After examining many stocks in today’s market, I’ve concluded that Amazon (NASDAQ: AMZN) is one of the best buys available. Even though it’s had a strong 2024, up 11%, I still think there is room for upside. I’ve pinpointed five factors that make Amazon a strong buy now, even with its great performance in 2024.

1. Amazon is no longer just a commerce business

While Amazon is well-known for its commerce business, it has quietly transitioned to a service business. These divisions include third-party seller services, advertising services, subscription services, and its cloud computing business, Amazon Web Services (AWS). Combined, these segments brought in $92.9 billion in revenue versus the commerce side’s revenue of $75.7 billion.

This is critical, as these services are vital for many businesses, which makes them more sustainable. Additionally, even though Amazon doesn’t break out the profitability of each division, looking at similar companies like Shopify for third-party sellers or Alphabet for advertising, it’s evident that services have much better margins.

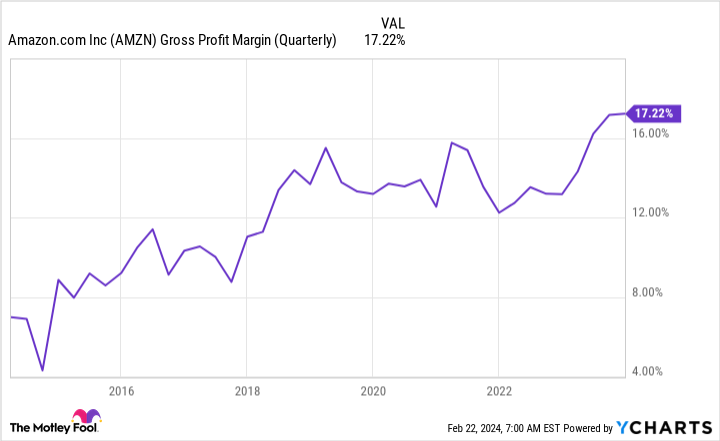

2. Amazon’s margins have dramatically improved

This leads me to my next reason for buying. Thanks to the rise of service divisions, Amazon’s gross margins have skyrocketed over the past decade.

A higher gross margin gives Amazon the potential to have a better profit margin, which has also improved in recent quarters after tanking thanks to overspending to fulfill pandemic-era demand. This will be a key metric for investors to watch as Amazon attempts to transition to becoming a company maximized for profits.

3. AWS is turning around

A key profit contributor is AWS, the cloud computing business. In the fourth quarter, Amazon’s North American commerce business made $6.5 billion in operating profits, while the international business lost $419 million. However, AWS picked up the slack, producing $7.2 billion in operating profits despite having much lower sales figures (AWS had $24.2 billion in sales in Q4 versus North American commerce sales of $106 billion).

AWS saw its profitability dip slightly as 2022’s Q4 operating margin was 24%. But it promptly recovered in 2023, and Q4 saw an operating profit of 30%

One item that has come into the spotlight is AWS’s growth. In Q4, it was up 13%, while competitors Google Cloud and Microsoft Azure both saw revenue growth in the high 20% range. While there are multiple reasons for this, Amazon’s management is starting to see new workloads come online, which should boost AWS’s growth throughout 2024. This is key as AWS is vital to Amazon’s profitability.

4. Reasonable valuation

While Amazon has had a strong year, its stock remains reasonably priced. Using traditional valuation metrics like a price-to-earnings (P/E) ratio isn’t ideal with Amazon, as it isn’t fully optimized for profits. Instead, I’ll use the price-to-sales ratio to evaluate the business. At three times sales, Amazon is valued at about the same level it was in 2018 and still below where it was during the pandemic sell-off.

5. Improving cash flows

Last is maybe the most important factor of all: Improving cash flows. Amazon’s cash flows are dramatically up due to AWS’ turnaround, the rise of service divisions, and improving margins.

Amazon’s Q4 cash flows were the highest they’ve ever been and helped propel its trailing-12-month total to new records.

With that cash, Amazon can pay down debt, repurchase shares, or fund dividends. Those actions benefit shareholders and are the primary reasons for investing in Amazon’s stock.

Despite Amaozn’s strength since the start of 2023 and so far in 2024, it’s still a great buy right now.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Amazon. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.

5 Reasons to Buy Amazon Stock Like There’s No Tomorrow was originally published by The Motley Fool