zuora (ZUO) Q4 FY2024 Highlights:

-

Revenue: $110.7 million vs analyst estimates of $110.8 million (small miss)

-

EPS (non-GAAP): $0.12 vs analyst estimates of $0.05 ($0.07 beat)

-

Revenue Guidance for Q1 2025 is $108.8 million at the midpoint, below analyst estimates of $111.9 million

-

Management’s revenue guidance for the upcoming financial year 2025 is $455 million at the midpoint, missing analyst estimates by 3.6% and implying 5.4% growth (vs 9% in FY2024)

-

Free Cash Flow of $14.62 million is up from -$58.73 million in the previous quarter

-

Net Revenue Retention Rate: 106%, in line with the previous quarter

-

Gross Margin (GAAP): 66.7%, up from 63.7% in the same quarter last year

-

Market Capitalization: $1.22 billion

“Fiscal 2024 was a year of balanced growth and profitability where we accelerated new customer acquisition by focusing on smaller, faster lands,” said Tien Tzuo, Founder and CEO at Zuora.

Founded in 2007, Zuora (NYSE:ZUO) offers software as a service platform that allows companies to bill and accept payments for recurring subscription products.

Payments Software

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

Sales Growth

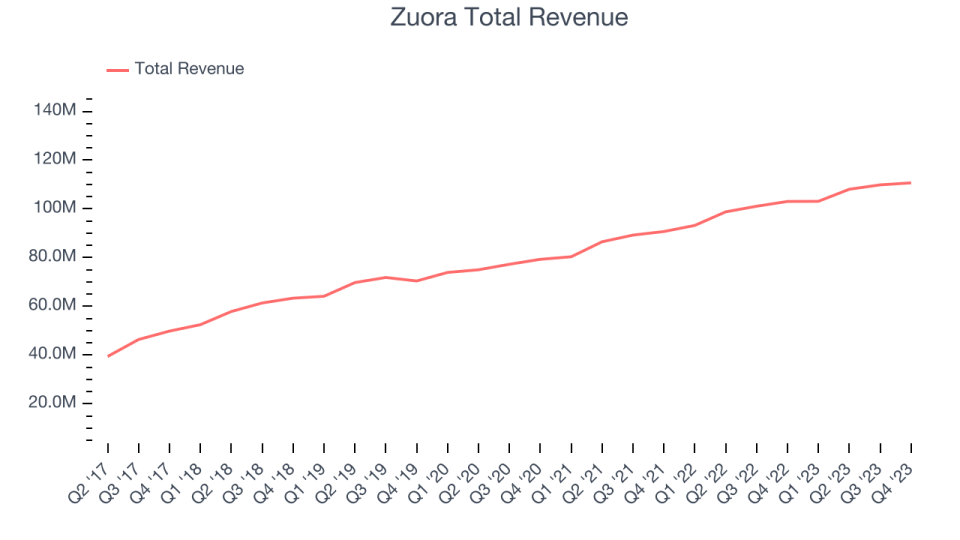

As you can see below, Zuora’s revenue growth has been unremarkable over the last two years, growing from $90.69 million in Q4 FY2022 to $110.7 million this quarter.

Zuora’s quarterly revenue was only up 7.4% year on year, which might disappoint some shareholders. Additionally, its growth did slow down compared to last quarter as the company’s revenue increased by just $820,000 in Q4 compared to $1.80 million in Q3 2024. While we’d like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter’s guidance suggests that Zuora is expecting revenue to grow 5.5% year on year to $108.8 million, slowing down from the 10.6% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $455 million at the midpoint, growing 5.4% year on year compared to the 9% increase in FY2024.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Product Success

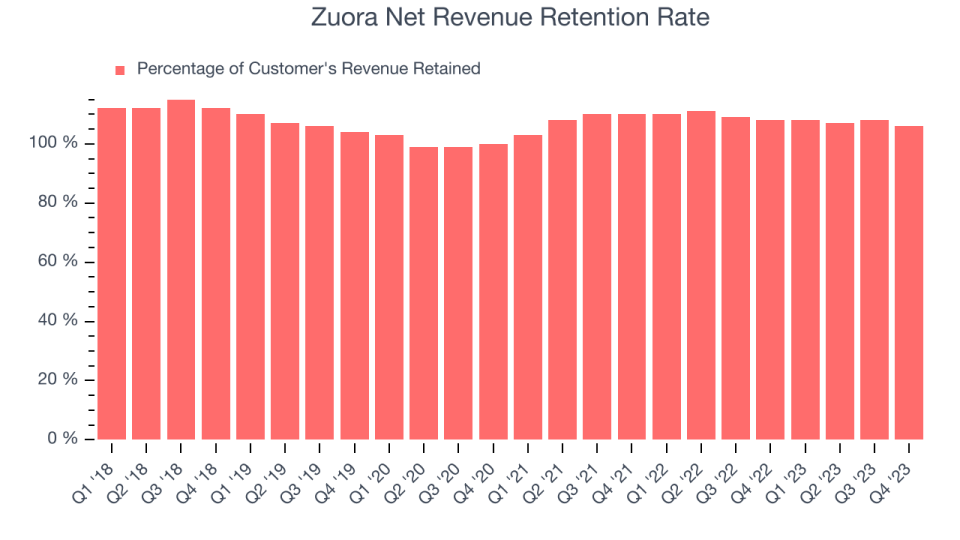

One of the best parts about the software-as-a-service business model (and a reason why SaaS companies trade at such high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Zuora’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 106% in Q4. This means that even if Zuora didn’t win any new customers over the last 12 months, it would’ve grown its revenue by 6%.

Despite its recent drop, Zuora still has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from Zuora’s Q4 Results

Zuora focused on profitablity and turned free cash flow positive year on year, which is is a positive sign. On the other hand, its full-year revenue guidance was below expectations and suggests a slowdown in already sluggish sales growth. Overall, this was a mixed quarter for Zuora. The stock is up 5.4% after reporting and currently trades at $9.05 per share.

So should you invest in Zuora right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.